Image of an apartment house under construction generated by ChatGTP 4o.

In Chapter 1, we discuss one of our three key economic ideas: “People respond to economic incentives.” When government policymakers ignore this idea, government programs can fail to meet their goals as the following example shows.

In April 2024, to spur construction of new apartment houses, the New York state legislature enacted the Affordable Neighborhoods for New Yorkers program. The program includes what’s known as the 485-x tax break for apartment house builders. The details of the program are complex but basically a builder can have a new apartment house exempted from property taxes for up to 40 years provided that the building includes a specified number of apartments set aside for people with lower incomes. Some members of the state legislature believe that developers of larger apartment houses are typically better able to pay higher wages than are developers of smaller apartment houses. So, the legislation contained a provision that builders of projects with 100 or more units must pay construction workers at least $40 per hour.

An article in Crain’s New York Business reported today on newly released data on developers registering an interest in participating in the program. The developers proposed building 118 apartment houses. (The developers can register an interest in the program, but aren’t formally awarded the tax break until after the projects are finished.) None of the projects would have 100 or more units; three projects will have 99 units. Not too surprisingly, developers have responded to the law by building smaller apartment houses rather than larger apartment houses that would require them to pay higher construction wages. The higher wages are also required for any project built south of 96th Street in the New York City borough of Manhattan. Again, unsurprisingly, only 2 of the 118 proposed projects are located in that part of the city. Although it was not the intent of the state legislature, the law provided an economic incentive to build smaller apartment houses outside of Manhattan and builders responded to that incentive.

The article quotes the president of the Real Estate Board of New York (REBNY) as saying: “The absence of the larger projects we need at scale to meet the city’s production goals was identified early on by REBNY as a likely outcome of the new program design.”

The article is here, although a subscription may be required.

In Chapter 1, Section 1.1, one of our three key economic ideas is that people respond to economic incentives. Government policy can change the economic incentives that people face. Sometimes a government policy can have unintended consequences because it changes economic incentives in a way that policymakers didn’t anticipate. Some economists argue that this was the case with the Biden administration’s decision to change the federal student loan program.

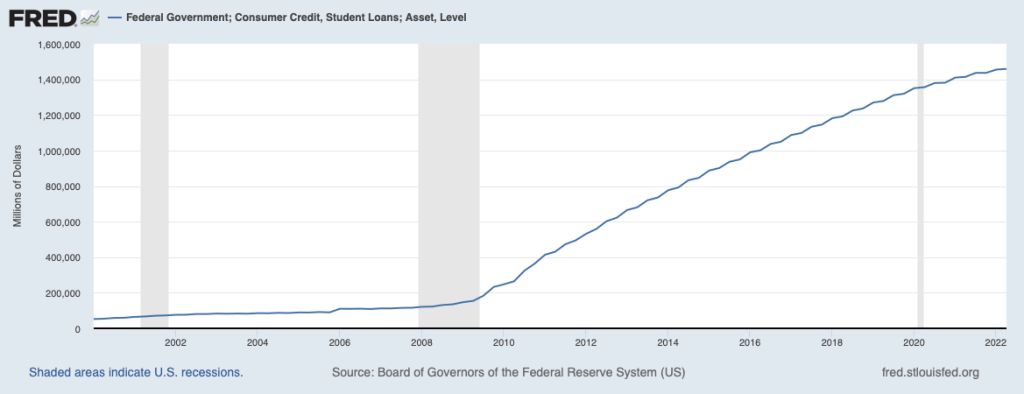

In recent years, college students and their parents have rapidly increased their loan debt. The following figure shows the total value of outstanding student loans beginning in 2000. Student loan debt increased from about $52 billion in 2000 to about $1.6 trillion in 2022. Or, put another way, for every dollar of loan debt students and their parents owed in 2000, they owed more than 27 dollars of debt in 2022. In 2022, the average borrower owed about $37,000.

During the Covid–19 pandemic, the Trump and Biden administrations allowed people with student loans to suspend making payments on them. The payment moratorium began March 31, 2020 and is scheduled to end on December 31, 2022. Student loan payments are often the largest item in the budgets of recent college graduates. Some economists argue that the need to make student loan payments has made it harder for young adults to accumulate the down payments necessary to buy homes. As a result, young adults are likely to delay forming families, thereby reducing their need to move from an apartment to a house. In 1967, about 83 percent of people aged 25 to 34 lived with a spouse or partner, while in 2021 only about 54 percent did.

Some economists doubt that student loan debt explains the delay in young adults forming families and buying houses. But many policymakers have seen reducing the burden of student loan debt on young adults as an important issue. In August 2022, President Joe Biden announced a plan under which individuals earning less than $125,000 per year would have up to $10,000 in student loan debt cancelled. Borrowers with Pell grants would have up to another $10,000 cancelled. A second part of the plan involved changes to the federal government’s income-driven repayment (IDR) program. As a result of these changes, lower and middle-income student loan borrowers will be able to more easily have their loan balances canceled. With some exceptions, borrowers who have loans of $12,000 or less will have their loans canceled after making payments for 10 years, rather than the current 20 years. The annual payments for most borrowers using the IDR program will be lowered to 5 percent of their income above about $33,000 per year, rather than the previous 10 percent.

Some policymakers objected to President Biden’s plan, arguing that it was unconstitutional because it was the result of a presidential executive order rather than the result of Congressional legislation. Many economists focused on a different potential problem with the plan: the economic incentives that might result from the changes to the IDR program. The intention of these changes was to reduce the burden on people who currently have student loans, but the changes also affected the economic incentives facing students applying for loans and colleges in deciding the level of tuition to charge.

In an article on the Brookings Institution website, Adam Looney, a professor of finance at the University of Utah, argued that because of the changes to the IDR program, the typical college student could expect to pay back only about 50 percent of the amount borrowed. Before the changes, the Congressional Budget Office had estimated that the typical student would end up paying more than 100 percent of the amount borrowed because the student would have to pay interest on the loan amount. Looney argues that students and their parents will have an incentive to borrow more because they will expect to pay back only half of the amount borrowed. In particular, he notes:

“A large share of student debt is not used to pay tuition, but is given to students in cash for rent, food, and other expenses…. While students certainly need to pay rent and buy food while in school, under the administration proposal a student can borrow significant amounts for ‘living expenses,’ deposit the check in a bank account, and not pay it all back…. Some people will use loans like an ATM, which will be costly for taxpayers and is certainly not the intended use of the loans.”

Sylvain Catherine, a professor of finance at the University of Pennsylvania’s Wharton School, makes a similar argument: “How can we not anticipate the distortionary effects of such a policy? Student will be encouraged to take more debt since they will not have to repay the marginal dollar, and colleges will have an incentive to further increase tuition.” An article in the New York Times noted that taxpayers will be responsible for the value of student loans that aren’t paid back: “By offering more-generous educational subsidies, the government may be creating a perverse incentive for both schools and borrowers, who could begin to pay even less attention to the actual price tag of their education—and taxpayers could be left footing more of the bill.”

It’s too early to judge the extent to which students, their families, and colleges will react to the changed incentives in President Biden’s student debt relief plan. But because the plan changes economic incentives, it may result in consequences not intended by President Biden and his advisers. (Note that the lawsuits challenging the plan’s constitutionality have also not yet been resolved.)

Sources: Adam Looney, “Biden’s Income-Driven Repayment Plan Would Turn Student Loans into Untargeted Grants,” brookings.edu, September 15, 2022; Gabriel T. Rubin and Amara Omeokwe, “Biden’s Student-Debt-Forgiveness Plan May Cost Up to $1 Trillion, Challenging Deficit Goals,” Wall Street Journal, September 5, 2022; Stacey Cowley, “Student Loan Subsidies Could Have Dangerous, Unintended Side Effects,” New York Times, September 19, 2022; Ron Lieber, “Why Aren’t Student Loans Simple? Because This Is America,” New York Times, September 3, 2022; Congressional Budget Office, “Federal Student Loan Programs, Baseline Projections,” May 2022; U.S. Census Bureau, “Historical Living Arrangements of Adults,” Table AD-3, November 2021; and Federal Reserve Bank of St. Louis FRED data set.