Kevin Hassett, director of the National Economic Council (photo from the AP via the Wall Street Journal)

Jerome Powell’s second term as chair of the Federal Reserve’s Board of Governor ends on May 15,2026. (Although his term as a member of the Board of Governors doesn’t end until January 31, 2028, Fed chairs have typically resigned their seats on the Board at the time that their term as chair ends.) President Trump has been clear that he won’t renominate Powell to a third term. Who will he nominate?

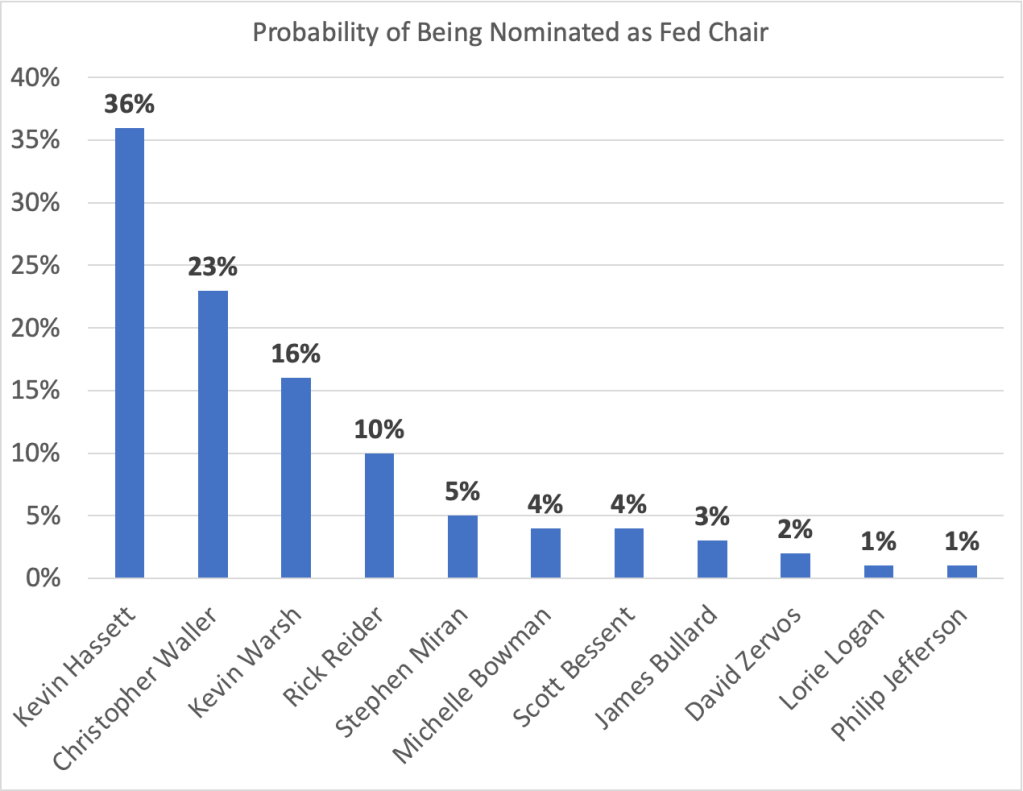

Polymarket is a site on which people can bet on political outcomes, including who President Trump will choose to nominate as Fed chair. The different amounts wagered on each candidate determine the probabilities bettors assign to that candidate being nominated. The following table shows each candidate with a probability of least 1 percent of being nominated as of 5 pm eastern time on October 27.

Kevin Hassett, who is currently the director of the National Economic Council, has the highest probability at 36 percent. Fed Governor Christopher Waller, who was nominated to the Board by President Trump in 2020, is second with a 23 percent probability. Kevin Warsh, who served on the Board from 2006 to 2011, and was important in formulating monetary policy during the financial crisis of 2007–2009, is third with a probability of 16 percent. Rick Reider, an executive at the investment company Black Rock, is unusual among the candidates in not having served in government. Bettors on Polymarket assign him a 10 percent probability of being nominated. Stephen Miran and Michelle Bowman are current members of the Board who were nominated by President Trump.

Scott Bessent is the current Treasury secretary and has indicated that he doesn’t wish to be nominated. James Bullard served as president of the Federal Reserve Bank of St. Louis from 2008 to 2023. David Zervos is an executive at the Jeffries investment bank and in 2009 served as an adviser to the Board of Governors. Lorie Logan is president of the Federal Reserve Bank of Dallas and Philip Jefferson is currently vice chair of the Board of Governors.

Today, Treasury Secretary Scott Bessent indicated that the list of candidates had been reduced to five—although bettors on Polymarket indicate that they believe these five are likely to be the first five candidates listed in the chart above, it appears that Bowman, rather than Miran, is the fifth candidate on Bessent’s lists. Bessent indicated that President Trump will likely make a decision on who he will nominate by the end of the year.

Federal Reserve Vice Chair Philip Jefferson (photo from the Federal Reserve)

Federal Reserve Chair Jerome Powell (photo from the Federal Reserve)

At the beginning of 2024, investors were expecting that during the year the Fed’s policy-making Federal Open Market Committee (FOMC) would cut its target range for the federal funds rate six or seven times. At its meeting on March 19-20 the economic projections of the members of the FOMC indicated that they were expecting to cut the target range three times from its current 5.25 percent to 5.50 percent. But, as we noted in this recent post and in this podcast, macroeconomic data during the first three months of this year indicated that the U.S. economy was growing more rapidly than the Fed had expected and the reductions in inflation that occurred during the second half of 2023 had not persisted into the beginning of 2024.

The unexpected strength of the economy and the persistence of inflation above the Fed’s 2 percent target have raised the issue of whether the FOMC will cut its target range for the federal funds rate at all this year. Earlier this month, Neel Kashkari, president of the Federal Reserve Bank of Minneapolis raised the possibility that the FOMC would not cut its target range this year.

Today (April 16) both Fed Vice Chair Philip Jefferson and Fed Chair Jerome Powell addressed the issue of monetary policy. They gave what appeared to be somewhat different signals about the likely path of the federal funds target during the remainder of this year—bearing in mind that Fed officials never commit to any specific policy when making a speech. Adressing the International Research Forum on Monetary Policy, Vice Chair Jefferson stated that:

“My baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labor market will remain strong, with labor demand and supply continuing to rebalance. Of course, the outlook is still quite uncertain, and if incoming data suggest that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer.”

One interpretation of his point here is that he is still expecting that the FOMC will cut its target for the federal funds rate sometime this year unless inflation remains persistently higher than the Fed’s target—which he doesn’t expect.

Chair Powell, speaking at a panel discussion at the Wilson Center in Washington, D.C., seemed to indicate that he believed it was less likely that the FOMC would reduce its federal funds rate target in the near future. The Wall Street Journal summarized his remarks this way:

“Federal Reserve Chair Jerome Powell said firm inflation during the first quarter had introduced new uncertainty over whether the central bank would be able to lower interest rates this year without signs of an economic slowdown. His remarks indicated a clear shift in the Fed’s outlook following a third consecutive month of stronger-than-anticipated inflation readings ….”

An article on bloomberg.com had a similar interpretation of Powell’s remarks: “Federal Reserve Chair Jerome Powell signaled policymakers will wait longer than previously anticipated to cut interest rates following a series of surprisingly high inflation readings.”

Politics may also play a role in the FOMC’s decisions. As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), the Federal Reserve Act, which Congress passed in 1913 and has amended several times since, puts the Federal Reserve in an unusal position in the federal government. Although the members of the Board of Governors are appointed by the president and confirmed by the Senate, the Fed was intended to act independently of Congress and the president. Over the years, Fed Chairs have protected that independence by, for the most part, avoiding taking actions beyond the narrow responsibilites Congress has given to the Fed by Congress and by avoiding actions that could be interpreted as political.

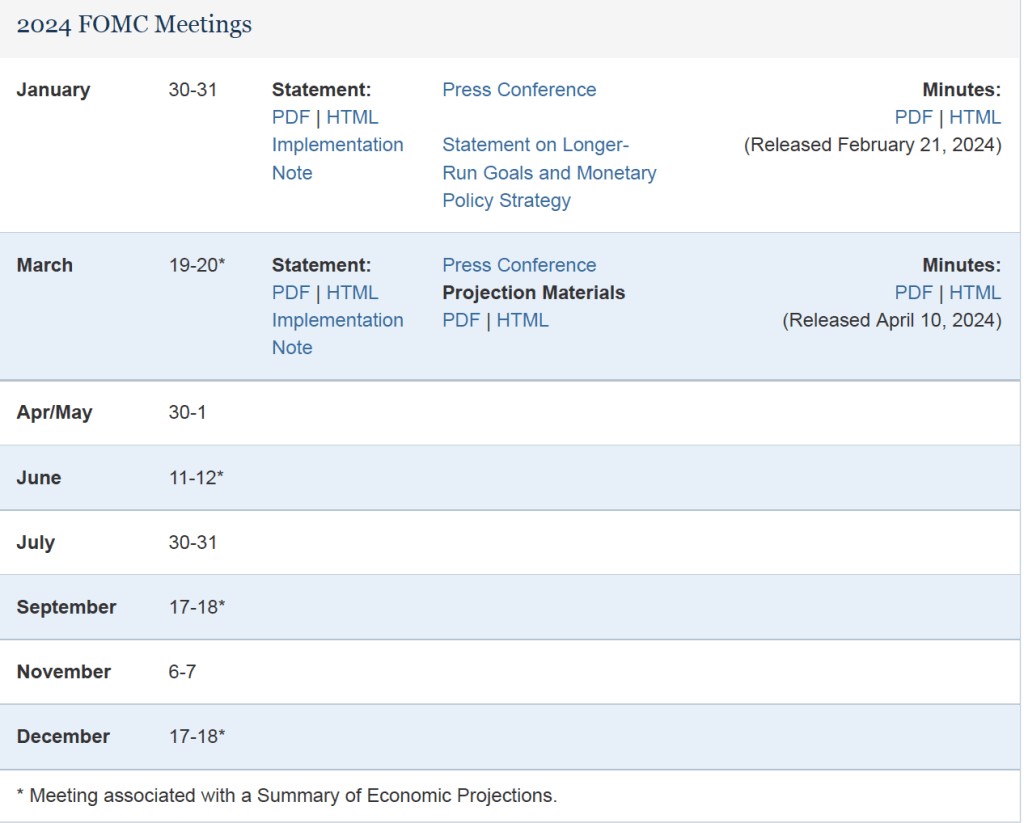

This year is, of course, a presidential election year. The following table from the Fed’s web site lists the FOMC meetings this year. The presidential election will occur on November 5. There are four scheduled FOMC meetings before then. Given that inflation has been running well above the Fed’s target during the first three months of the year, it would likely take at least two months of lower inflation data—or a weakening of the economy as indicated by a rising unemployment rate—before the FOMC would consider lowering its federal funds rate target. If so, the meeting on July 30-31 might be the first meeting at which a rate reduction would occur. If the FOMC doesn’t act at its July meeting, it might be reluctant to cut its target at the September 17-18 meeting because acting close to the election might be interpreted as an attempt to aid President Joe Biden’s reelection.

Although we don’t know whether avoiding the appearance of intervening in politics is an important consideration for the members of the FOMC, some discussion in the business press raises the possibility. For instance, a recent article in the Wall Street Journal noted that:

“The longer that officials wait, the less likely there will be cuts this year, some analysts said. That is because officials will likely resist starting to lower rates in the midst of this year’s presidential election campaign to avoid political entanglements.”

These are clearly not the easiest times to be a Fed policymaker!

Fed Chair Jerome Powell and Fed Vice-Chair Philip Jefferson this summer at the Fed conference in Jackson Hole, Wyoming. (Photo from the AP via the Washington Post.)

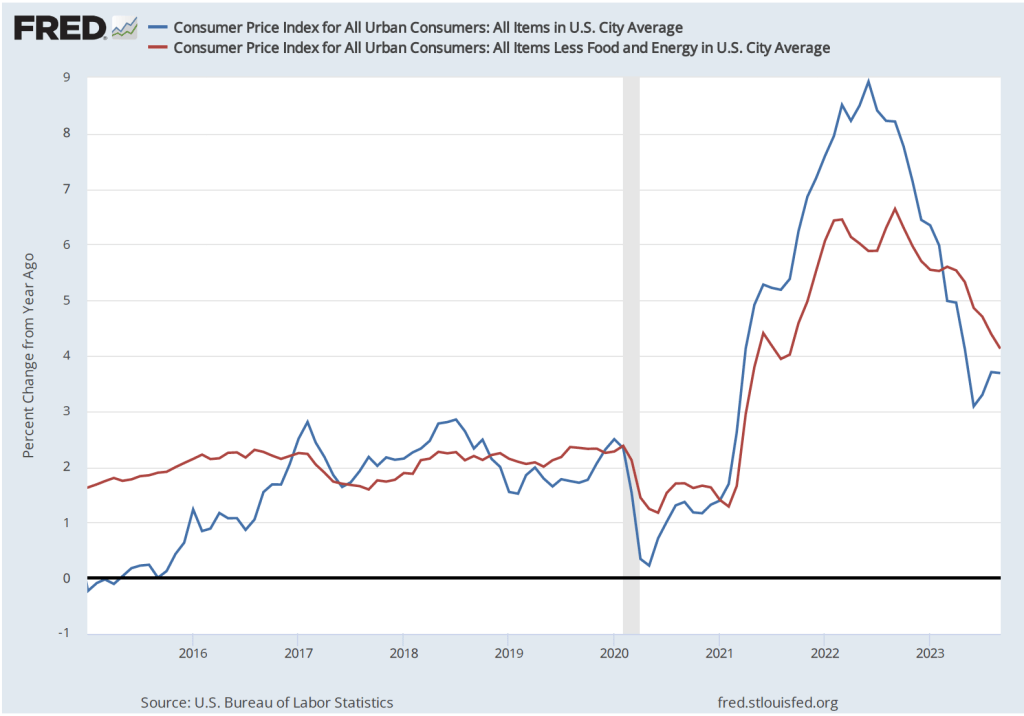

This morning, the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for September. (The full report can be found here.) The report was consistent with other recent data showing that inflation has declined markedly from its summer 2022 highs, but appears, at least for now, to be stuck in the 3 percent to 4 percent range—well above the Fed’s 2 percent inflation target.

The report indicated that the CPI rose by 0.4 percent in September, which was down from 0.6 percent in August. Measured by the percentage change from the same month in the previous year, the inflation rate was 3.7 percent, the same as in August. Core CPI, which excludes the prices of food and energy, increased by 4.1 percent in September, down from 4.4 percent in August. The following figure shows inflation since 2015 measured by CPI and core CPI.

Reporters Gabriel Rubin and Nick Timiraos, writing in the Wall Street Journalsummarized the prevailing interpretation of this report:

“The latest inflation data highlight the risk that without a further slowdown in the economy, inflation might settle around 3%—well below the alarming rates that prompted a series of rapid Federal Reserve rate increases last year but still above the 2% inflation rate that the central bank has set as its target.”

As we discuss in this blog post, some economists and policymakers have argued that the Fed should now declare victory over the high inflation rates of 2022 and accept a 3 percent inflation rate as consistent with Congress’s mandate that the Fed achieve price stability. It seems unlikely that the Fed will follow that course, however. Fed Chair Jerome Powell ruled it out in a speech in August: “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.”

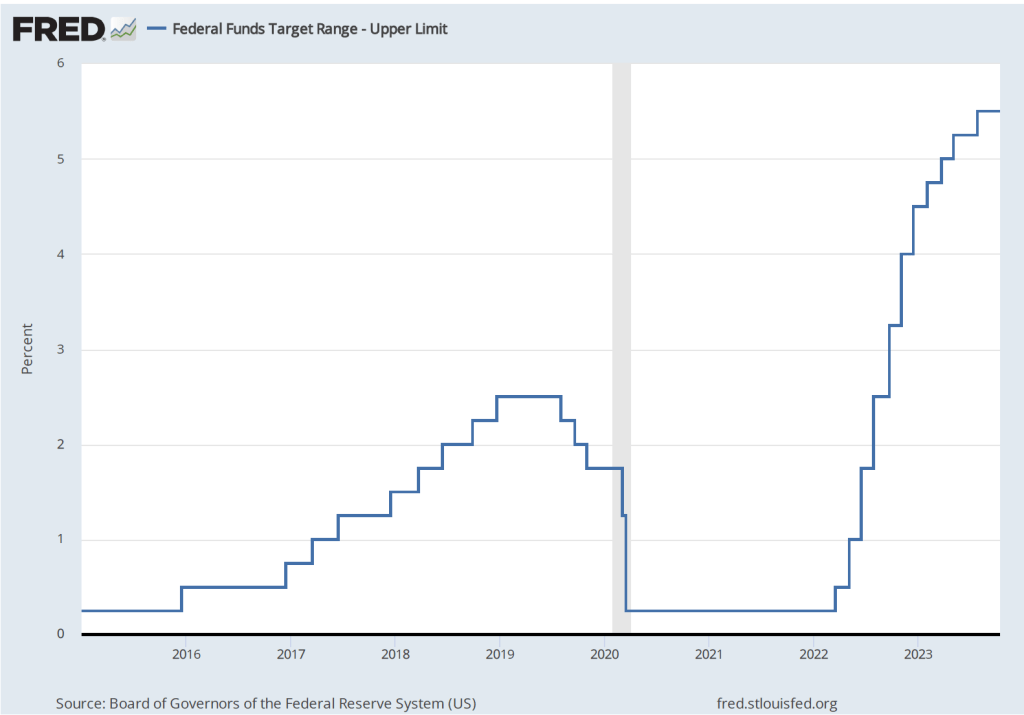

To achieve its goal of bringing inflation back to its 2 percent targer, it seems likely that economic growth in the United States will have to slow, thereby reducing upward pressure on wages and prices. Will this slowing require another increase in the Federal Open Market Committe’s target range for the federal funds rate, which is currently 5.25 to 5.50 percent? The following figure shows changes in the upper bound for the FOMC’s target range since 2015.

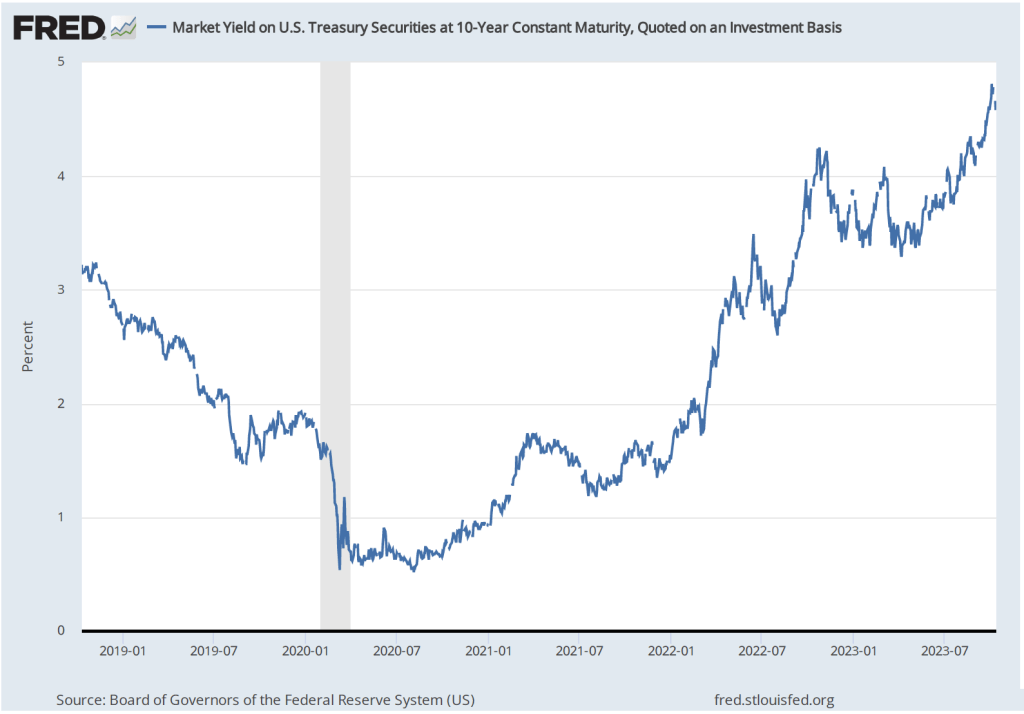

Several members of the FOMC have raised the possibility that financial markets may have already effectively achieved the same degree of policy tightening that would result from raising the target for the federal funds rate. The interest rate on the 10-year Treasury note has been steadily increasing as shown in the following figure. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. In fact, the main way in which monetary policy works is for the FOMC’s increases or decreases in its target for the federal funds rate to result in increases or decreases in long-run interest rates. Higher long-run interest rates typically result in a decline in spending by consumrs on new housing and by businesses on new equipment, factories computers, and software.

Federal Reserve Bank of Dallas President Lorie Logan, who serves on the FOMC, noted in a speech that “If long-term interest rates remain elevated … there may be less need to raise the fed funds rate.” Similarly, Fed Vice-Chair Philip Jefferson stated in a speech that: “I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

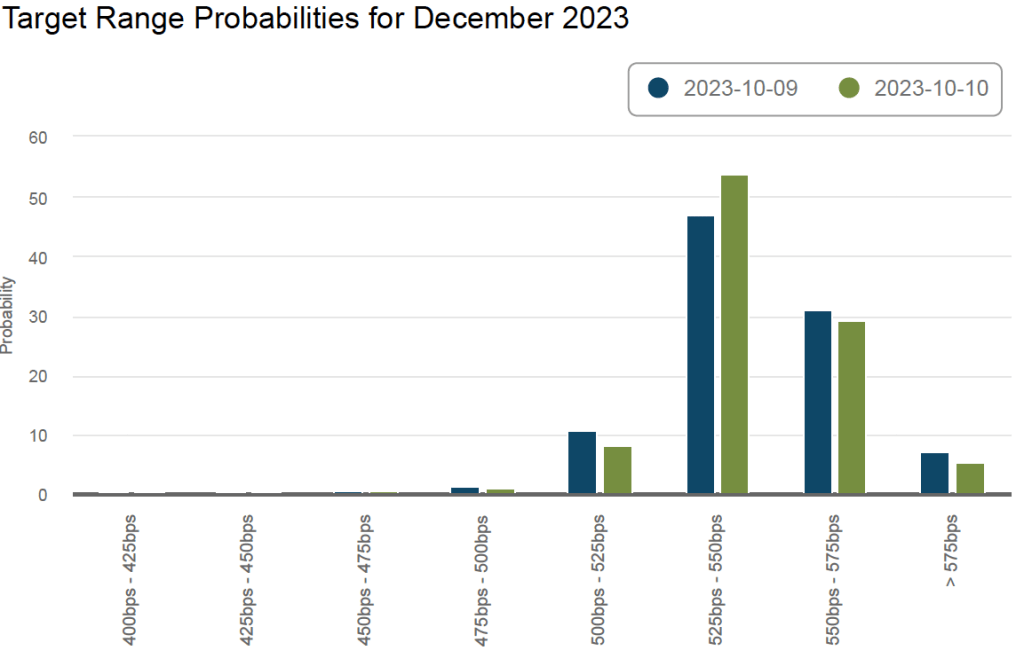

The FOMC has two more meetings scheduled for 2023: One on October 31-November 1 and one on December 12-13. The following figure from the web site of the Federal Reserve Bank of Atlanta shows financial market expectations of the FOMC’s target range for the federal funds rate in December. According to this estimate, financial markets assign a 35 percent probability to the FOMC raising its target for the federal funds rate by 0.25 or more. Following the release of the CPI report, that probability declined from about 38 percent. That change reflects the general expectation that the report didn’t substantially affect the likelihood of the FOMC raising its target for the federal funds rate again by the end of the year.

Sarah Bloom Raskin. (Photo from the Wall Street Journal)Lisa Cook (Photo from Michigan State via the Wall Street Journal)Philip Jefferson (Photo from Davidson College via the Wall Street Journal)

The terms of the seven members of the Fed’s Board of Governors are staggered with a new 14-year term beginning each February 1 of even-numbered years. That system of appointments was intended to limit turnover on the board with the aim of avoiding sudden swings in monetary policy. But because in practice board members often resign before their terms have expired and because presidents sometimes delay making appointments to empty positions, presidents sometimes face the need to make multiple appointments at the same time. In January 2022, President Joe Biden nominated the following three people—one lawyer and two economists—to positions on the board:

Sarah Bloom Raskin is the Colin W. Brown Distinguished Professor of the Practice of Law at Duke University. She served on the Board of Governors from 2010 to 2014 before resigning to become deputy secretary of the Treasury, a position she held until 2017. If confirmed by the Senate, she would serve as the board’s vice chair for supervision, becoming the second person to hold that position, which was established by the 2010 Dodd-Frank Act. The vice chair for supervision has important responsibility in leading the Fed’s regulation and supervision of banks.

Philip Jefferson is the Paul B. Freeland Professor of Economics, vice president for academic affairs, and dean of the faculty at Davidson College. He received his PhD from the University of Virginia in 1990. He previously taught at Swarthmore College and served a year as an economist at the Board of Governors.

Lisa Cook is a professor of economics at Michigan State University. She received her PhD in economics from the University of California, Berkeley in 1997. She served on the Council of Economic Advisers from 2011 to 2012 during the Obama Administration.

Before taking their positions, the three nominees must first be confirmed by the U.S. Senate. At this point, it’s unclear whether any of the three nominees will encounter significant opposition to their confirmation. Senator Pat Toomey of Pennsylvania has raised some concerns about Raskin’s nomination, arguing that she:

“has specifically called for the Fed to pressure banks to choke off credit to traditional energy companies and to exclude those employers from any Fed emergency lending facilities. I have serious concerns that she would abuse the Fed’s narrow statutory mandates on monetary policy and banking supervision to have the central bank actively engaged in capital allocation.”

If confirmed, the nominees will join these other four board members:

Jerome Powell has been nominated by President Biden to a second term as Fed Chair that, if the Senate votes favorably on the nomination, would begin in February 2022. Powell was first nominated to the board by President Obama in 2011 and nominated by President Trump to his first term as chair, which began in February 2018.

Lael Brainard was first nominated to the board by President Obama in 2014. President Biden has nominated Brainard to serve as vice-chair of the board. If confirmed, she would succeed in that position Richard Clarida who resigned in January 2022.

Christopher Waller was nominated by President Trump to a term on the board in 2020. He had previously served as director of research at the Federal Reserve Bank of St. Louis. He received his PhD in economics from Washington State University and served as a professor of economics at Notre Dame University and the University of Kentucky. His term expires in 2030.

Michelle Bowman was nominated by President Trump to a term on the board in 2018. Bowman had served as the state bank commissioner of Kansas and as an executive at a local bank in Kansas. She has a law degree from Washburn University. She was reappointed to a full 14-year term in 2020.

Sources: Senator Toomey’s statement on Sarah Bloom Raskin’s nomination can be found here. An overview of the membership of the Board of Governors can be found here on the Federal Reserve’s website. An Associated Press article covering President Biden’s nominations can be found here.