Silver pennies used in England during the 600s. (Image from Jane Kershaw, et al.)

As economies move from subsistence agriculture towards specialization and trade, the inefficiency of barter exchange pushes them toward developing money. Any commodity that is widely accepted in payment for goods and services—that is, any commodity that can function as a medium of exchange—can be used as money. As we discuss in a recent blog post, in frontier America animal hides were used as money. In a World War II German prisoner of war camp, the British prisoners used cigarettes as money. Most economies made a transition from using commodities like animal skins to using coins made of precious metals, such as copper, silver, and gold. (We discuss the development of money in Macroeconomics, Chapter 14, Section 14.1, Economics, Chapter 24, Section 24.1, and Essentials of Economics, Chapter 16, Section 16.1.)

Coins were typically minted by kings, local warlords, bishops, or other people with control over a sufficient sized territory to make minting coins worthwhile. Where did they get the metal needed to mint coins? During the height of the gold standard in the 1800s and early 1900s, governments could rely on supplies of precious metals from domestic mines or from trade with other countries. In earlier periods, access to sufficient supplies of precious metals could be more difficult.

A recent academic paper by Jane Kershaw, of the University of Oxford; Stephen W. Merkel and Paolo D’Imporzano, of Vrije Universiteit Amsterdam; and Rory Naismith the University of Cambridge, examined the case of coins minted by kings of England during the year 660 to 820. During the time from the year 43 to the year 409, most of modern England and Wales was part of the Roman Empire. (A non-technical summary of the paper, with a video, is here. A timeline of Roman Britain is here.) During that time, the Roman province of Britannia used the same gold, silver, and copper coins used throughout the empire. After the withdrawal of the last Roman legions, England experienced waves of invasions from Saxons, Angles, and other Germanic tribes that destroyed most of Roman civilization on the island. Very few written records have survived from 409 through the end of the 500s. But it’s likely that few, if any, coins were minted during this period.

As trade within England began to revive in the second half of the 600s, the demand for coins increased. Given the inefficiency of barter, the absence of a sufficient supply of coins would have hobbled the growth of trade. With more than 200 years having passed since the end of Roman rule, Roman coins were no longer available in significant quantities. The increased demand for coins was met by silver pennies, like those shown in the photo at the top of this post.

Where did the rulers of the various English kingdoms get the silver to mint pennies, given that there were no known silver mines operating during this period? Searching for clues, Jane Kershaw and her colleagues analyzed the composition of the silver used in the pennies. Surprisingly, the silver turned out to have the same composition as silver used in the Byzantine Empire in the eastern Mediterranean. Because in this period there was little to no trade between England and the Byzantine Empire, Kershaw and colleagues believe that the silver was likely obtained from melting silver objects, like the plate shown above, obtained from trade with the Byzantine Empire in earlier periods.

The work of these researchers has provided insight into an historical example of governments supplying the money needed to facilitate the transition away from barter.

Counterfeit 1899 Peruvian dinero. (Image from Luis Ortega-San-Martín and Fabiola Bravo-Hualpa article.)

What counts as money is an interesting topic. For instance, in Macroeconomics, Chapter 14, Section 14.2 (Economics, Chapter 24, Section 24.2, and Essentials of Economics, Chapter 16, Section 16.2), we discuss whether bitcoin is money (spoiler alert: it isn’t).

Of the four functions of money that we discuss in Chapter 14, the most important is that money serves as a medium of exchange. Anything can be used as money if most people are willing to accept it in exchange for goods and services. In that chapter, we mention that at one time in West Africa cowrie shells were used as money. In the early years of the United States, animal skins were sometimes used as money. For instance, the first governor of Tennessee received an annual salary of 1,000 deerskins.

In a famous article in the academic journal Economica, economist Richard A. Radford who had been captured in 1942 by German troops while fighting with the British Army in North Africa described his experiences in a prisoner-of-war camp. The British prisoners in the camp developed an economy in which cigarettes were used as money:

“Everyone, including nonsmokers, was willing to sell for cigarettes, using them to buy at another time and place. Cigarettes became the normal currency .… Laundrymen advertised at two cigarettes a garment …. There was a coffee stall owner who sold tea, coffee or cocoa at two cigarettes a cup, buying his raw materials at market prices and hiring labour ….”

In Chapter 24, in end of chapter problem 1.8, we note that according to historian Peter Heather, during the time of the Roman Empire, German tribes east of the Rhine river used Roman coins as money even though Rome didn’t govern that area. Roman coins were apparently also used as money in parts of India during those years even though the nearest territory the Romans controlled was hundreds of miles to the west. Again we have an example of something—roman coins in this case—being used as money because people were willing to aceept it in exchange for goods and services even though the government that issued the coins didn’t control that area.

Even more striking case is the case of Iraqi paper currency issued by the government of Saddam Hussein. This currency continued to circulate even after Saddam’s government had collapsed following the invasion of Iraq by U.S. and British troops. U.S. officials in Iraq had expected that as soon as the war was over and Saddam had been forced from power, the currency with his picture on it would lose all its value. This result had seemed inevitable once the United States had begun paying Iraqi officials in U.S. dollars. However, for some time many Iraqis continued to use the old currency because they were familiar with it. According to an article in the Wall Street Journal, the Iraqi manager of a currency exchange put it this way: “People trust the dinar more than the dollar. It’s Iraqi.” In fact, for some weeks after the invasion, increasing demand for the dinar caused its value to rise against the dollar. Eventually, a new Iraqi government was formed, and the government ordered that dinars with Saddam’s picture be replaced by a new dinar. Again we see that anything can be used as money as long as people are willing to accept it in exchange for goods and services, even paper currency issued by a government that no longer exists.

Finally, there is the case of the coin shown at the beginning of this post. The coin looks like the dineros—small denomination silver coins—issued by the Peruvian government. But the coin is dated 1899, a year in which the Peruvian government did not issue any dineros. An analysis of one of these coins by Luis Ortega-San-Martín, Fabiola Bravo-Hualpa, and their students at the Pontifical Catholic University of Peru showed that it was made of copper, nickel, and zinc, in contrast to deniros from other years, which where made primarily of silver with a small amount of copper. They concluded that the coin was a counterfeit made around 1900:

“It is our belief that this counterfeit coin was not made as a numismatic rarity to deceive modern collectors … but rather to be used as current money (its worn state indicates ample use) …. [C]ounterfeiters usually make common coins that do not draw attention expecting them to pass unnoticed.”

In other words, as long as people are willing to accept counterfeit coins—which they likely will do if they do not recognize them as being counterfeit—they can serve as money. In fact, even if coins are easily recognizable as being counterfeit, they might still be used as money—particularly in a time and place where there is a shortage of government issued coins. In the British North American colonies, there was frequently a shortage of coins. Some people would clip small amounts off gold and silver coins, either selling the metal or having it minted into coins. The clipped coins, while not actually counterfeit, contained less precious metal than did unclipped coins, yet they continued to be used in buying and selling because of the general shortage of coins.

An Automated Teller Machine (ATM) located in Egypt that dispenses gold bars rather than currency. (Photo from ahrm.org.)

A recent article in the New York Times (available here, but a subscription may be required) discusses how consumers in Egypt are dealing with inflation. According to statistics from the International Monetary Fund, consumer prices in Egypt rose 23.5 percent in 2023 and are projected to increase by 32.2 percent in 2024, although in early 2024 inflation may have been running at an annual rate of 50 percent. In response to the inflation, many Egyptian businesses have begun quoting prices in U.S. dollars rather than in Egyptian pounds. The value of the Egyptian pound has declined from about 18 pounds to the U.S. dollar in early 2022 to about 48 pounds to the dollar today. In practice, many Egyptian consumers can have difficulty obtaining dollars except on the black market, where the exchange rate is generally worse than the rate quoted by the Egyptian central bank.

According to the article, many Egyptians, losing faith in value of the pound and unable to easily obtain U.S. dollars, have turned to gold as a potentially “safe financial harbor.” The article notes that: “The market [for gold] grew so fevered that the government announced in November that it was partnering with a financial technology company to install A.T.M.s [Automated Teller Machines] that would dispense gold bars instead of cash.” That ATM is shown in the photo above.

This episode raises two questions:

Is gold a good hedge (a “safe harbor”) against inflation?

Are ATMs that dispense gold rather than currency a good idea?

As we discuss in Chapter 14, Section 14.3 of Money, Banking, and the Financial System, gold has not been a good hedge against inflation for U.S. investors. Although many people believe that the price of gold can be relied on to increase if the general price level increases, in fact, the data show that the price of gold can’t be counted on to keep up with increases in the general price level. In the following figure, the blue line shows the market price of gold during each month since January 1976. The red line shows the real price of gold, which is calculated by dividing the nominal price of gold by the consumer price index (CPI). (For convenience, we set the value of the CPI equal to 100 in January 1976.) The price of gold is measured in dollars per ounce.

The figure shows that the market price of gold can fall even as the price level rises. For example, the price of gold rose from $132 per ounce in January 1976 to $670 per ounce in September 1980. As a result, during that period the real price of gold more than tripled, and holding gold during this period was a good hedge against inflation. Unfortunately, the market price of gold then went into a long decline and didn’t again reach its September 1980 value until April 2007, a period during which the CPI more than doubled. In other words, over this more than 25-year period gold provided no hedge at all against the effects of inflation. Consumers in India today shouldn’t count on buying gold as way to protect the real value of their savings from being reduced by inflation.

The New York Times article refers to only a single ATM in Egypt that dispenses gold bars rather than Egyptian pounds. Would we expect that the number of these ATMs will increase in Egypt and other countries experiencing very high inflation rates? Does the existence of these ATMs indicate that people in Egypt are now—or will likely begin—using gold bars rather than currency for routine buying and selling?

The answer to both questions is likely “no.” Although the article refers to an “ATM,” it might be better to think of this facility as instead being a vending machine. Similar ATMs/vending machines that dispense gold bars are available in the United States (as indicated here, here, and here), and, most likely, in other countries as well.

We usually think of vending machines as selling soda and water or snacks. But there are many vending machines that sell other products as well. For instance, most large airports have vending machines that sell small electronic products, such as cell phone batteris or earphones. The term ATM is usually reserved for machines that enable people who have deposits at a bank or other financial firms to withdraw currency. So, the article seems to be describing something that is more a vending machine than an ATM. The article discusses the many small businesses in Egypt that buy and sell gold, which makes it likely that most consumers will continue to rely on those businesses rather than on a machine when they want to buy and sell gold.

It seems unlikely that people in Egypt will beging using gold bars for routine buying and selling—that is, using gold as a medium of exchange. Most goods in Egypt have their prices denominated in either Egyptian pounds or in U.S. dollars or in both. Anyone attempting to buy goods with gold bars would need first to determine the market price of gold at that time before making the purchase and would have to locate a seller who was willing to accept gold in exchange for their goods. In effect, sellers would be engaging in two transactions at the same time: buying gold from the buyer and selling goods to the buyer. Although in a time of high inflation a seller takes on the risk that currency he accepts for a purchase may decline in value while the seller is holding it, a seller accepting gold also takes on the risk that the market price of gold may fall while the seller is holding it.

It’s interesting that the Egyptian government reacted to consumers buying gold as a hedge against inflation by partnering with a financial firm to make available an “ATM” that dispenses gold bars. But it probably doesn’t represent a significant development in the Egyptian financial system.

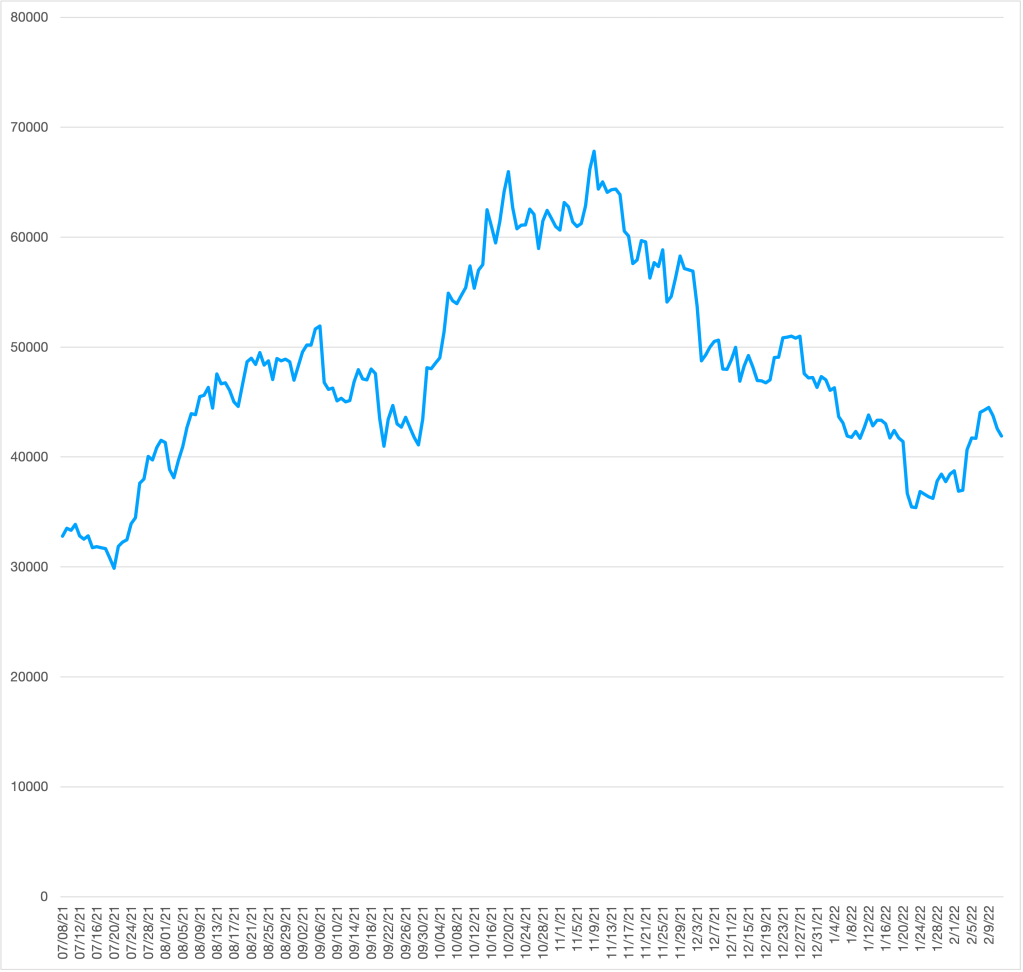

Bitcoin has failed in their original purpose of providing a digital currency that could be used in everyday transactions like buying lunch and paying a cellphone bill. As the following figure shows, swings in the value of bitcoin have been too large to make useful as a medium of exchange like dollar bills. During the period shown in the figure—from July 2021 to February 2022—the price of bitcoin has increased by more than $30,000 per bitcoin and then fallen by about the same amount. Bitcoin has become a speculative asset like gold. (We discuss bitcoin in the Apply the Concept, “Are Bitcoins Money?” which appears in Macroeconomics, Chapter 14, Section 14.2 and in Economics, Chapter 24, Section 24.2. In an earlier blog post found here we discussed how bitcoin has become similar to gold.)

The vertical axis measures the price of bitcoin in dollars per bitcoin.

The Slow U.S. Payments Increases the Appeal of a Digital Currency

Some economists and policymakers argue that there is a need for a digital currency that would do what bitcoin was originally intended to do—serve as a medium of exchange. Digital currencies hold the promise of providing a real-time payments system, which allow payments, such as bank checks, to be made available instantly. The banking systems of other countries, including Japan, China, Mexico, and many European countries, have real-time payment systems in which checks and other payments are cleared and funds made available in a few minutes or less. In contrast, in the United States, it can two days or longer after you deposit a check for the funds to be made available in your account.

The failure of the United States to adopt a real-time payments system has been costly to many lower-income people who are likely to need paychecks and other payments to be quickly available. In practice, many lower-income people: 1) incur bank overdraft fees, when they write checks in excess of the funds available in their accounts, 2) borrow money at high interest rates from payday lenders, or 3) pay a fee to a check cashing store when they need money more quickly than a bank will clear a check. Aaron Klein of the Brookings Institution estimates that lower-income people in the United States spend $34 billion annually as a result of relying on these sources of funds. (We discuss the U.S. payments system in Money, Banking, and the Financial System, 4th edition, Chapter 2, Section 2.3.)

The Problem with Stablecoins as Money

Some entrepreneurs have tried to return to the original idea of using cryptocurrencies as a medium of exchange by introducing stablecoins that can be bought and sold for a constant number of dollars—typically one dollar for one stablecoin. The issuers of stablecoins hold in reserve dollars, or very liquid assets like U.S. Treasury bills, to make credible the claim that holders of stablecoins will be able to exchange them one-for-one for dollars. Tether and Circle Internet Financial are the leading issuers of stablecoins.

So far, stablecoins have been used primarily to buy bitcoin and other cryptocurrencies rather than for day-to-day buying and selling of goods and services in stores or online. Financial regulators, including the U.S. Treasury and the Federal Reserve, are concerned that stablecoins could be a risk to the financial system. These regulators worry that issuers of stablecoins may not, in fact, keep sufficient assets in reserve to redeem them. As a result, stablecoins might be susceptible to runs similar to those that plagued the commercial banking system prior to the establishment of the Federal Deposit Insurance Corporation in the 1930s or that were experienced by some financial firms during the 2008 financial crisis. In a run, issuers of stablecoins might have to sell financial assets, such as Treasury bills, to be able to redeem the stablecoins they have issued. The result could be a sharp decline in the prices of these assets, which would reduce the financial strength of other firms holding the assets.

In 2019, Facebook (whose corporate name is now Meta Platforms) along with several other firms, including PayPal and credit card firm Visa, began preparations to launch a stablecoin named Libra—the name was later changed to Diem. In May 2021, the firms backing Diem announced that Silvergate Bank, a commercial bank in California, would issue the Diem stablecoin. But according to an article in the Wall Street Journal, the Federal Reserve had “concerns about [the stablecoin’s] effect on financial stability and data privacy and worried [it] could be misused by money launderers and terrorist financiers.” In early 2022, Diem sold its intellectual property to Silvergate, which hoped to still issue the stablecoin at some point.

A Federal Reserve Digital Currency?

If private firms or individual commercial banks have not yet been able to issue a digital currency that can be used in regular buying and selling in stores and online, should central banks do so? In January 2022, the Federal Reserve issued a report discussing the issues involved with a central bank digital currency (CBCD). As we discuss in Macroeconomics, Chapter 14, Section 14.2, most of the money supply of the United States consists of bank deposits. As the Fed’s report points out, because bank deposits are computer entries on banks’ balance sheets, most of the money in the United States today is already digital. As we discuss in Section 14.3, bank deposits are liabilities of commercial banks. In contrast, a CBCD would be a liability of the Fed or other central bank.

The Fed report lists the benefits of a CBCD:

“[I]t could provide households and businesses [with] a convenient, electronic form of central bank money, with the safety and liquidity that would entail; give entrepreneurs a platform on which to create new financial products and services; support faster and cheaper payments (including cross-border payments); and expand consumer access to the financial system.”

Importantly, the Fed indicates that it won’t begin issuing a CBCD without the backing of the president and Congress: “The Federal Reserve does not intend to proceed with issuance of a CBDC without clear support from the executive branch and from Congress, ideally in the form of a specific authorizing law.”

The Fed report acknowledges that “a significant number of Americans currently lack access to digital banking and payment services. Additionally, some payments—especially cross-border payments—remain slow and costly.” By issuing a CBDC, the Fed could help to reduce these problems by making digital banking services available to nearly everyone, including lower-income people who currently lack bank checking accounts, and by allowing consumers to have payments instantly available rather than having to wait for a check to clear.

The report notes that: “A CBDC would be the safest digital asset available to the general public, with no associated credit or liquidity risk.” Credit risk is the risk that the value of the currency might decline. Because the Fed would be willing to redeem a dollar of CBDC currency for a dollar or paper money, a CBDC has no credit risk. Liquidity risk is the risk that, particularly during a financial crisis, someone holding CBDC might not be able to use it to buy goods and services or financial assets. Fed backing of the CBDC makes it unlikely that someone holding CBDC would have difficulty using it to buy goods and services or financial assets.

But the report also notes several risks that may result from the Fed issuing a CBDC:

Banks rely on deposits for the funds they use to make loans to households and firms. If large numbers of households and firms switch from using checking accounts to using CBDC, banks will lose deposits and may have difficulty funding loans.

If the Fed pays interest on the CBDC it issues, households, firms, and investors may switch funds from Treasury bills, money market mutual funds, and other short-term assets to the CBDC, which might potentially disrupt the financial system. Money market mutual funds buy significant amounts of corporate commercial paper. Some corporations rely heavily on the funds they raise from selling commercial paper to fund their short-term credit needs, including paying suppliers and financial inventories.

In a financial panic, many people may withdraw funds from commercial bank deposits and convert the funds into CBDC. These actions might destabilize the banking system.

A related point: A CBDC might result in large swings in bank reserves, particularly during and after a financial panic. As we discuss in Macroeconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Section 24.4), increasing and decreasing bank reserves is one way in which the Fed carries out monetary policy. So fluctuations in bank reserves may make it more difficult for the Fed to conduct monetary policy, particularly during a financial panic. (This consideration is less important during times like the present when banks hold very large reserves.)

Because the Fed has no experience in operating a retail banking operation, it would be likely that if it began issuing a CBDC, it would do so through commercial banks or other financial firms rather than doing so directly. These financial firms would then hold customers CBDC accounts and carry out the actual flow of payments in CBDC among households and firms.

The report notes that the Fed is only beginning to consider the many issues that would be involved in issuing a CBDC and still needs to gather feedback from the general public, financial firms, nonfinancial firms, and investors, as well as from policymakers in Washington.

Sources: Peter Rudegeair and Liz Hoffman, “Facebook’s Cryptocurrency Venture to Wind Down, Sell Assets,” Wall Street Journal, January 26, 2022; Liana Baker, Jesse Hamilton, and Olga Kharif, “Mark Zuckerberg’s Stablecoin Ambitions Unravel with Diem Sale Talks,” bloomberg.com, January 25, 2022; Amara Omeokwe, “U.S. Regulators Raise Concern With Stablecoin Digital Currency,” Wall Street Journal, December 17, 2022; Jeanna Smialek, “Fed Opens Debate over a U.S. Central Bank Digital Currency with Long-Awaited Report,”, January 20, 2022; Board of Governors of the Federal Reserve System, Money and Payments: The U.S. Dollar in the Age of Digital Transformation, January 2022; and Aaron Klein, “The Fastest Way to Address Income Inequality? Implement a Real Time Payments System,” brookings.edu, January 2, 2019.