Photo from the Wall Street Journal.

At the conclusion of its meeting today (March 22, 2023), the Federal Reserve’s Federal Open Market Committee (FOMC) announced that it was raising its target for the federal funds rate from a range of 4.50 percent to 4.75 percent to a range of 4.75 percent to 5.00 percent. As we discussed in this recent blog post, the FOMC was faced with a dilemma. Because the inflation rate had remained stubbornly high at the beginning of this year and consumer spending and employment had been strongly increasing, until a couple of weeks ago, financial markets and many economists had been expecting a 0.50 percentage point (or 50 basis point) increase in the federal funds rate target at this meeting. As the FOMC noted in the statement released at the end of the meeting: “Job gains have picked up in recent months and are running at a robust pace; the unemployment rate has remained low. Inflation remains elevated.”

But increases in the federal funds rate lead to increases in other interest rates, including the interest rates on the Treasury securities and mortgage-backed securities that most banks own. On Friday, March 10, the Federal Deposit Insurance Corporation (FDIC) was forced to close the Silicon Valley Bank (SVB) because the bank had experienced a deposit run that it was unable to meet. The run on SVB was triggered in part by the bank taking a loss on the Treasury securities it sold to raise the funds needed to cover earlier deposit withdrawals. The FDIC also closed New York-based Signature Bank. San Francisco-based First Republic Bank experienced substantial deposit withdrawals, as we discussed in this blog post. In Europe, the Swiss bank Credit Suisse was only saved from failure when Swiss bank regulators arranged for it to be purchased by UBS, another Swiss bank. These problems in the banking system led some economists to urge that the FOMC keep its target for the federal funds rate unchanged at today’s meeting.

Instead, the FOMC took an intermediate course by raising its target for the federal funds rate by 0.25 percentage point rather than by 0.50 percentage point. In a press conference following the announcement, Fed Chair Jerome Powell reinforced the observation from the FOMC statement that: “Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation.” As banks, particularly medium and small banks, have lost deposits, they’ve reduced their lending. This reduced lending can be a particular problem for small-to medium-sized businesses that depend heavily on bank loans to meet their credit needs. Powell noted that the effect of this decline in bank lending on the economy is the equivalent of an increase in the federal funds rate.

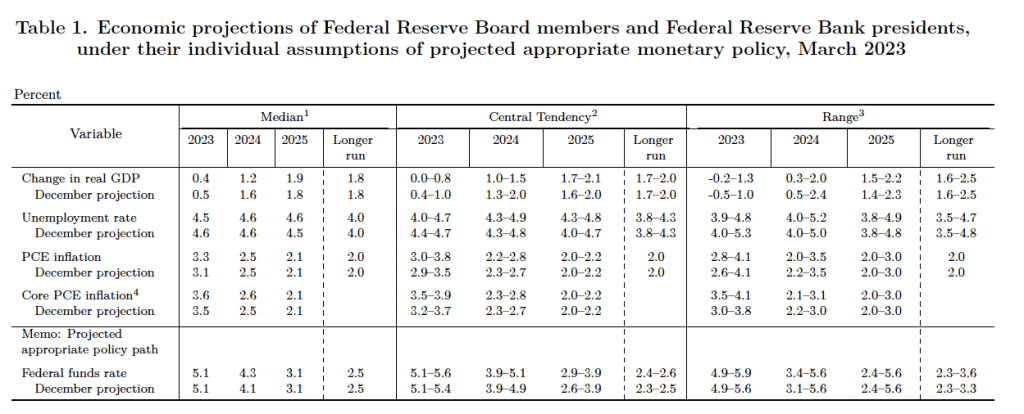

The FOMC also released its Summary of Economic Projections (SEP). As Table 1 shows, committee members’ median forecast for the federal funds rate at the end of 2023 is 5.1 percent, indicating that the members do not anticipate more than a single additional 0.25 percentage point increase in the target for the federal funds rate. The members expect a significant increase in the unemployment rate from the current 3.6 percent to 4.5 percent at the end of 2023 as increases in interest rates slow down the growth of aggregate demand. They expect the unemployment rate to remain in that range through the end of 2025 before declining to the long-run rate of 4.0 percent in later years. The members expect the inflation rate as measured by the personal consumption (PCE) price index to decline from 5.4 percent in January to 3.3 percent in December. They expect the inflation rate to be back close to their 2 percent target by the end of 2025.