When inflation began to accelerate in the spring of 2022, the highly unusual situation in the U.S. labor market was one of the reasons. This morning (July 2), the Bureau of Labor Statistics (BLS) released its “Job Openings and Labor Turnover” (JOLTS) report for May 2024. The report proivided more data indicating that the U.S. labor market is continuing its return to pre-pandemic conditions.

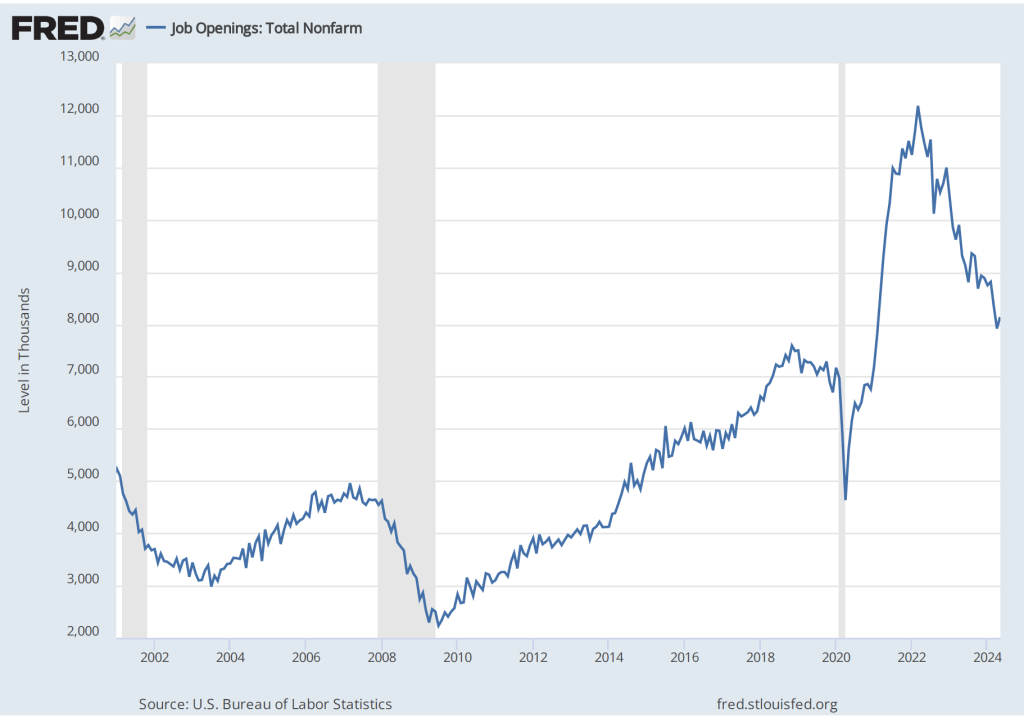

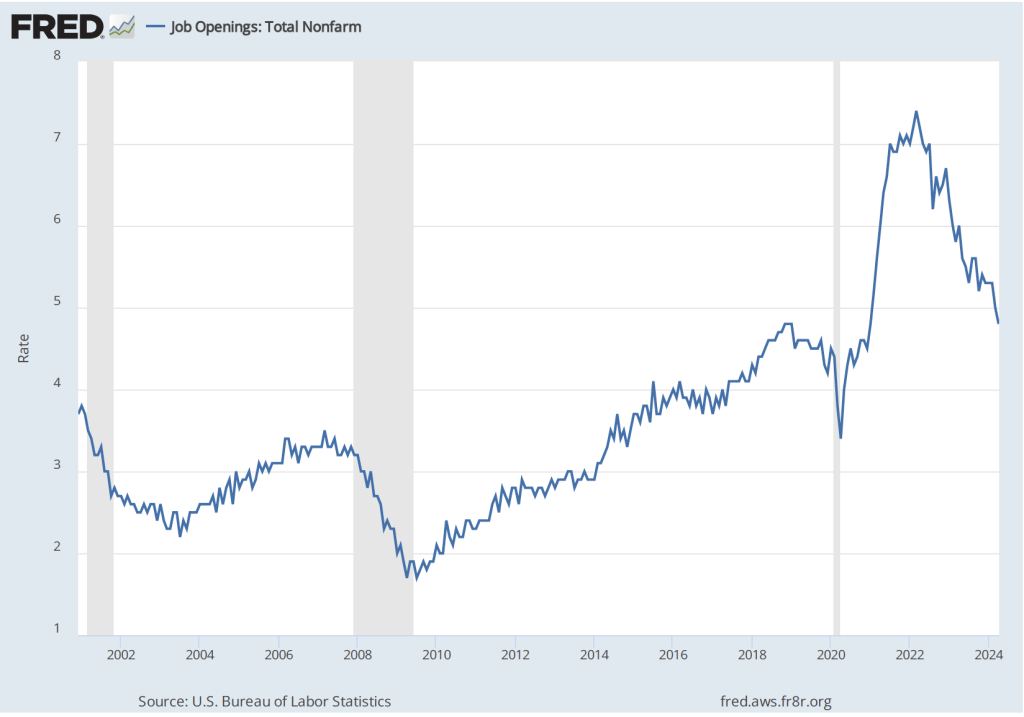

The following figures shows the total number of job openings. The BLS defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. Although the total number of job openings, at 8.1 million, is still somewhat above pre-pandemic levels, it has been gradually declining since reaching a peak of 12.2 million in March 2022.

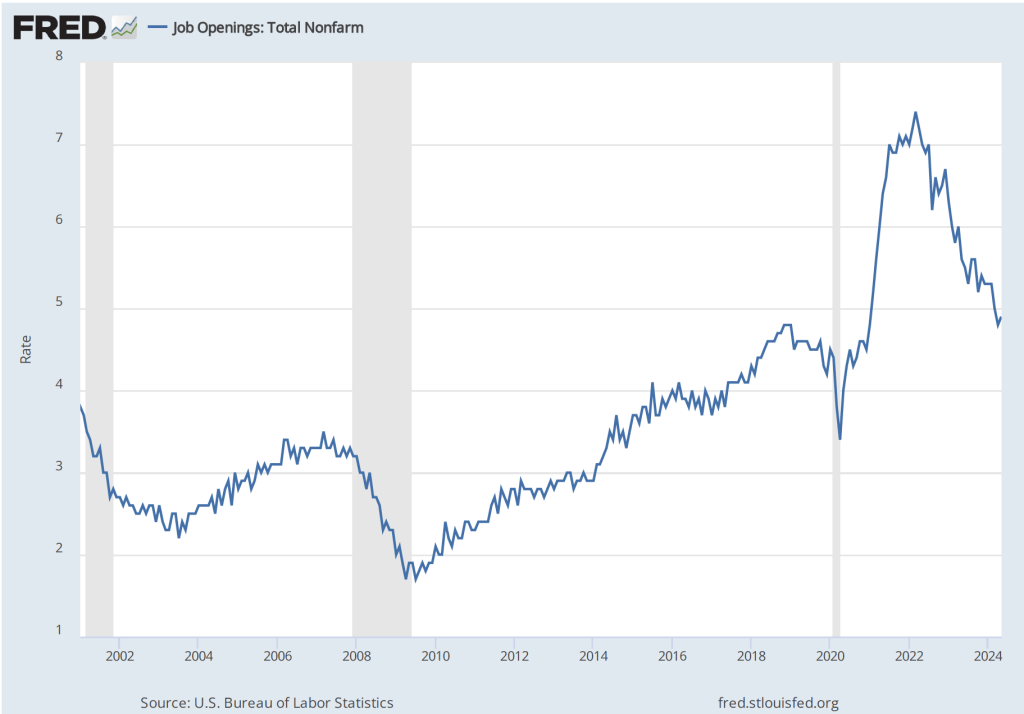

The next figure shows that, at 4.9 percent, the rate of job openings has continued its slow decline from 7.4 percent in March 2022. The rate in May was just slightly above the rate in January 2019, although it was till above the rates during most of 2019 and early 2020, as well as the rates during most of the period following the Great Recession of 2007–2009. The rate of job openings is defined by the BLS as the number of job openings divided by the number of job openings plus the number of employed workers, multiplied by 100.

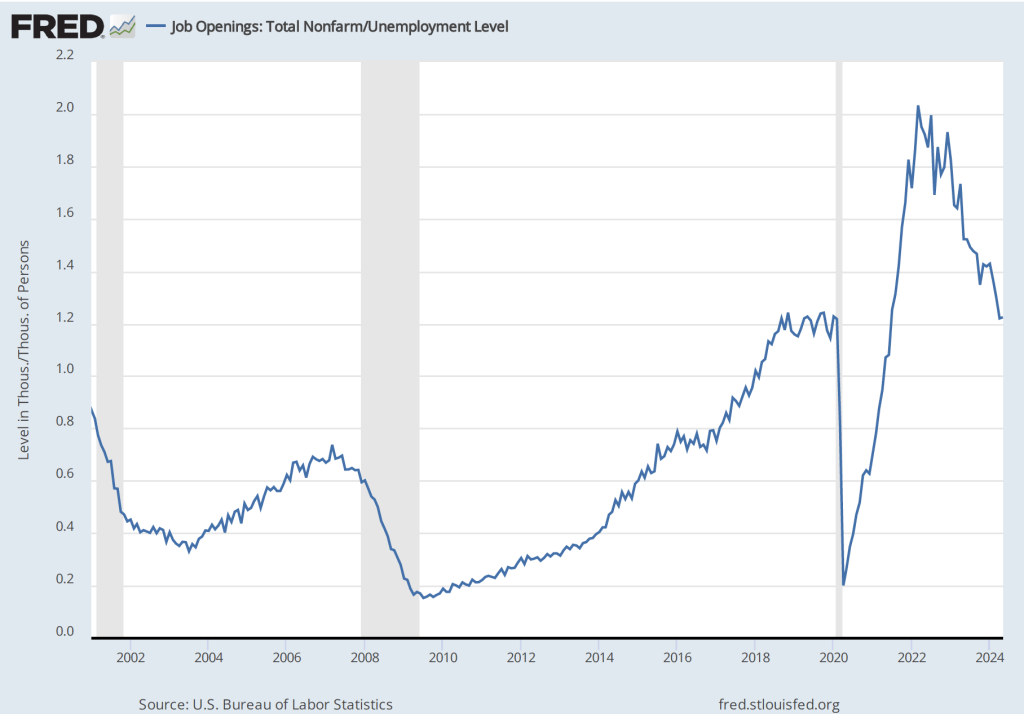

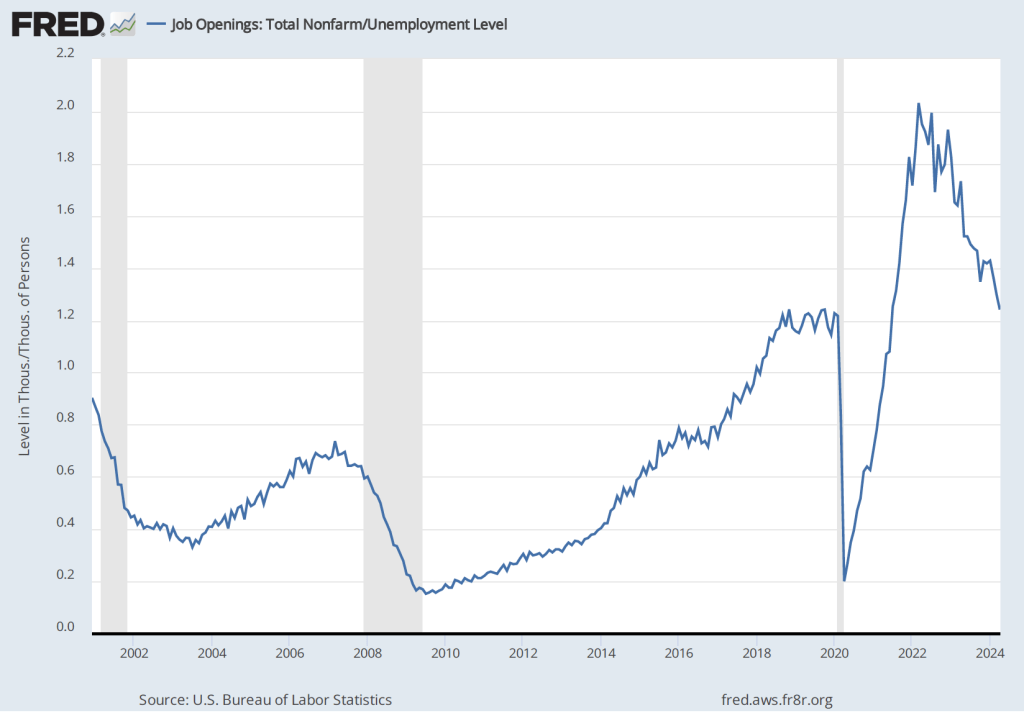

In the following figure, we compare the total number of job openings to the total number of people unemployed. The figure shows a slow decline from a peak of more than 2 job openings per unemployed person in the spring of 2022 to 1.2 job openings per employed person in May 2024—the same as in April and about the same as in 2019 and early 2020, before the pandemic. Note that the number is still above 1.0, indicating that the demand for labor is still high, although no higher than during the strong labor market of 2019.

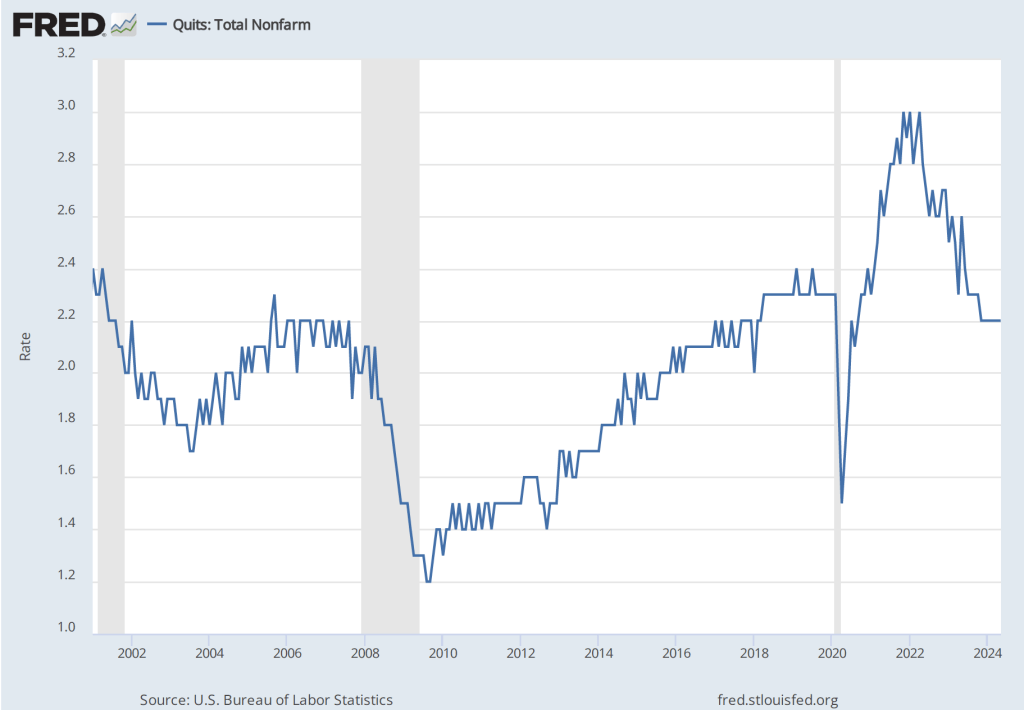

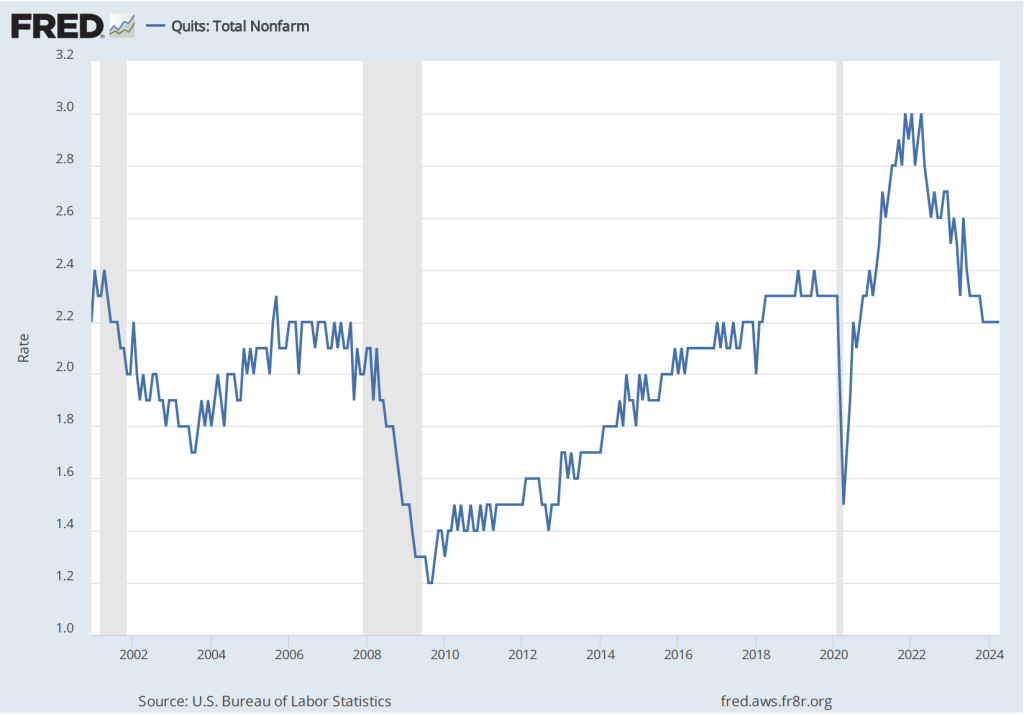

The rate at which workers are willing to quit their jobs is an indication of how they perceive the ease of finding a new job. As the following figure shows, the quit rate declined slowly from a peak of 3 percent in late 2021 and early 2022 to 2.2 percent in November 2023, where it has remained through May 2024. That rate is slightly below the rate during 2019 and early 2020. By this measure, workers perceptions of the state of the labor market seem largely unchanged in recent months.

The JOLTS data indicate that the labor market is about as strong as it was in the months priod to the start of the pandemic, but it’s not as historically tight as it was through most of 2022 and 2023. Speaking today at a conference hosted by the European Central Bank, Fed Chair Jerome Powell was quoted as saying that the Fed had made “a lot of progress” in reducing inflation and that the labor market had made “a pretty substantial” move toward a better balance between labor demand and labor supply.

On Friday morning, the BLS will release its “Employment Situation” report for June, which will provide additional data on the state of the labor market. (Note that the data in the JOLTS report lag the data in the “Employment Situation” report by one month.)

Supports: Microeconomics and Economics, Chapter 6, and Essentials of Economics, Chapter 7.

Photo from the New York Times.

An article in the Wall Street Journal reported that Starbucks during certain periods is cutting by 50 percent the prices of many of its coffees, including its Frappuccino. The article also noted that: “Many restaurant chains are pumping out new deals this year in a bid to reverse weak traffic.” The article also quoted a Starbucks spokesman as saying that Starbucks is cutting prices “to ensure that consumers who are facing a challenging economic environment continue to visit its cafes.”

What is Starbucks likely assuming about the price elasticity of demand for Frappuccinos?

Suppose that after cutting its price of Frappuccinos by 50 percent, the quantity of Frappuccinos sold increases by 20 percent. Ignoring any information other than the values of the price cut and the quantity increase, calculate the price elasticity of demand for Frappuccinos. Considering only the value of the price elasticity of demand you calculated, will Starbucks earn more revenue or less revenue from selling Frappuccions as a result of the price cut? Briefly explain.

Suppose that during the time that Starbucks cuts the price of Frappuccinos, competing coffee houses also cut the prices of their coffees. How will this fact affect your answer to part b.? Briefly explain.

Does the fact that, because of inflation, some consumers are facing a “challenging economic environment” affect your answer to part b.? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the determinants of the price elasticity of demand and the effect of the value of the price elasticity of demand on a firm’s revenue following a price change, so you may want to review Chapter 6, Section 6.2 and Section 6.3.

Step 2: Answer part a. by explaining what Starbucks is likely assuming about the price elasticity of demand for Frappuccinos. Starbucks appears to be assuming that the demand for Frappuccions is price elastic, in which case a cut in the price will result in a more than proportional increase in the quantity of Frappuccions demanded.

Step 3: Answer part b. by using the values given to calculate the price elasticity of demand for Frappuccions and explain whether as a result of the price cut Starbucks will earn more or less revenue from selling Frappuccinos.If all other factors affecting the demand for a product are held constant, the price elasticity of demand equals the percentage change in the quantity demanded divided by the percentage change in price. Therefore, in this case the price elasticity of demand for Frappuccinos equals 20%/–50% = –0.4. Therefore, relying just on the information on the changes in the price and quantity demanded, the demand for Frappuccinos is price inelastic. As explained in Section 6.5, when demand is price inelastic, a cut in price will result in a decrease in revenue.

Step 4: Answer part c. by explaining whether other coffee houses cutting the prices of their coffees will affect your calculation from part b. of the price elasticity of demand for Frappuccinos. The calculation in part b. assumes that during the time that Starbucks cuts the price of Frappuccinos, nothing else that affects demand will have changed. We know that the coffees sold by other coffee houses are substitutes for Frappuccinos. So we would expect that if other coffeehouses cut the prices of their coffees, the demand curve for Frappuccinos will shift to the left. The 20 percent increase in the quantity of Frappuccions sold reflects the effects of both the price cut and the shift in the demand curve for Frappuccinos. Therefore our calculation of the price elasticity of demand for Frappuccinos is inaccurate. It’s likely that the price elasticity is larger (in absolute value) than the value we caculated in part b.

Step 5: Answer part d. by explaining whether the fact that some consumers are facing a “challenging economic environment” affects your answer to part b. The answer to part d. is similar to the answer to part c. If the fact that some consumers are facing a “challenging economic environment” means that these consumers are less likely to be buying coffee and other products away from home, then the demand curve for Frappuccinos will have shifted to the left during the period that Starbucks cut the price of these coffees. As a result, the value we computed for the price elasticity of demand in part b. will be inaccurate. Taken together, the factors mentioned in parts c. and d. indicate the difficulties that firms have in calculating the price elasticity of demand for their products during a time period when several factors that affect the demand for the products may be changing.

Chair Jerome Powell and other members of the Federal Open Market Committee (Photo from federalreserve.gov)

On Friday, June 28, the Bureau of Economic Analysis (BEA) released its “Personal Income and Outlays” report for April, which includes monthly data on the personal consumption expenditures (PCE) price index. Inflation as measured by annual changes in the consumer price index (CPI) receives the most attention in the media, but the Federal Reserve looks instead to inflation as measured by annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target.

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2015 with inflation measured as the change in the PCE from the same month in the previous year. Measured this way, in May PCE inflation (the blue line) was 2.6 percent in May, down slightly from PCE inflation of 2.7 percent in April. Core PCE inflation (the red line) in May was also 2.6 percent, down from 2.8 percent in April.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation sharply declined from 3.2 percent in April to -0.1 percent in in May—meaning that consumer prices actually fell during May. Core PCE inflation declined from 3.2 percent in April to 1.0 percent in May. This decline indicates that inflation by either meansure slowed substantially in May, but data for a single month should be interpreted with caution.

The following figure shows another way of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above—although note that PCE inflation is now the red line rather than the blue line), inflation as measured using only the prices of the services included in the PCE (the green line), and the trimmed mean rate of PCE inflation (the blue line). Fed Chair Jerome Powell and other members of the Federal Open Market Committee (FOMC) have said that they are concerned by the persistence of elevated rates of inflation in services. The trimmed mean measure is compiled by economists at the Federal Reserve Bank of Dallas by dropping from the PCE the goods and services that have the highest and lowest rates of inflation. It can be thought of as another way of looking at core inflation by excluding the prices of goods and services that had particularly high or particularly low rates of inflation during the month.

Inflation using the trimmed mean measure was 2.8 percent in May (calculated as a 12-month inflation rate), down only slightly from 2.9 percent in April—and still well above the Fed’s target inflation rate of 2 percent. Inflation in services remained high in May at 3.9 percent, down only slightly from 4.0 percent in April.

This month’s PCE inflation data indicate that the inflation rate is still declining towards the Fed’s target, with the low 1-month inflation rates being particularly encouraging. But the FOMC will likely need additional data before deciding to lower the committee’s target for the federal funds rate, which is currently 5.25 percent to 5.50 percent. The next meeting of the FOMC is July 30-31. What do financial markets think the FOMC will decide at that meeting?

Futures markets allow investors to buy and sell futures contracts on commodities–such as wheat and oil–and on financial assets. Investors can use futures contracts both to hedge against risk—such as a sudden increase in oil prices or in interest rates—and to speculate by, in effect, betting on whether the price of a commodity or financial asset is likely to rise or fall. (We discuss the mechanics of futures markets in Chapter 7, Section 7.3 of Money, Banking, and the Financial System.) The CME Group was formed from several futures markets, including the Chicago Mercantile Exchange, and allows investors to trade federal funds futures contracts. The data that result from trading on the CME indicate what investors in financial markets expect future values of the federal funds rate to be. The following chart from the CME’s FedWatch Tool shows the current values from trading of federal funds futures.

The probabilities in the chart reflect investors’ predictions of what the FOMC’s target for the federal funds rate will be after the committee’s July meeting. The chart indicates that investors assign a probability of only 10.3 percent to the FOMC cutting its federal funds rate target by 0.25 percentage point at that meeting and an 89.7 percent probability of the commitee leaving the target unchanged.

In contrast, the following figure shows that investors expect that the FOMC will cut its federal funds rate at the meeting scheduled for September 17-18. Investors assign a 57.9 percent probability of a 0.25 percentage point cut and a 6.2 percent probability of a 0.50 percentage point cut. The committee deciding to leave the target unchanged at 5.25 percent to 5.50 percent is assigned a probability of only 35.9 percent.

Presidents Biden and Trump during one of their 2020 debates. (Photo from the Wall Street Journal)

On the eve of first debate between President Joe Biden and former President Donald Trump, Glenn reflects on the fundamentals of sound economic policy. This essay first appeared inNational Affairs.

The advent of “Bidenomics” has resurrected decades-old debates about the merits of markets versus industrial policy. When President Joe Biden announced his eponymous strategy in June 2023, he blasted what he described as “40 years of Republican trickle-down economics” and insisted that he would seek instead to build “an economy from the middle out and the bottom up, not the top down.” He would achieve this through “targeted investments” in technologies like semiconductors, batteries, and electric cars — all of which featured heavily in initiatives like the CHIPS and Science Act and the Inflation Reduction Act. Yet despite the president’s professed support for a “middle out” economics, Bidenomics has thus far proven to be less of an intellectual framework than a set of well-intended yet ill-fated industrial-policy interventions implemented from the top down.

Some conservatives have joined Biden in embracing industrial policy. Writing recently in these pages, Republican senator Marco Rubio of Florida asserted that while it is difficult to “get industrial policy right, conservatives can and must take ownership of this space to keep the American economy strong and free.” Former president Donald Trump, for his part, staunchly advocates heavy tariffs to promote domestic manufacturing.

Conservatives who adopt their own version of protectionist tinkering with markets are missing an important opportunity. As mercantilism’s decline did for classical liberalism in the 19th century and Keynesianism’s misadventures did for neoliberalism in the 20th, Bidenomics’ failures offer an opening for the right to champion a new type of economics — one that puts opportunity for the people ahead of the economic rules of the game.

Rapid globalization and technological change have left too many Americans behind. But the answer is not for the state to invest in costly projects with dubious prospects, nor is it to adopt a strictly laissez-faire approach to the economy. By reviving classically liberal ideas about competition and opportunity in the face of change, conservatives can promote an alternative economics that retains the enormous benefits of markets and openness while putting people first.

LIBERALISM’S RISE AND FALL

Before “Bidenomics” became a popular term, national-security advisor Jake Sullivan hinted at the president’s economic priorities in an April 2023 speech at the Brookings Institution. There, he declared that a “new Washington consensus” had formed around a “modern industrial and innovation strategy,” which would correct for the excesses of the free-market orthodoxy propagated by the likes of Adam Smith, Friedrich Hayek, and Milton Friedman.

This orthodoxy, according to Sullivan, “championed tax cutting and deregulation, privatization over public action, and trade liberalization as an end in itself,” all of which eroded the nation’s industrial and social foundations. Finally, after nearly three decades of such policies, two “shocks” — the global financial crisis of 2007-2009 and the Covid-19 pandemic — ”laid bare the limits” of liberalism. The time had come, Sullivan concluded, to dispense with decades of policies touting the benefits of markets and free trade — and economists would just have to get over it.

The Biden administration’s assault on open markets and free trade is odd in some respects. Scholars at the Peterson Institute for International Economics — located just across the street from Brookings — concluded in a 2022 report that, thanks to America’s openness to globalization, trillions of dollars in economic benefits have flowed to U.S. households. Moreover, the United Nations estimates that integrating China, India, and other economies into the world trading order has brought one billion individuals out of poverty since the 1980s. The impact of technological change as a driver of growth and incomes is larger still. Juxtaposing such outcomes with the administration’s grievances calls to mind the popular outcry in Monty Python’s Life of Brian: “What have the Romans ever done for us?” Quite a lot, in fact.

Proponents of free markets have clashed with advocates of government intervention before, most notably at the dawn of classical liberalism toward the end of the 18th century and the advent of neoliberalism during the first half of the 20th. These contests were not so much battles of ideas as they were intellectual critiques of real-life policy failures.

In 1776, Adam Smith’s Inquiry into the Nature and Causes of the Wealth of Nations threw down the gauntlet. The book was radical, offering a sharp rebuke of the economic-policy order of the day. Mercantilism — or the “mercantile system,” as Smith called it — assumed that the world’s wealth is fixed, and that a state wishing to improve its relative financial strength would have to do so at the expense of others by maintaining a favorable balance of trade — typically by restricting imports while encouraging exports. Recognizing merchants’ role in generating domestic wealth, mercantilist states also developed government-controlled monopolies that they protected from domestic and foreign competition through regulations, subsidies, and even military force.

Predictably, this system enriched the merchant class. But it did so at the expense of the poor, who were subject to trade restrictions and import taxes that drove up the price of goods. It also stunted business growth, expanded the slave trade, and triggered inflation in regions with little gold and silver bullion on hand.

Smith turned the mercantilist view on its head, insisting that the real touchstone of “the wealth of a nation” was not the amount of gold and silver held in its treasury, but the value of the goods and services it produced for its citizens to consume. To maximize a nation’s wealth, he argued that the state should unleash its population’s productive capacity by liberating markets and trade. Setting markets free, he observed, would enable firms to specialize in generating the goods they produced most efficiently, and to exchange surpluses of those goods for specialized goods produced by others. This approach would spread the benefits of free trade throughout the population.

While sometimes caricatured as a full-throated endorsement of laissez-faire economics, Wealth of Nations also recognized that government played an important role in sustaining an environment that would allow free markets to flourish. This included protecting property rights, building and maintaining infrastructure, upholding law and order, promoting education, providing for national security, and ensuring competition among firms. Smith cautioned, however, that government officials should be careful not to distort markets unnecessarily through such mechanisms as taxation and overregulation, and should avoid accumulating large public debts that would drain capital from future productive activities.

Mercantilism did not suddenly fall away after Smith’s critique; it continued to dominate much of the world’s economic order for another half-century. But eventually, Smith’s arguments in favor of market liberalization carried the day. For much of the 19th and early 20th centuries, free markets and free trade facilitated unprecedented prosperity in the West.

A parallel series of events occurred during the 1930s and ’40s, when Friedrich Hayek and John Maynard Keynes famously (and nastily) debated economic theory in the pages of the Economic Journal. That contest, too, revolved around what was happening on the ground: the Great Depression and increasing government investment in industry. Keynes contended that market economies experience booms and busts based on fluctuations in aggregate demand, and that the government could mitigate the harms of recessions by stimulating that demand through increased spending. Hayek disagreed, arguing that such large-scale public spending programs as those Keynes proposed would prompt not just market inefficiency and inflation, but tyranny.

During the 1950s and ’60s, Milton Friedman took on Keynes’s theories, asserting instead that the key to stimulating and maintaining economic growth was to control the money supply. He also expanded on Hayek’s case for free markets as necessary elements of free societies: As he wrote in Capitalism and Freedom, economic freedom serves as both “a component of freedom broadly understood” and “an indispensable means toward the achievement of political freedom.”

Of course Hayek and Friedman, like Smith before them, did not immediately win the debate; Keynesianism dominated America’s economic policy for decades after the Second World War. But by the mid-1970s, rising inflation and slowed economic growth pressured policymakers to consider a different approach. Hayek and Friedman’s arguments — now often referred to collectively as “neoliberalism” — ultimately won over important political figures like Ronald Reagan and Bill Clinton in the United States and Margaret Thatcher and Tony Blair in Britain. It had a major impact on each of their economic-policy initiatives, which typically combined tax cuts and deregulation with reduced government spending and liberalized international trade.

The upshot of that liberal market order is reflected in the 2022 findings of the Peterson Institute outlined above — namely the trillions of dollars in economic benefits that have flowed to American households. In a similar vein, the institute found in a 2017 report that between 1950 and 2016, trade liberalization combined with cheaper transportation and communication owing to technological change increased per-household GDP in the United States by about $18,000. The benefits of economic liberalism have thus been and continue to be massive.

NEOLIBERAL OVERCORRECTION

For all the prosperity it brought to the world, market-induced change in an era of globalization and rapid technological advance also entailed significant costs. Leaders across the political spectrum celebrated the former but paid little attention to the latter, which hit low- and medium-skilled American workers particularly hard. As global competition intensified and technological change mounted, tens of thousands of Americans in the manufacturing industry lost their jobs. Meanwhile, state benefits programs and occupational-licensing requirements made it difficult, if not impossible, for these individuals to move in search of better opportunities.

Neoliberal economic logic asserts that maintaining the labor market’s dynamism will right the ship in response to economic change — that new jobs will be created to replace the old. While true in most respects, for individuals and communities buffeted by structural market forces beyond their control, “just let the market work” is neither an economically correct answer nor a response likely to win political favor.

Proponents of neoliberalism tend to overlook the politically salient pressures generated by the speed, irreversibility, and geographic concentration of market-induced changes. Their lack of empathy for working-class communities hollowed out by the competitive and technological disruption that took place between the 1980s and the early 2010s ceded the political lane to proponents of industrial policy, enabling Trump to ride the wave of working-class grievances to the White House in 2016.

The ensuing tariffs, along with President Biden’s protectionist activity, invited retaliation from America’s trading partners. A Federal Reserve study by economists Aaron Flaaen and Justin Pierce concluded that, contrary to protectionists’ claims, employment losses triggered by trade retaliation were significantly greater than the number of jobs garnered through protectionism. The subsidy game tells a similar story: The Inflation Reduction Act’s large incentives for domestic clean-energy projects put America’s trading partners engaged in battery and electric-vehicle manufacturing at a disadvantage, which in turn pushed greater subsidization efforts overseas and prompted political grumbling among our trading partners.

It is policy failure, not a grand new economic strategy, that the Biden and Trump administrations’ industrial policies have teed up. Market liberalism must rise once again to counter the muddled mercantilism of both. But instead of repeating the cycle of neoliberalism overcorrecting for central planning and vice versa, today’s free-market and free-trade proponents will need to update their theories to address the challenges of our contemporary economy. By recovering insights from classical liberalism while keeping people in mind, economic policymakers can once again facilitate an open economy that ensures mass opportunity and flourishing.

MUDDLED MERCANTILISM

An intellectual path forward for today’s economic liberals must begin by highlighting the practical failures of Sullivan’s “new Washington consensus.” To that end, it will be useful to revisit the lack of intellectual foundation in today’s mercantilist industrial policy.

Skepticism of industrial policy revolves around two major challenges inherent to the strategy. The first is ensuring that capital is allocated to “winners” and not “losers.” The second is protecting industrial policy from mission creep and rent seeking.

Hayek addressed the first problem in his classic 1945 article, “The Use of Knowledge in Society.” As he observed there, “the knowledge of the particular circumstances of time and place” necessary to rationally plan an economy is distributed among innumerable individuals. No single person has access to all of this localized knowledge, which is not only infinite, but also constantly in flux. Statistical aggregates cannot account for it all, either. Thus, even the most earnest and sophisticated government planners could not amass the knowledge required to allocate capital to the right firms based on ever-changing circumstances on the ground. Recent examples of the government’s misfires — from the bankruptcy of the federally subsidized solar-panel startup Solyndra to the billions in Covid-19 relief aid lost to fraud and waste — speak to the truth of Hayek’s argument.

The free market, by contrast, transmits relevant information — that “knowledge of the particular circumstances of time and place” — in real time to everyone who needs it. It does so in large part via the price system. Friedman famously illustrated this process using the humble No. 2 pencil:

Suppose that, for whatever reason, there is an increased demand for lead pencils — perhaps because a baby boom increases school enrollment. Retail stores will find that they are selling more pencils. They will order more pencils from their wholesalers. The wholesalers will order more pencils from the manufacturers. The manufacturers will order more wood, more brass, more graphite — all the varied products used to make a pencil. In order to induce their suppliers to produce more of these items, they will have to offer higher prices for them. The higher prices will induce the suppliers to increase their work force to be able to meet the higher demand. To get more workers they will have to offer higher wages or better working conditions. In this way ripples spread out over ever widening circles, transmitting the information to people all over the world that there is a greater demand for pencils — or, to be more precise, for some product they are engaged in producing, for reasons they may not and need not know.

In this way, free markets ensure that capital is allocated to the right place at the right time based on the laws of supply and demand.

The second problem that plagues industrial policy arises when policies that are nominally targeted at a single goal end up serving the interests of government actors and individual firms. This problem comes in two flavors: mission creep and rent seeking.

Mission creep is the tendency of government actors to gradually expand the goal of a given policy beyond its original scope. One illustrative example comes from the CHIPS and Science Act, a bill designed to encourage semiconductor manufacturing in the United States. The act tasked the Commerce Department with drafting the conditions that manufacturers must meet to qualify for the program’s $39 billion in subsidies. In addition to manufacturing semiconductors domestically, those rules now require subsidy recipients to offer workers affordable housing and child care, develop plans for hiring disadvantaged workers, and encourage mass-transit use among their workforces. While arguably laudable (and certainly attractive to various interest groups), these goals distract from the original purpose of the law and may even detract from it.

Rent seeking — another problem characteristic of industrial policy — is a strategy that firms employ to increase their profits without creating anything of value. They do so by attempting to influence public policy or manipulate economic conditions in their favor.

Rent seeking often arises when firms devote lobbying resources to garnering funds from new government largesse. For the CHIPS and Science Act, firms’ scramble for subsidies replaces a focus on basic research. For the Inflation Reduction Act, firms’ hiring consultants to help them gain access to agricultural-conservation spending and technical assistance replaces a focus on researching market trends.

Industrial unions — whose goals might not be consistent with market outcomes or the new industrial policy — are a second source of rent seeking. Today, both the left and right have slouched away from liberalism’s emphasis on maintaining an open and dynamic labor market, pledging instead to create and protect “good jobs” — primarily in the manufacturing sector. This new thrust is yet another example of Washington picking “winners” and “losers” among industries and firms.

Concerns about this new approach to labor policy extend well beyond neoliberal critiques of limiting labor-market dynamism. Practically speaking, who decides what a “good job” is, or that manufacturing jobs are the ones to be prized and protected? Many of today’s most desired jobs for labor-market entrants did not exist decades ago when manufacturing employment was at its peak. Why should industrial policy’s goal be to cement the past as opposed to preparing individuals and locales for the work of the future?

A PATH FORWARD

Bidenomics’ policy failures offer an opening for leaders on the right to champion a new type of liberal economics that avoids the pitfalls of both markets-only neoliberalism and industrial policy’s central planning. In doing so, they will need to keep three things in mind.

The first is obvious but bears repeating: Markets don’t always work well, and calls for intervention are not necessarily calls for industrial policy.

Critiques of neoliberalism often focus on the stark observation from Friedman’s famous 1970 New York Times piece on the purpose of the corporation, which he asserted is to maximize its profits — full stop. While the article has now generated more than five decades of criticism, Friedman’s argument is quite sensible as a starting point under the assumptions he had in mind: perfect competition in product and labor markets, and a government that does its job well — namely by providing public goods like education and defense, and correcting for externalities.

Put this way, the problem with neoliberalism is less that it is laissez-faire and more that it assumes away important questions about the state’s role in the market economy. As a prominent example, national-security concerns raise questions about the boundaries between markets and the state. Export controls and certain supply-chain restrictions can be a legitimate way to deny sensitive technologies to adversaries (principally China in the present context). But they also raise several thorny questions. For instance, which technologies should be subject to controls and restrictions? What if those technologies are also employed for non-sensitive purposes? How do we defend sensitive technologies while avoiding blatant protectionism? (The Trump administration’s invocation of “national security” in levying steel tariffs against Canada was less than convincing.) Economists should invite scientists and technology experts into these discussions rather than ceding all ground to politicians and Commerce Department officials.

A second lesson relates to competition — the linchpin of both neoliberalism and classical-liberal economics dating back to Adam Smith. Is the pursuit of competition, though a worthy goal, sufficient to ensure widespread flourishing?

Contemporary economic models assign value to economic growth, openness to globalization, and technological advance. But as noted above, with that growth, openness, and advance comes disruption, often in the form of a diminished ability to compete for new jobs and business opportunities. It’s not a stretch to argue that a classical-liberal focus on free markets should also recognize the ability to compete as an important component to advancing competition. Competition might increase the size of the economic pie, but some will have easier access to a larger slice than others. Thus, in addition to promoting competition, today’s free-market advocates need to focus on preparing individuals to reconnect to opportunity in a changing economy.

To that end, neoliberals would do well to increase public investment in education and skill training. This includes greater support for community colleges — the loci of much of the training and retraining efforts required to reconnect workers to the job market. The demand for such training is rising among young workers skeptical of the value of a four-year college degree: The Wall Street Journal recently reported that the “number of students enrolled in vocational-focused community colleges rose 16% last year to its highest level since the National Student Clearinghouse began tracking such data in 2018.” Returning to Hayek’s “Use of Knowledge” essay, these interventions are likely to be successful because they decentralize training programs, divvying them up to the educational institutions that are in the best position to prepare workers for the jobs of today and tomorrow.

A third lesson for today’s neoliberals relates to the goals of the market. Smith, the father of modern economics, was also a student of moral philosophy — a discipline studiously avoided by most contemporary economists. To win the war of policy ideas, Smith understood that the goal could not simply be for the market to function. Today, demands to “let the market work” clearly do not meet the moment.

Market and trade liberalization are not ends in themselves; they are tools for organizing and promoting economic activity. Channeling Smith’s thoughts in his other classic work emphasizing shared purpose, The Theory of Moral Sentiments, Columbia professor and Nobel laureate Edmund Phelps argued that economic policies should pursue freedom not for its own sake, but to facilitate “mass flourishing.” In this vein, markets should promote, not prevent, innovation and productivity. They should aid, not hinder, the formation of strong families, communities, and religious and civic institutions.

Just as neoliberals need to be more cognizant of the human element in economics, proponents of industrial policy need to rethink the mercantilist strand present in their proposals.

To minimize the problems endemic to industrial policy — mission creep, rent seeking, and the risk of backing the wrong firms and industries — policy architects need to be both more general and more specific in their proposed interventions. By more general, I mean they must emphasize broad mechanisms to counter market failures. In the technology industry, for instance, expanding federal funding for basic scientific research can lead to useful applications for technologies and industries without picking winners and losers. Likewise, adopting a carbon tax would provide more neutral incentives for firms to develop low-carbon fuels and technologies without the need to pick winners and spend taxpayer dollars on costly subsidies. And again, as workers’ skills are an important policy concern, increases in general public investment in education and training should be front and center in any industrial policy.

By more specific, I mean the proposed policy interventions must have more specific goals. The Trump administration’s Operation Warp Speed succeeded without picking winners or over-relying on bureaucracy largely because its goals — developing and deploying a vaccine against Covid-19 as quickly as possible — were narrowly defined. Similarly, the Apollo program — which Senator Rubio rightly pointed to as an effective example of industrial policy — succeeded in part because it focused on a single, concrete, time-bound goal: putting a man on the moon within the decade.

Targeting and customizing aid is another way of making industrial-policy goals more specific. Economist Timothy Bartik has pushed for reforms to current place-based jobs policies, which typically consist of business-related tax and cash incentives. Such incentives, he argues, should be “more geographically targeted to distressed places,” “more targeted at high-multiplier industries” like technology, more favorable to small businesses, and more “attuned to local conditions.” Different local economies have different needs, from infrastructure to land development to job training. Funding customized services and inputs is more cost effective, more directly targeted at local shortcomings, and more likely to raise employment and productivity than one-size-fits-all tax and cash incentives.

While much of this analysis has been applied to the manufacturing context, such approaches can also be applied to the services sector. Customized input support would focus on developing partnerships between businesses and local educational institutions to develop job-specific training. Public support for applied research centers could help disseminate technological and organizational improvements to firms across the country. As with the general improvements to current industrial policy outlined above, these methods harness market mechanisms while recognizing and responding to underlying market failures.

A RIGHT TO OPPORTUNITY

The neoliberal notion that markets should focus on allocation and growth alone cannot be an endpoint; updating classical-liberal ideas with a deliberate focus on adaptation and the ability to compete is the place to start. Recognizing a right to opportunity in addition to property rights could provide a liberal counterweight to the temptation to reach for industrial policy to help distressed communities.

This right to opportunity — for today and tomorrow — should lead a conservative pushback to Bidenomics. Voters might not have much of a choice between Biden and Trump’s economic populism in the election this fall, but economists and policymakers can begin to advance a new market economics that leaves no Americans behind in the hope that future administrations will take notice.

The monthly “Employment Situation” report from the Bureau of Labor Statistics (BLS) is closely watched by economists, investment analysts, and Federal Reserve policymakers. Many economists believe that the payroll employment data from the report is the best single indicator of the current state of the economy.

Most economists, inside and outside of the government, accept the dates determined by the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER) for when a recession begins and ends. Although that committee takes into account a variety of macroeconomic data series, the peak of a business cycle as determined by the committee almost always corresponds to the peak in payroll employment and the trough of a business cycle almost always corresponds to the trough in payroll employment.

One drawback to relying too heavily on payroll employment data in gauging the state of the economy is that the data are subject to—sometimes substantial—revisions. As the BLS explains: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.” The revisions can be particularly large at the beginning of a recession.

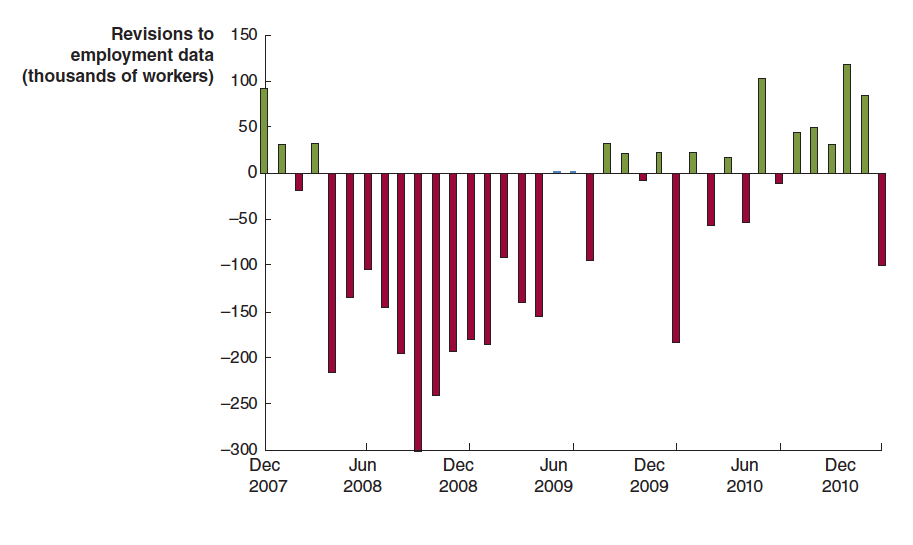

For example, the following figure shows revisions the BLS made to its initial estimates of the change in payroll employment during the months around the 2007–2009 recession. The green bars show months for which the BLS revised its preliminary estimates to show that fewer jobs were lost (or that more jobs were created), and the red bars show months for which the BLS revised its preliminary estimates to show that more jobs were lost (or that fewer jobs were created).

For example, the BLS initially reported that employment declined by 159,000 jobs during September 2008. In fact, after additional data became available, the BLS revised its estimate to show that employment had declined by 460,000 jobs during the month—a difference of 300,000 more jobs lost. As the recession deepened between April 2008 and April 2009, the BLS’s initial reports underestimated the number of jobs lost by 2.3 million. In other words, the recession of 2007–2009 turned out to be much more severe than economists and policymakers realized at the time.

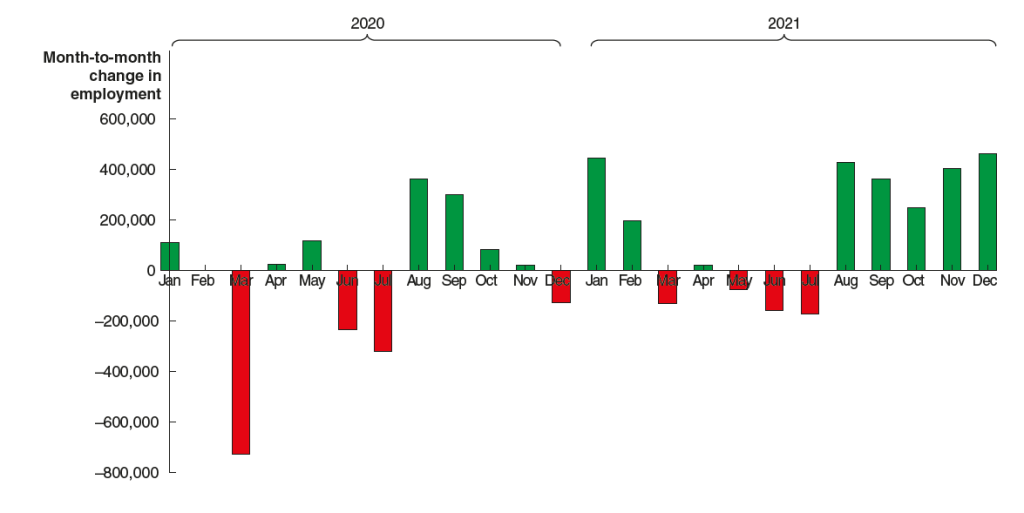

The BLS also made substantial revisions to its initial estimates of payroll employment for 2020 and 2021 during the Covid pandemic, as the following figure shows. (Note that this figure appears in our new 9th edition of Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1 and Essentials of Economics, Chapter 13, Section 13.1).)

The BLS initially estimated that employment in March 2020 declined by about 700,000. After gathering more data, the BLS revised its estimate to indicate that employment declined by twice as much. Similarly, the BLS’s initial estimates substantially understated the actual growth in employment from August to December 2021. After gathering more data, the BLS revised its estimate to indicate that nearly 2 million more jobs had been created during those months than it had originally estimated.

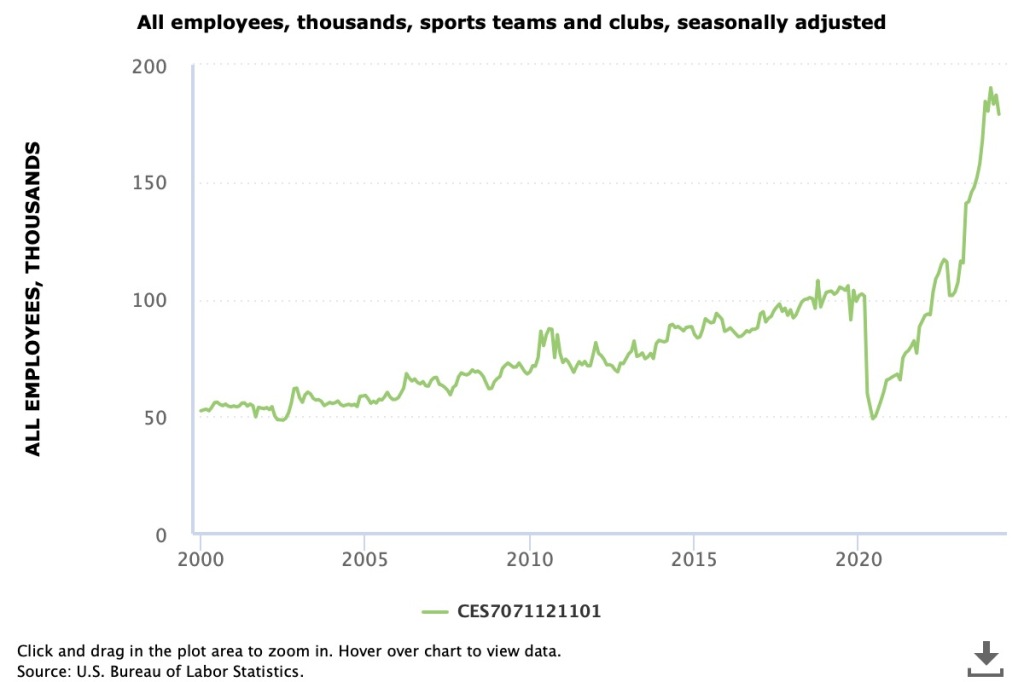

Just as the initial estimates for total payroll employment are often revised by sutbstantial amounts up or down, the same is true of the initial estimates of payroll employment in individual industries. Because the number of establishments surveyed in any particular industry can be small, the initial estimates can be highly inaccurate. For instance, Justin Fox, a columnist for bloomberg.com recently noted what appears to be a surge in employment in the “sports teams and clubs” industry. As the following figure shows, employment in this industry seems to have increased by an improbably large 75 percent. Was there a sudden increase in the United States in the number of new sports teams? Certainly not over just a few months. It’s more likely that most of the increase in employment in this industry will disappear when the initial employment estimates are revised.

One source of data for the BLS revisions to the monthly payroll employment data is the BLS’s “Quarterly Census of Employment and Wages.” The QCEW is based on the reports required of all firms that participate in the state and federal unemployment insurance program. The BLS estimates that 95 percent of all jobs in the United States are included in the QCEW data. As a result, the QCEW surveys about 11.9 million establishments as opposed to the 666,000 establishments included in the establishment survey.

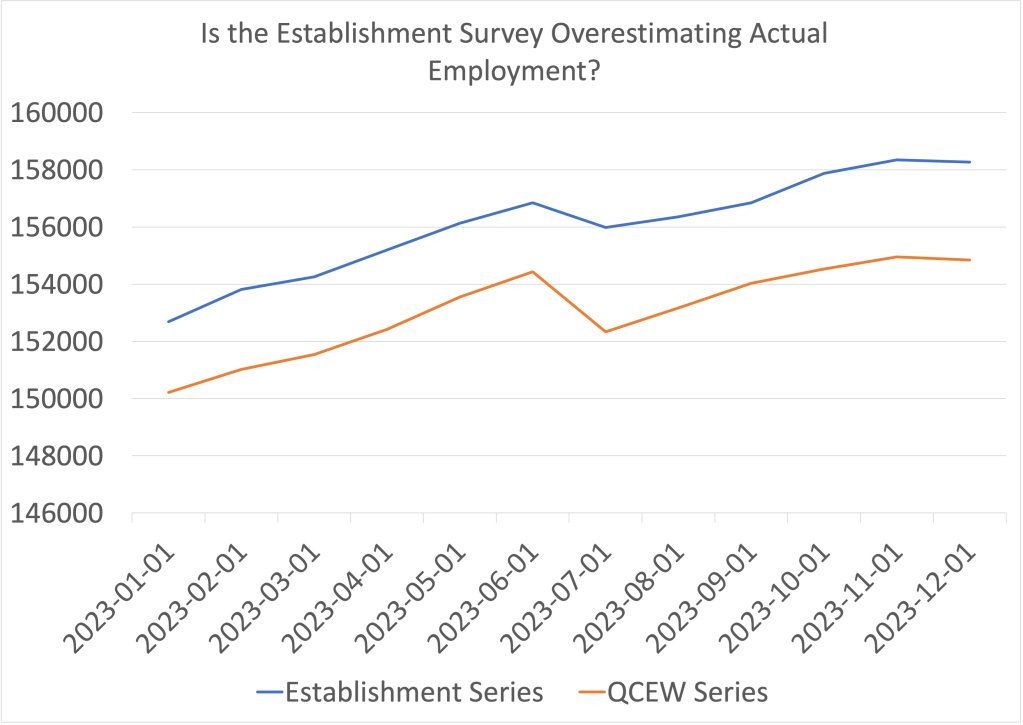

The BLS uses the QCEW to benchmark the payroll employment data, which reconciles the two series. The BLS makes the revisions with a lag. For instance, the payroll employment data for 2023 won’t be revised using the QCEW data until August 2024. Looking at the 2023 employment data from the two series shows a large discrepancy, as seen in the following figure.

The blue line shows the employment data from the establishment survey and the orange line shows the data from the QCEW survey. (Both series are of nonseasonally adjusted data.) The values on the vertical axis are thousands of workers. In December 2023, the establishment survey indicated that a total of 158,347,000 people were employed in the nonfarm sector in the United States. The QCEW series shows a total of 154,956,133 people were employed in the nonfarm sector—about 3.4 million fewer.

How can we interpret the discrepancy between the employment totals from the two series? The most straightforward interpretation is that the QCEW data, which uses a larger sample, is more accurate and payroll employment has been significantly overstating the level of employment in the U.S. economy. In other words, the labor market was weaker in 2023 than it seemed, which may help to explain why inflation slowed as much as it did, particularly in the second half of the year.

However, this interpretation is not clear cut because the QCEW data are also subject to revision. As Ernie Tedeschi, director of economics at the Budget Lab at Yale and former chief economist for the Council of Economic Advisers, has pointed out, the QCEW data are typically revised upwards, which would close some of the gap between the two series. So, although it seems likely that the closely watched payroll employment data have overstated the strength of the labor market, we won’t get a clearer indication of how large the overstatement is until August when the BLS will use the QCEW data to benchmark the payroll employment data.

Image of “a woman shopping in a grocery store” generated by ChatGTP 4o.

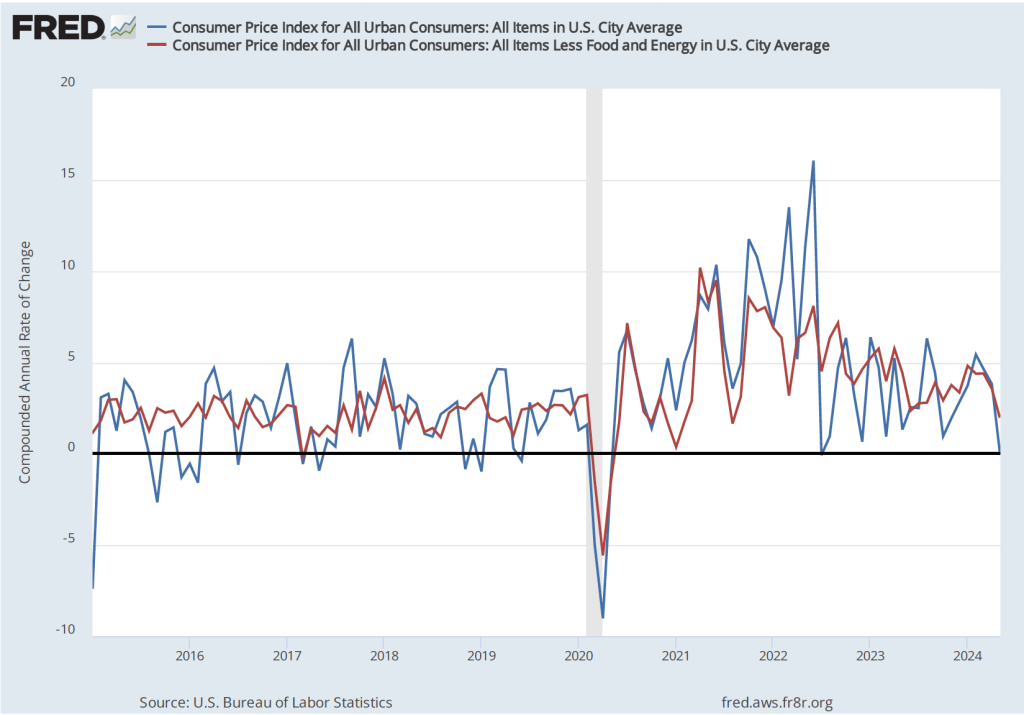

Today (June 12) we had the unusual coincidence of the Bureau of Labor Statistics (BLS) releasing its monthly report on the consumer price index (CPI) on the same day that the Federal Open Market Committee (FOMC) concluded a meeting. The CPI report showed that the inflation rate had slowed more than expected. As the following figure shows, the inflation rate for May measured by the percentage change in the CPI from the same month in the previous month—headline inflation (the blue line)—was 3.3 percent—slightly below the 3.4 percent rate that economists surveyed by the Wall Street Journal had expected, and slightly lower than the 3.4 percent rate in April. Core inflation (the red line(—which excludes the prices of food and energy—was 3.4 percent in May, down from 3.6 percent in April and slightly lower than the 3.5 percent rate that economists had been expecting.

As the following figure shows, if we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—the declines in the inflation rate are much larger. Headline inflation (the blue line) declined from 3.8 percent in April to 0.1 percent in May. Core inflation (the red line) declined from 3.6 percent in April to 2.0 percent in May. Overall, we can say that inflation has cooled in May and if inflation were to continue at the 1-month rate, the Fed will have succeeded in bringing the U.S. economy in for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession.

But two important notes of caution:

1. It’s hazardous to rely to heavily on data from a single month. Over the past year, the BLS has reported monthly inflation rates that were higher than economists expected and rates that was lower than economists expected. The current low inflation rate would have to persist over at least a few more months before we can safely conclude that the Fed has achieved a safe landing.

2. As we discuss in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5), the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target. So, today’s encouraging CPI data would have to carry over to the PCE data that the Bureau of Economic Analysis (BEA) will release on January 28 before we can conclude that inflation as the Fed tracks it did in fact slow significantly in April.

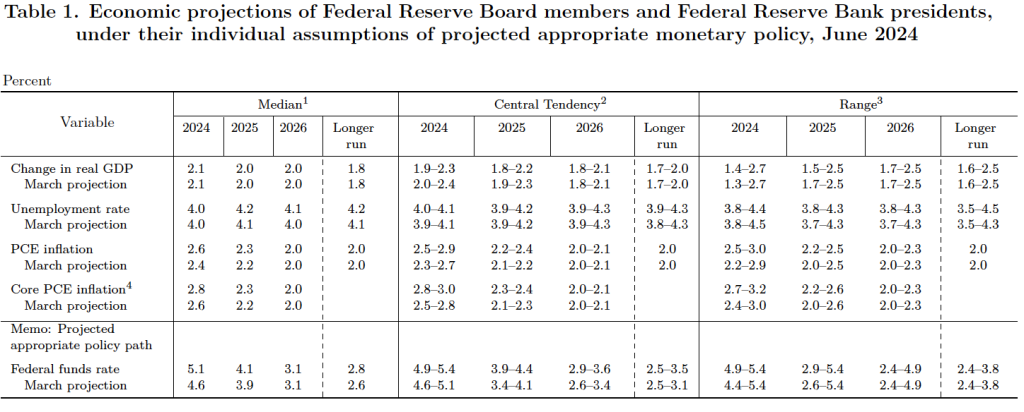

The BLS released the CPI report at 8:30 am eastern time. The FOMC began its meeting later in the day and so committee members were able to include in their deliberations today’s CPI data along with other previously available information on the state of the economy. At the close of the meeting, , the FOMC released a statement in which it stated, as expected, that it would leave its target range for the federal funds rate unchanged at 5.25 percent to 5.50 percent. After the meeting, the committee also released—as it typically does at its March, June, September, and December meetings—a “Summary of Economic Projections” (SEP), which presents median values of the committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

The table shows that compared with their projections in March—the last time the FOMC published the SEP—committee members were expecting higher headline and core PCE inflation and a higher federal funds rate at the end of this year. In the long run, committee members were expecting a somewhat highr unemployment rate and somewhat higher federal funds rate than they had expected in March.

Note, as we discuss in Macreconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Section 24.4 and Essentials of Economics, Chapter 16, Section 16.4), there are twelve voting members of the FOMC: the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and presidents of four of the other 11 Federal Reserve Banks, who serve one-year rotating terms. In 2024, the presidents of the Richmond, Atlanta, San Francisco, and Cleveland Feds are voting members. The other Federal Reserve Bank presidents serve as non-voting members, who participate in committee discussions and whose economic projections are included in the SEP.

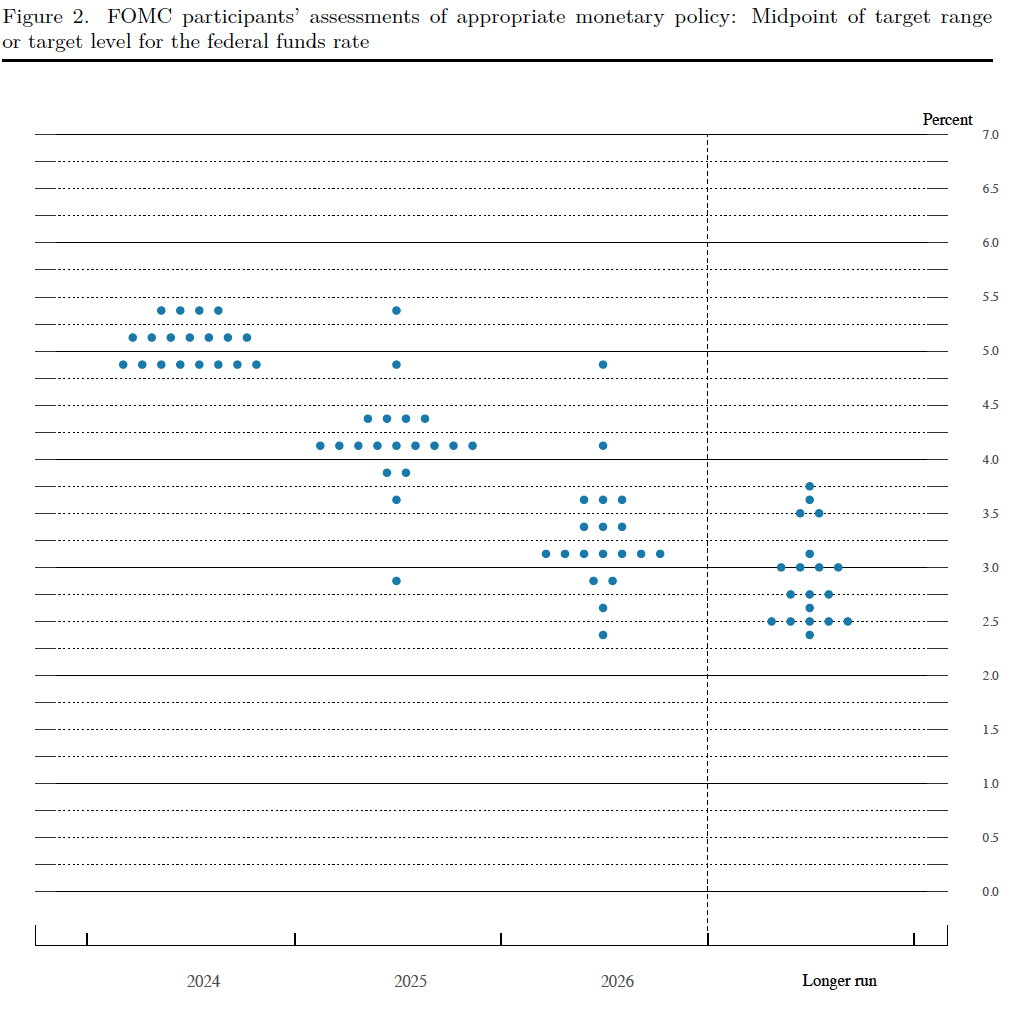

Prior to the meeting there was much discussion in the business press and among investment analysts about the dot plot, shown below. Each dot in the plot represents the projection of an individual committee member. (The committee doesn’t disclose which member is associated with which dot.) Note that there are 19 dots, representing the 7 members of the Fed’s Board of Governors and all 12 presidents of the Fed’s district banks.

The plots on the far left of the figure represent the projections of each of the 19 members of the value of the federal funds rate at the end of 2024. Four members expect that the target for the federal funds rate will be unchanged at the end of the year. Seven members expect that the committee will cut the target range once, by 0.25 percentage point, by the end of the year. And eight members expect that the cut target range twice, by a total of 0.50 percent point, by the end of the year. Members of the business media and financial analysts were expecting tht the dot plot would project either one or two target rate cuts by the end of the year. The committee was closely divided among those two projections, with the median projection being for a single rate cut.

In its statement following the meeting, the committee noted that:

“In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‐backed securities. The Committee is strongly committed to returning inflation to its 2 percent objective.”

In his press conference after the meeting, Fed Chair Jerome Powell noted that the morning’s CPI report was a “Better inflation report than nearly anyone expected.” But, Powell also noted that: “You don’t want to be motivated any one data point.” Reinforcing the view quoted above in the committee’s statement, Powell emphasized that before cutting the target for the federal funds rate, the committee would need “Greater confidence that inflation is moving back to 2% on a sustainable basis.”

In summary, today’s CPI report was an indication that the Fed is on track to bring about a soft landing, but the FOMC will be closely analyzing macroeconomic data over at least the next few months before it is willing to cut its target for the federal funds rate.

Image of “people working in a store” generated by ChatGTP 4o.

This morning (June 7), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report for May. Recent government releases of macroeconomic data have indicated that the expansion of the U.S. economy is slowing. For instance, as we noted in this recent post on the JOLTS report, the labor market seems to be normalizing. Real personal consumption expenditures declined from March to April. The Federal Reserve Bank of New York’s Nowcast of real GDP growth during the current quarter declined from 2.74 percent at the end of April to 1.76 percent at the end of May. That decline reflects some weakness in the data series the economists at the New York Fed use to forecast current real GDP growth

In that context, today’s jobs report was, on balance, surprisingly strong. The report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and policymakers at the Federal Reserve believe that employment data from the establishment survey provides a more accurate indicator of the state of the labor market than do either the employment data or the unemployment data from the household survey. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

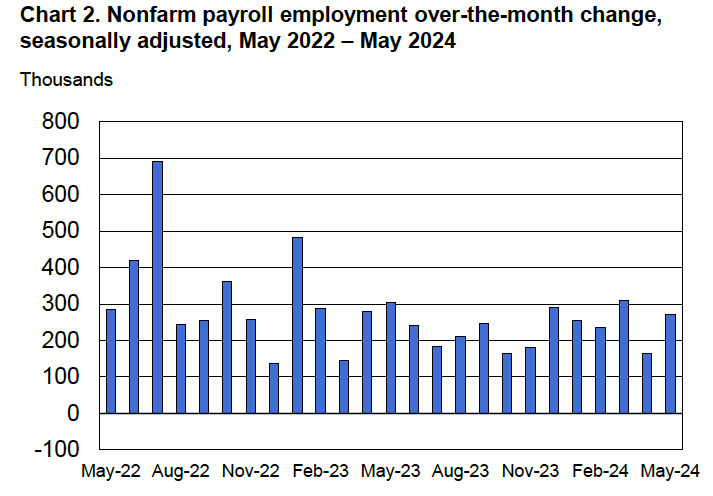

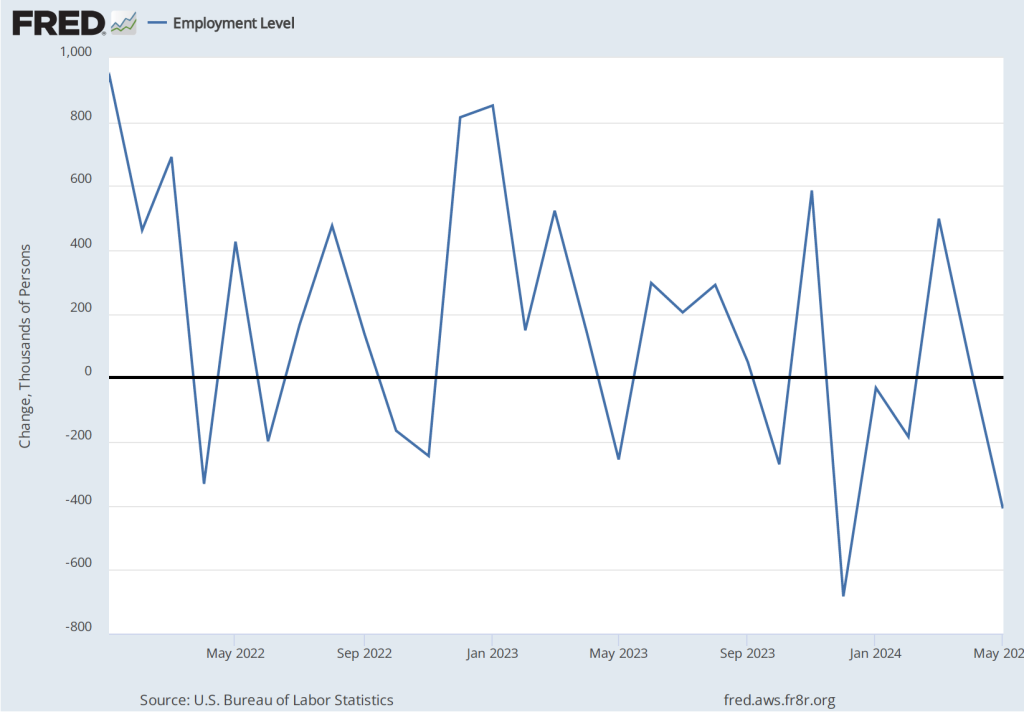

According to the establishment survey, there was a net increase of 272,000 jobs during May. This increase was well below the increase of 190,000 that economists had forecast in a survey by the Wall Street Journal and well above the net increase of 165,000 during April. (Bloomberg’s survey of economists yielded a similar forecast of an increase of 180,000.) The increase was also higher than the 232,000 average monthly increase during the past year. The following figure, taken from the BLS report, shows the monthly net changes in employment for each month during the past two years.

The surprising strength in employment growth in establishment survey was not echoed in the household survey, which reported a net decrease of 408,000 jobs. As the following figure shows, the net change in jobs from the household survey moves much more erratically than does the net change in jobs in the establishment survey, and—as noted earlier—the two surveys are of somewhat different groups. Still, the discrepancy between the two survey was notable.

The unemployment rate, which is also reported in the household survey, ticked up slightly from 3.9 percent to 4.0 percent. This is the first time that the unemployment has reached 4.0 percent since January 2022.

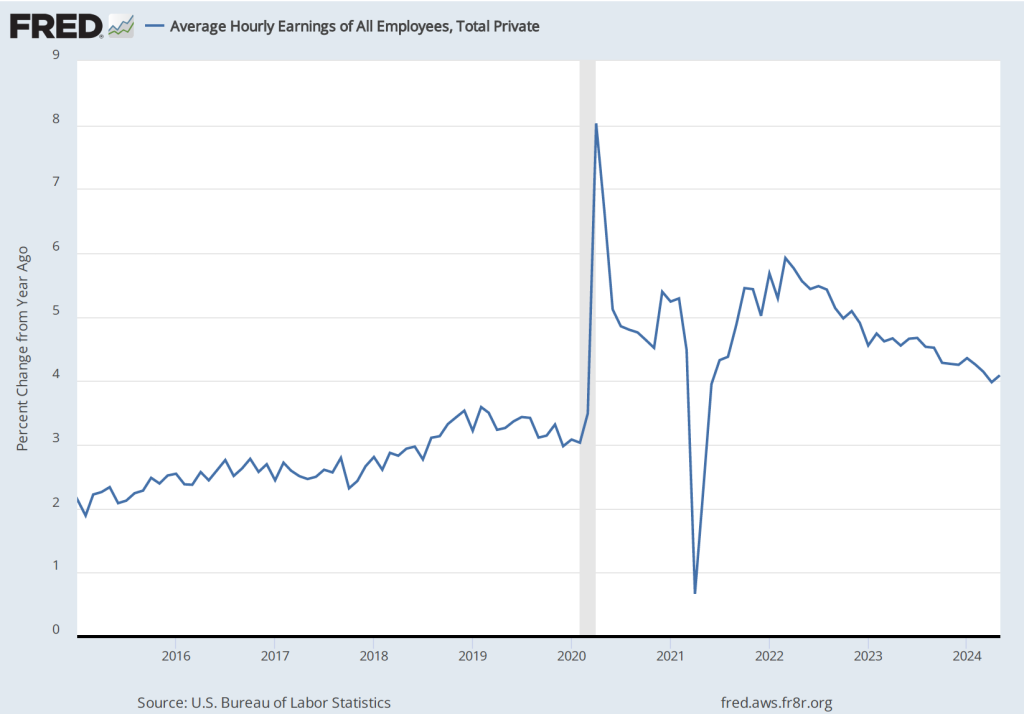

The establishment survey also includes data on average hourly earnings (AHE). As we note in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage that it is available monthly, whereas the ECI is only available quarterly. The following figure show the percentage change in the AHE from the same month in the previous year. The 4.1 percent increase in May was a slight increase from the 4.0 percent increase in April. The increase in the rate of wage inflation is in contrast with the decline in employment and increase in the unemployment rate in the same report.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. The 1-month rate of wage inflation of 4.9 percent in May is a sharp increase from the 2.8 percent rate in April, although it’s unclear whether the increase represents a significant acceleration in wage inflation or is just reflecting the greater volatility in wage inflation when calculated this way.

To answer the question posed in the title to this post, the latest jobs report is a mixed bag that doesn’t send a clear message as to the state of the economy. The strong increase in employment and the increase in the rate of wage growth indicate that economy may not be slowing sufficiently to result in inflation declining to the Federal Reserve’s 2 percent annual target. On the other hand, the decline in employment as measured in the household survey and the tick up in the unemployment rate, along with the data in the recent JOLTS report, indicate that the labor market may be returning to more normal conditions.

It seems unlikely that this jobs report will have much effect on the thinking of the Fed’s policy-making Federal Open Market Committee (FOMC), which has its next meeting next week on June 11-12.

Image of “a small business with a help wanted sign in the window” generated by ChatGTP 4o.

This morning (June 4), the Bureau of Labor Statistics (BLS) released its “Job Openings and Labor Turnover” (JOLTS) report for April 2024. The report proivided more data indicating that the U.S. labor market is continuing its return to pre-pandemic conditions. The following figure shows that, at 4.8 percent, the rate of job openings has continued its slow decline from the rate of 7.4 percent in March 2022. The rate in April was the same as the rate in January 2019, although it was till above the rates during most of 2019 and early 2020, as well as the rates during most of the period following the Great Recession of 2007–2009.

The BLS defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. The rate of job openings is the number of job openings divided by the number of job openings plus the number of employed workers, multiplied by 100.

In the following figure, we compare the total number of job openings to the total number of people unemployed. The figure shows a slow decline from a peak of more than 2 job openings per unemployed person in the spring of 2022 to 1.2 job openings per employed person in April 2024—about the same as in 2019 and early 2020, before the pandemic. Note that the number is still above 1.0, indicating that the demand for labor is still high, although no higher than during the strong labor market of 2019.

The rate at which workers are willing to quit their jobs is an indication of how they perceive the ease of finding a new job. As the following figure shows, the quit rate declined slowly from a peak of 3 percent in late 2021 and early 2022 to 2.2 percent in November 2023, where it has remained through April of 2024. That rate is slightly below the rate during 2019 and early 2020. By this measure, workers perceptions of the state of the labor market seem largely unchanged in recent months.

The JOLTS data indicate that the labor market is about as strong as it was in the months priod to the start of the pandemic, but it’s not as historically tight as it was through most of 2022 and 2023.

On Friday morning, the BLS will release its “Employment Situation” report for May, which will provide additional data on the state of the labor market. (Note that the data in the JOLTS report lag the data in the “Employment Situation” report by one month.)

Image of “someone in Zimbabwe holding the new ZiG currency” generated by ChatGPT 4o.

The classical gold standard lasted from 1880 until the outbreak of World War I in 1914 disrupted the global financial system. Under the gold standard, countries stood ready to redeem their paper currencies in gold and many business contracts contained “gold clauses” that allowed the receiver of funds to insist on being paid in gold. The countries shaded in yellow in the following figure were on the gold standard at the beginning of 1914.

After World War I, the United States remained on the gold standard but the very high inflation rates during and immediately after the war made it difficult for most European countries to resume redeeming their domestic currencies in gold. The United Kingdom didn’t return to the gold standard until 1925—seven years after the end of the war—at which time several other countries participated with the United Kingdom and the United States in what was called the gold exchange standard. In this system, countries fixed their exchange rates against the U.S. dollar and the British pound and held their international reserves in either pounds or dollars. By fixing the value of their currencies against the dollar and the pound—which were both convertible into gold—the currencies effectively fixed the value of their currencies against gold. The gold exhange standard ended in 1931 when, as the result of financial problems caused by the Great Depression, the United Kingdom stopped the convertibility of pounds into gold. The United States stopped the convertiblity of dollars into gold in 1933. (We discuss the gold standard in the online appendix to Macroeconomics, Chapter 18 and Economics, Chapter 28, and in Money, Banking, and the Financial System, Chapter 16, Section 16.4).

In 1944, near the end of World War II, several countries meeting at Bretton Woods New Hampshire agreed to fix the exchange rates between their currencies. Under the Bretton Woods system, the United States agreed to convert U.S. dollars into gold at a price of $35 per ounce—but only in dealing with foreign central banks. U.S. citizens continued to be prohibited from redeeming dollars for gold. The central banks of all other members of the system pledged to buy and sell their currencies at fixed rates against the dollar but not to exchange their currencies for gold either domestically or internationally. As can be seen, the Bretton Woods system was not actually a gold standard because no members of the system allowed their currencies to be freely convertible into gold. The difficulty of keeping exchange rates fixed over long periods led to the collapse of the Bretton Woods system in 1971. (We discuss the Bretton Woods system in the places referenced at the end of the last paragraph.)

Although over the decades there have been various proposals to return to the gold standard, it seems unlikely that the United States or other high-income countries will ever do so. Current day advocates of returning to the gold standard often mention the check the gold standard can place on inflation because the size of a country’s money supply is limited by the country’s gold reserves. In the United States and most other high-income countries the central bank attempts to regulate the inflation rate by controlling short-term interest rates. In lower-income countries, central banks are often not able to act independently of the government. That has been the situation in the African country of Zimbabwe, which has frequently experienced hyperinflation—that is, rates of inflation exceeding 50 percent per month. The inflation rate in 2008 reached a staggering 15 billion percent. As a result, most people in Zimbabwe lost faith in Zimbabwean currency and instead used U.S. dollars for most buying and selling.

That most of the currency in circulation in Zimbabwe is U.S. dollars causes two problems: 1) The supply of available U.S. dollars is limited—so much so that some businesses carefully wash dollars to try to prolong their usability; and 2) few U.S. coins are available, making it difficult for businesses to make change for purchases that aren’t priced in even dollar amounts. Some businesses give customers change in the form of candy or other small food items. The government has made several attempts to resume printing Zimbawean dollars but has had trouble getting consumers and businesses to accept them.

In late April, the Zimbabwean tried a different approach, introducing a new currency, the ZiG, which is short for Zimbabwe Gold. The new paper currency is “backed” by the government’s gold supply, which has a value of about $185 million U.S. dollars. We put the word “backed” in quotation marks because the government isn’t backing the ZiG in the way that governments backed their currency during the period of the classical gold standard. Under the gold standard, paper currency was freely convertible into gold, so anyone wishing to exchange currency for gold was able to do so. The ZiG isn’t convertible into gold. The government is backing the currency with gold only in the sense that it pledges not to issue more currency than it has gold. In other words, the government is essentially promising to put a limit on the total value of the ZiG currency it will issue. Zimbabwean governments have made similar promises in the past that they have ended up breaking.

In its first weeks, the ZiG was having trouble finding acceptance among consumers and businesses, despite efforts by the government to require most businesses to accept it. An article in the Financial Times quoted the owner of a grocery store in the capital of Harare as stating that he won’t accept the ZiG because “My business is alive because I stick to the US dollar.” Similarly, the web site of the BBC quoted the owner of a market stall as saying that “Everything, absolutely everything, is still in US dollars.”

As we discuss in Macroeconomics, Chapter 24, the key to the acceptance of any paper currency is that households and firms have confidence that if they accept the paper currency in exchange for goods and services, the currency will not lose much value during the time they hold it. Without this confidence, currency can’t fulfill the key function of serving as a medium of exchange. In Zimbabwe, as a post on the web site of the World Economic Forum puts it: “It remains to be seen whether the new ZiG can gain the confidence of the public and become a stable local currency, which would allow officials to regain control over monetary policy.”

Supports: Macroeconomics, Chapter 15,Economics, Chapter 25, Essentials of Economics, Chapter 17, and Money, Banking, and the Financial System, Chapter 15.

Image generated by ChatGTP-4o.

In a book review in the Wall Street Journal, the financial writer James Grant referred to “the Federal Reserve’s goal to cheapen the dollar by 2% a year.”

Briefly explain what “cheapen the dollar” means.

Briefly explain what Grant means by writing that the Fed has a “goal to cheapen the dollar by 2% a year.”

Do you agree with Grant that the Fed has this goal? Briefly explain.

Solving the Problem Step 1: Review the chapter material. This problem is about the economic effects of the Federal Reserve’s policy goal of a 2 percent annual inflation rate, so you may want to review Chapter 15, Section 15.5, “A Closer Look at the Fed’s Setting Monetary Policy Targets.”

Step 2: Answer part a. by explaining what “cheapen the dollar” means. Judging from the context, “cheapen the dollar” means to reduce the purchasing power of a dollar. Whenever inflation occurs, the amount of goods and services a dollar can purchase declines. If the inflation rate in a year is 10 percent, than at the end of the year $1,000 can buy 10 percent fewer goods and services than it could at the beginning of the year.

Step 3: Answer part b. by expalining what Grant means by the Fed having a goal of cheapening the dollar by 2 percent a year. Congress has given a dual mandate of high employment and price stability. Since 2012, the Fed has interpreted a 2 percent annual inflation rate as meeting its mandate for price stability. So, Grant means that the Fed’s 2 percent annual inflation goal in effect is also a goal to cheapen—or reduce the purchasing power of the dollar—by 2 percent a year.

Step 4: Answer part c. by explaining whether you agree with Grant that the Fed has a goal of cheapening the dollar by 2 percent a year. As explained in the answer to part b., there is a sense in which Grant is correct; the Fed’s goal of a 2 percent inflation rate is a goal of allowing the purchasing power of the dollar to decline by 2 percent a year. One complication, however, is that most economists believe that changes in price indexes such as the consumer price index (CPI) and the personal consumption expenditures (PCE) price index overstate the actual amount of inflation occurring in the economy. As we discuss in Macroeconomics, Chapter 9, Section 9.4 (Economics, Chapter 19, Section 19.4, and Essentials of Economics, Chapter 13, Section 13.4), there are several biases that cause price indexes to overstate the true inflation rate; the most important of the biases is the failure of price indexes to take fully into account improvements over time in the quality of many goods and services. If increases in price indexes are overstating the inflation rate by one percentage point, then the Fed’s goal of a 2 percent inflation rate results in the dollar losing 1 percent—rather than 2 percent—of its purchasing power over time, corrected for changes in quality.