Novo Nordisk production facility in Denmark (Photo from Bloomberg News via the Wall Street Journal.)

Like most other small European countries, imports and exports are more important in the Danish economy than in the U.S. economy. In 2022, imports were 59 percent of Danish GDP and exports were 70 percent. In contrast, in 2022 imports were only 16 percent of U.S. GDP and exports were only 12 percent.

The Danish company Novo Nordisk makes the weight-loss prescription injections Ozempic and Wegovy. Because these and related pharmaceuticals are the first to result in significant weight loss among patients, demand for them has been very strong. (Note that some researchers believe that is not yet clear whether long-term use of these drugs might have side effects.) Demand has been so strong that Novo Nordisk’s market cap—the total value of its outstanding shares of stock—is now larger than Denmark’s GDP. According to the Wall Street Journal, Novo Nordisk now has the second largest market cap in Europe, behind only luxury good manufacturer LVMH Moët Hennessy Louis Vuitton

Most of Novo Nordisk’s customers are outside of Denmark, so to buy Ozempic or Wegovy, these customers much exchange their domestic currency—for example, euros, U.S. dollars, pounds, or yen—for Danish kroner. This increase in demand, increases the value of kroner relative to dollars, euros, and other currencies. (We discuss the effects of changes in demand and supply of a currency relative other currencies in Macroeconomics, Chapter 18, Section 18.2, Economics, Chapter 28, Section 28.2, and Essentials of Economics, Chapter 19, Section 19.6.)

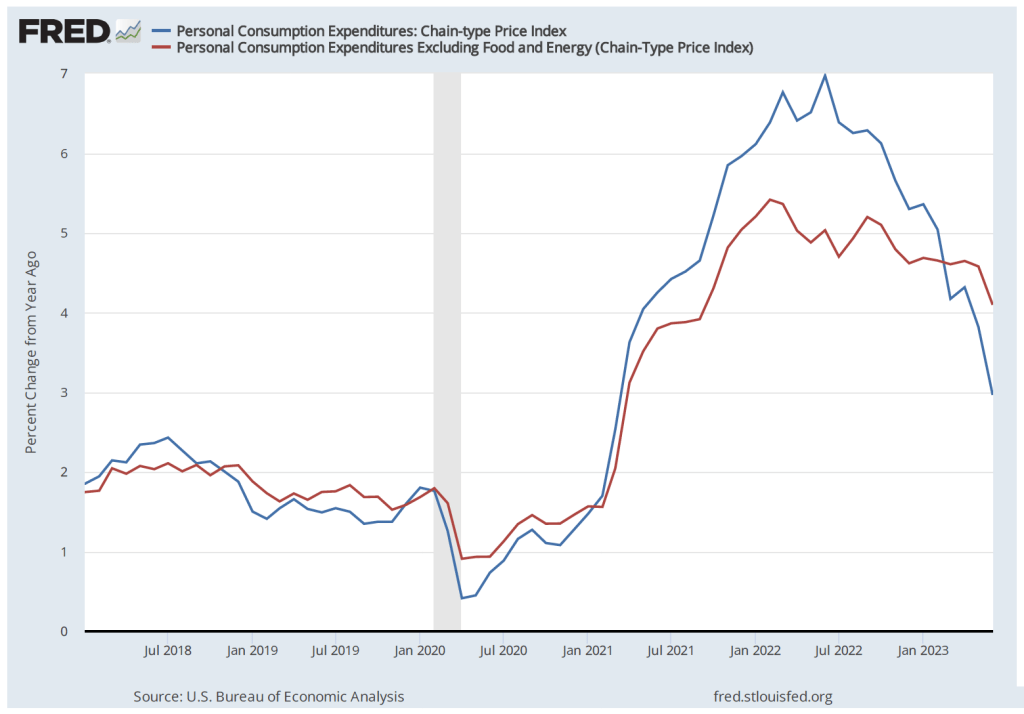

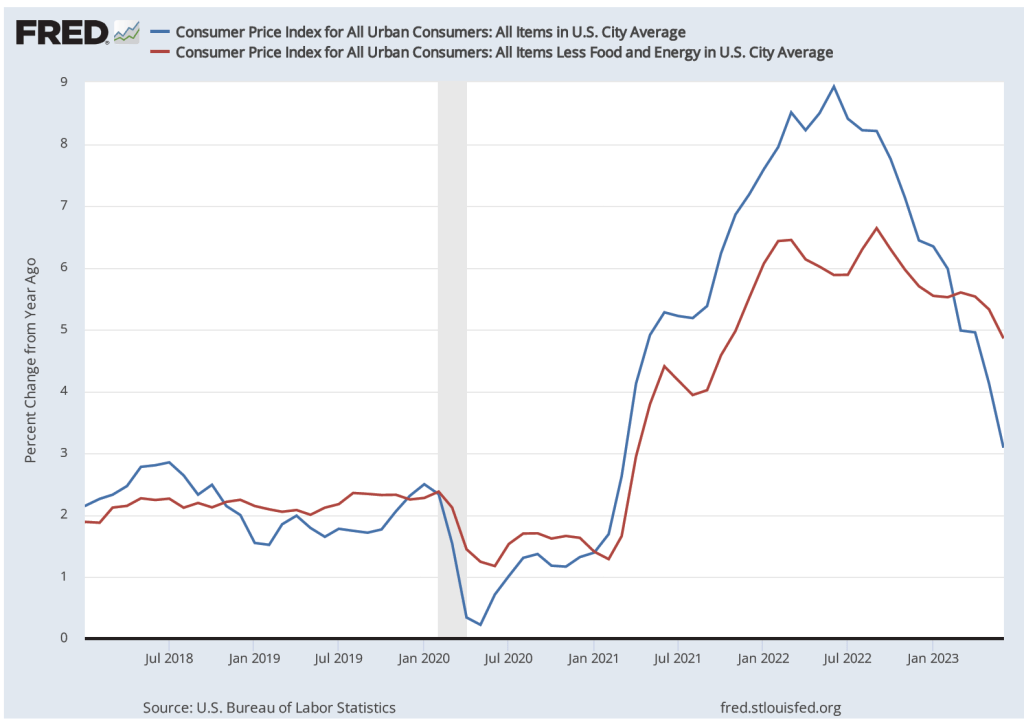

Denmark has been a member of the European Union (EU), since the EU’s formation in 1991. But it is one of two EU countries (Sweden is the other) that has retained its own currency rather than using the euro. Because most of Denmark’s trade has traditionally been with other countries in the EU, the Danmarks Nationalbank, Denmark’s central bank, has pegged the value of the krone to the euro. Pegging makes it easier for Danish firms to plan because they know the prices their goods and services will sell for in eurozone countries. In addition, Danish firms that borrow in euros know how much in interest they will be paying in kroner. Finally, if the krone rises in value against other currencies, prices of imported goods and services will increase, raising the Danish inflation rate. (We discuss currency pegs in Macroeconomics, Chapter 18, Section 18.3, and Economics, Chapter 28, Section 28.3.) Inflation is a significant concern in Denmark because, as the following figure shows, the inflation rate reached 10.1 percent in October 2022. Although by July 2023, the inflation rate had decline to 3.1 percent, that rate was still above the Nationalbank’s inflation target of 2 percent.

Source: Statistics Denmark, dst.dk.

To keep the the krone pegged against the euro, the Nationalbank has to reduce the demand for the krone. The key tool that a central bank has to reduce demand for its country’s currency is interest rates. If the Nationalbank keeps interest rates in Denmark below interest rates in eurozone countries, investors will demand fewer kroner in exchange for euros. Accordingly, the Nationalbank as kept its key monetary policy rate below the corresponding rate set by the European Central Bank. In August the ECB’s policy rate was 3.75 percent, whereas the Nationalbank’s corresponding policy rate was 3.35 percent.

It’s unusual even for a small country that its central bank has to take steps to respond to a surge in demand for a single product. But that was the situation of the Danish central bank in 2023.

Sources: Joseph Walker, Dominic Chopping, and Sune Engel Rasmussen Wall Street Journal, August 17, 2023; Matthew Fox, “America’s Favorite Weight Loss Drugs Are Impacting Denmark’s Currency and Interest Rates,” finance.yahoo.com, August 18, 2023; Christian Weinberg, “Novo’s Value Surpasses Denmark GDP After Obesity Drug Boost,” bloomberg.com, August 9, 2023; Tom Fairless, “European Central Bank Raises Rates, Says Pausing Is an Option” Wall Street Journal, July 27, 2023; and “Official Interest Rates,” nationalbanken.dk.