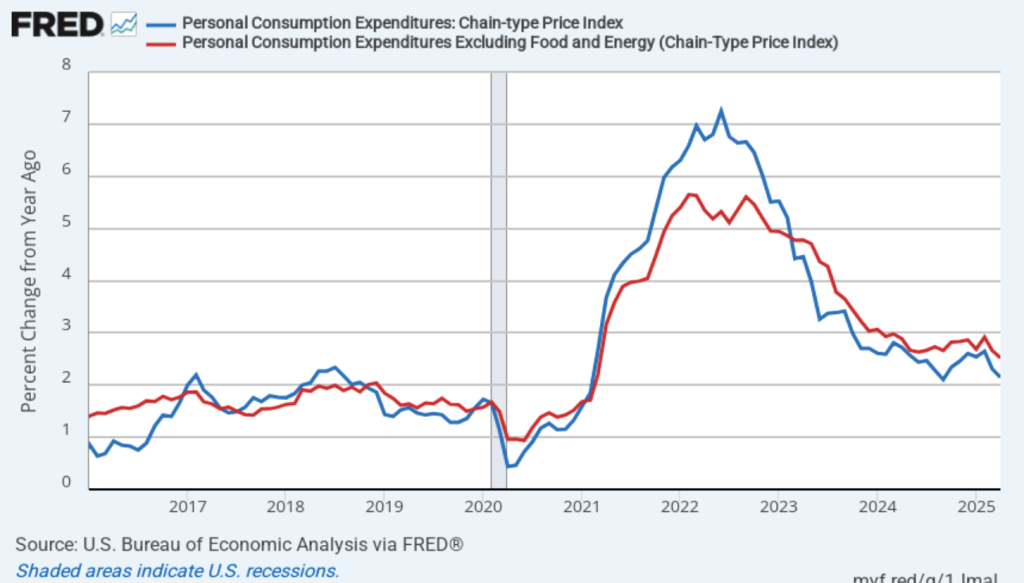

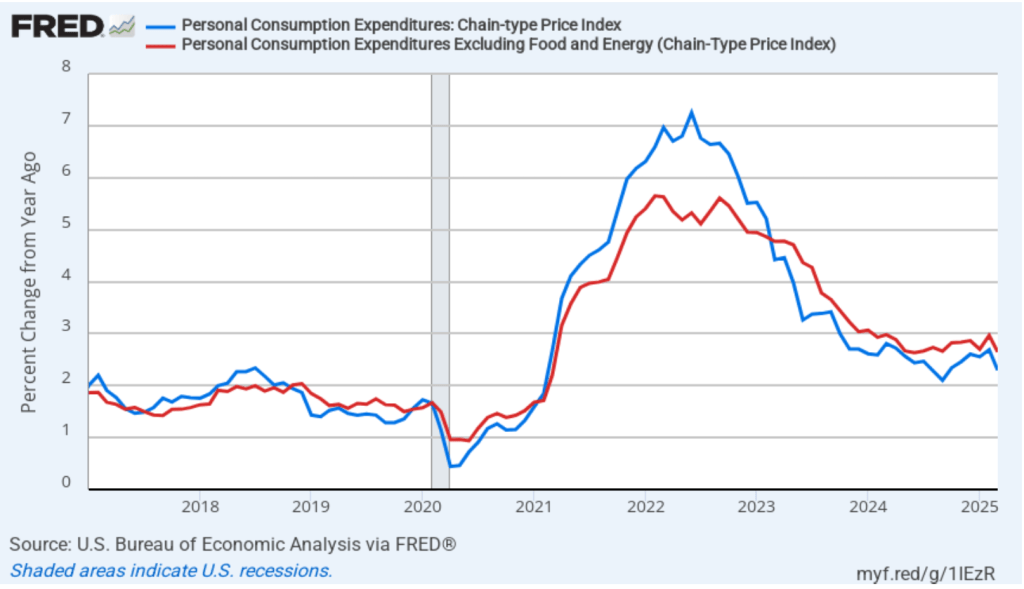

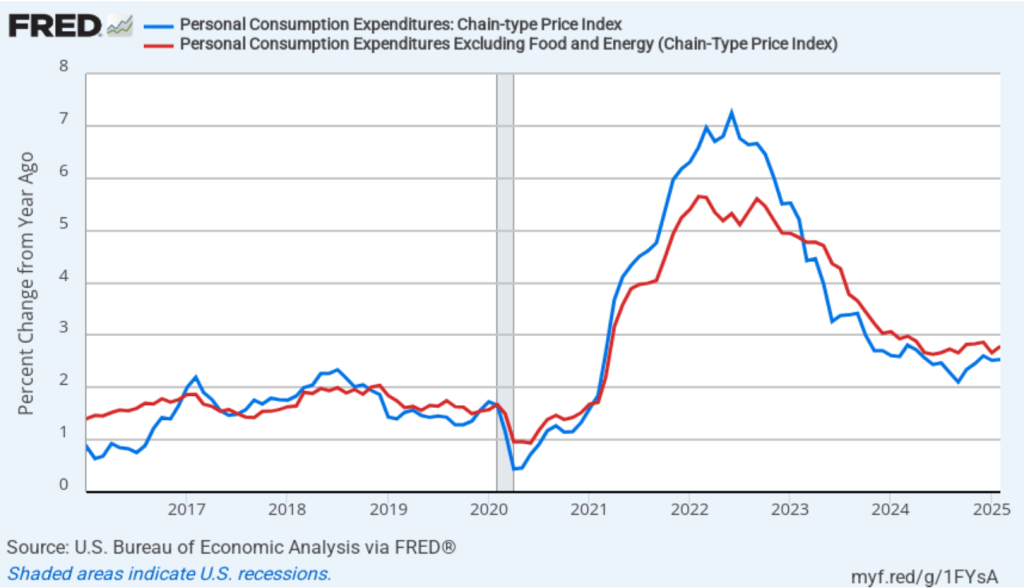

Today (May 30), the BEA released monthly data on the personal consumption expenditures (PCE) price index as part of its “Personal Income and Outlays” report. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2016, with inflation measured as the percentage change in the PCE from the same month in the previous year. In April, PCE inflation was 2.1 percent, down from 2.3 percent in March. Core PCE inflation in April was 2.5 percent, down from 2.7 percent in March. Headline PCE inflation was below the forecast of economists surveyed, while core PCE inflation was consistent with the forecast.

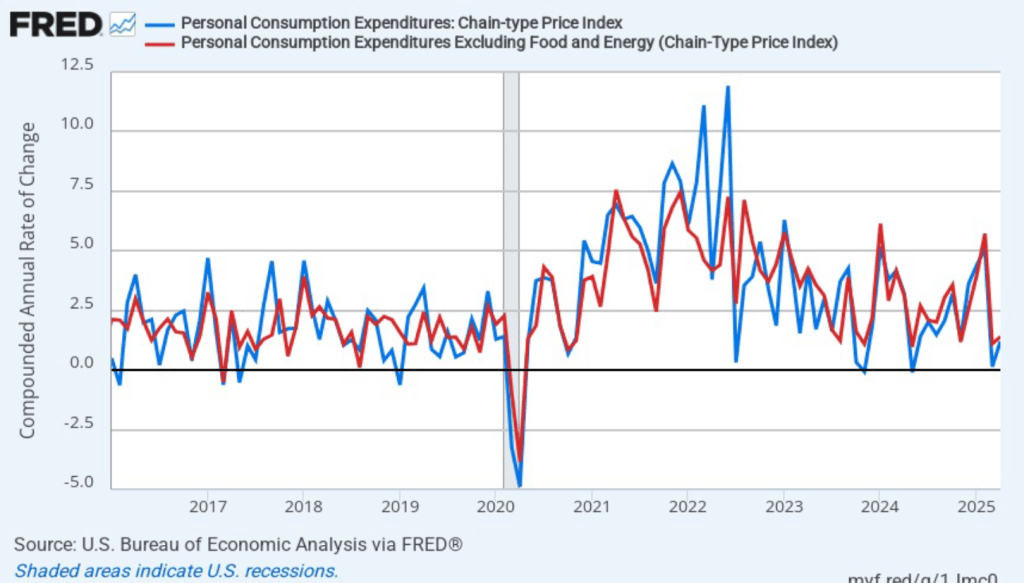

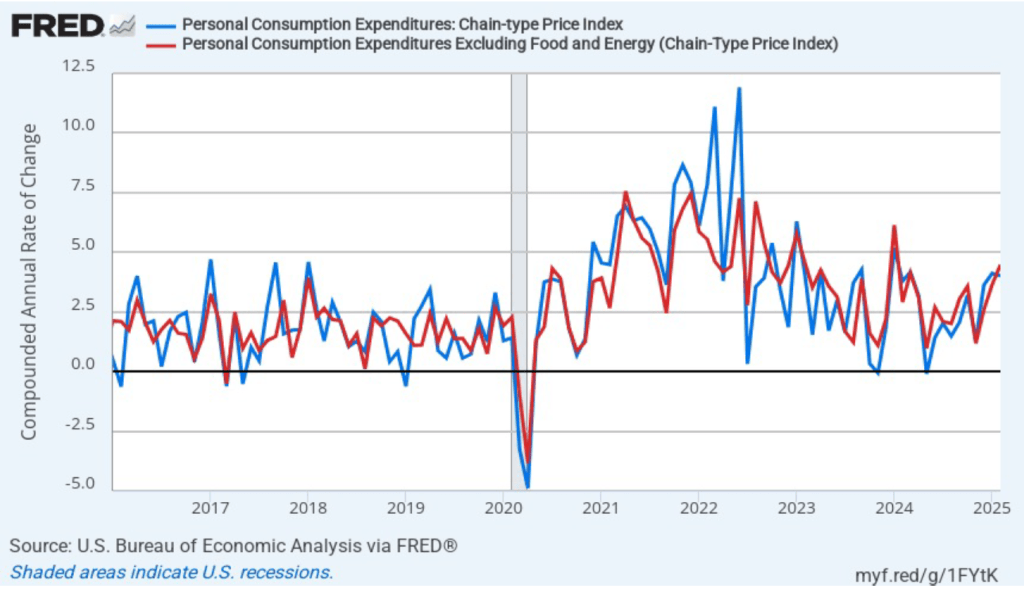

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation increased in April to 1.2 percent from 0.1 percent in March. Core PCE inflation also increased from 1.1 percent in March to 1.4 percent in April. So, both 1-month PCE inflation estimates are well below the Fed’s 2 percent target. The usual caution applies that 1-month inflation figures are volatile (as can be seen in the figure), so we shouldn’t attempt to draw wider conclusions from one month’s data. In addition, because these data are for April, they don’t capture fully the price increases resulting from the tariff increases the Trump administration announced on April 2.

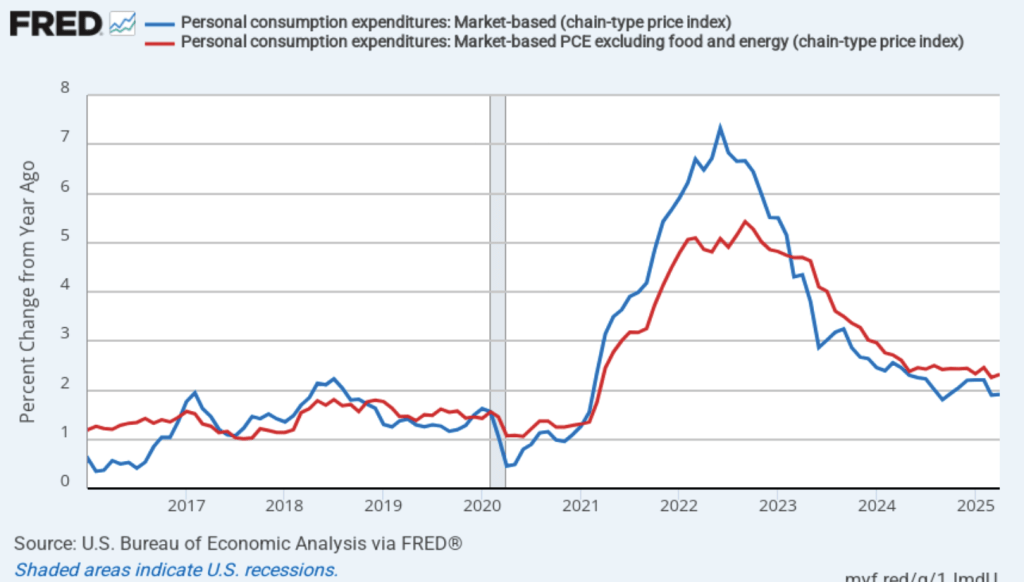

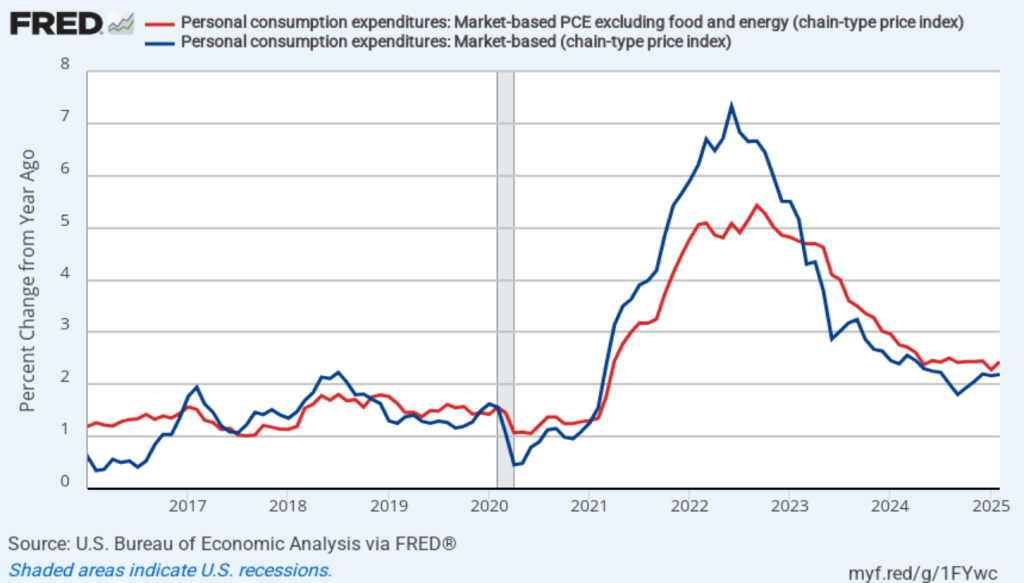

Fed Chair Jerome Powell has noted that inflation in non-market services has been high. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the red line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

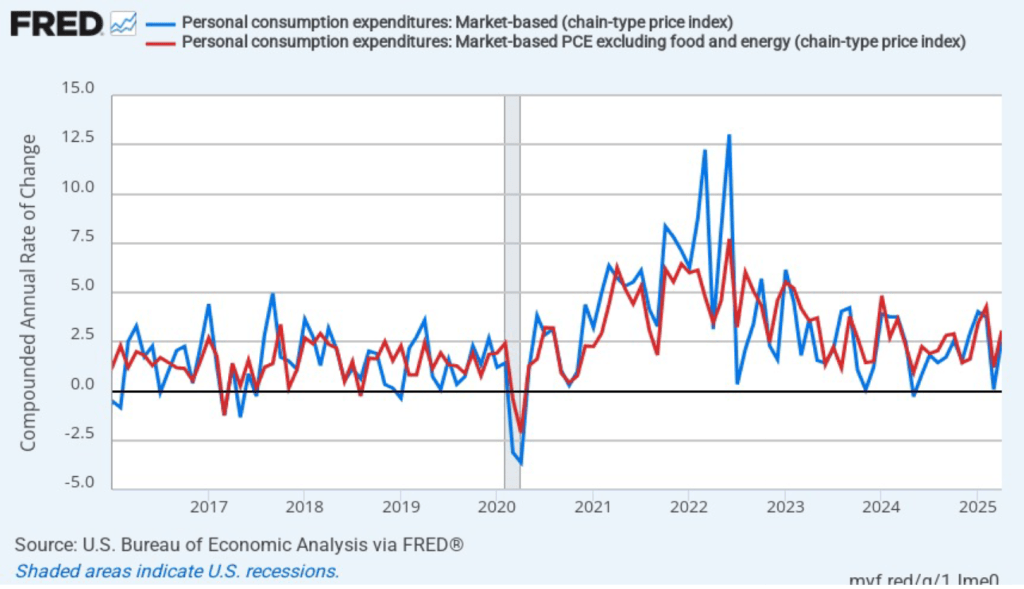

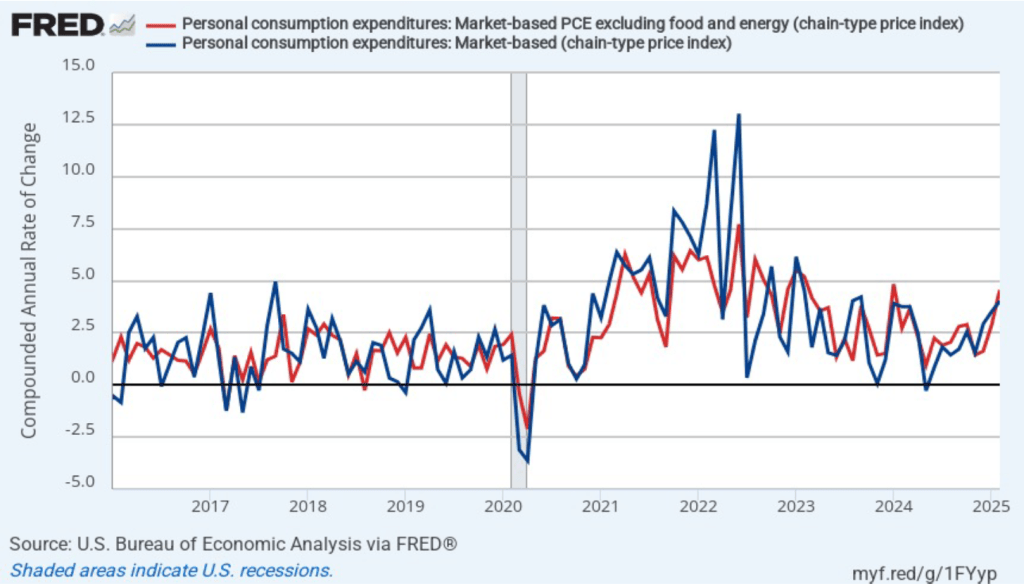

Headline market-based PCE inflation was 1.9 percent in April, unchanged from March. Core market-based PCE inflation was 2.3 percent in April, which was also unchanged from March. So, both market-based measures show about the same rate of inflation in April as the total measures do. In the following figure, we look at 1-month inflation using these measures. The 1-month inflation rates are both higher than the 12-month rates. Headline market-based inflation was 2.6 percent in April, up from 0.1 percent in March. Core market-based inflation was 3.1 percent in April, up from 1.2 percent in March. As the figure shows, the 1-month inflation rates are more volatile than the 12-month rates, which is why the Fed relies on the 12-month rates when gauging how close it is coming to hitting its target inflation rate.

In summary, today’s data provide some evidence that the inflation rate is getting closer to the Fed’s 2 percent annual target. Improving inflation combined with some indications that output growth is slowing—the BEA release indicated that growth in real consumption expenditures slowed in April—might make it more likely that the Fed’s policymaking Federal Open Market Committee (FOMC) will cut its target for the federal funds rate relatively soon.

However, investors who buy and sell federal funds futures contracts expect that the FOMC will leave its federal funds rate target unchanged at its next meetings on June 17–18 and July 29–30. (We discuss the futures market for federal funds in this blog post.) Investors assign a probability 0f 72.6 percent to the FOMC cutting its target at its September 29–30 meeting. Investor expectations reflect the recent statements from Fed Chair Jerome Powell and other members of the FOMC that they intend to wait until the effects of the tariff increases on the economy are clearer before changing the target for the federal funds rate.

Since 1946, the Institute for Social Research (ISR) at the University of Michigan has conducted surveys of consumers. Each month, the ISR interviews a nationwide sample of 900 to 1,000 consumers, asking a variety of questions, including some on inflation.

The results of the University of Michigan surveys are widely reported in the business press. In the latest ISR survey it’s striking how much consumers expect inflation to increase. The median response by those surveyed to the question “By about what percent do you expect prices to go up/down on the average, during the next 12 months?” was 7.3 percent. If this expectation were to prove to be correct, inflation, as measured by the percentage change in the consumer price index (CPI), will have to more than double from its April value of 2.3 percent.

How accurately have consumers surveyed by the ISR predicted future inflation? The question is difficult to answer definitively because the survey question refers only to “prices” rather than to a measure of the price level, such as the consumer price index (CPI). Some people may have the CPI in mind when answering the question, but others may think of the prices of goods they buy regularly, such as groceries or gasoline. Nevertheless, it can be interesting to see how well the responses to the ISR survey match changes in the CPI, which we do in the following figure for the period from January 1978—when the survey began—to April 2024—the last month for which we have CPI data from the month one year in the future.

The blue line shows consumers’ expectations of what the inflation rate will be over the following year. The red line shows the inflation rate in a particular month calculated as the percentage change in the CPI from the same month in the previous year. So, for instance, in February 2023, consumers expected the inflation rate over the next 12 months to be 4.2 percent. The actual inflation, measured as the percentage change in the CPI between February 2023 and February 2024 was 3.2 percent.

The figure shows that consumers forecast inflation reasonably well. As a simple summary, the average inflation rate consumers expected over this whole period was 3.6 percent, while the actual inflation rate was 3.5 percent. So, for the period as a whole, the inflation rate that consumers expected was about the same as the actual inflation rate. The most persistent errors occurred during the recovery from the Great Recession of 2007–2008, particularly the five years from 2011 to 2016. During those five years, consumers expected inflation to be 2.5 percent or more, whereas actual inflation was typically below 2 percent.

Consumers also missed the magnitude of dramatic changes in the inflation rate. For instance, consumers did not predict how much the inflation would increase during the 1978 to 1980 period or during 2021 and early 2022. Similarly, consumers did not expect the decline in the price level from March to October 2009.

The two most recent expected inflation readings are 6.5 percent in April and, as noted earlier, 7.3 percent in May. In other words, the consumers surveyed are expecting inflation in April and May 2026 to be much higher than the 2 percent to 3 percent inflation rate most economists and Fed policymakers expect. For example, in March, the median forecast of inflation at the end of 2026 by the members of the Fed’s policymaking Federal Open Market Committee (FOMC) was only 2.2 percent. (Note, though, that FOMC members are projecting the percentage change in the personal consumption expenditures (PCE) price index rather than the percentage change in the CPI. CPI inflation has typically been higher than PCE inflation. For instance, in the period since January 1978, average CPI inflation was 3.6 percent, while average PCE inflation was 3.1 percent).

If economists and policymakers are accurately projecting inflation in 2026, it would be an unusual case of consumers in the ISR survey substantially overpredicting the rate of inflation. One possibility is that news reports of the effect of the Trump Administration’s tariff policies on the inflation rate may have caused consumers to sharply increase the inflation rate they expect next year. If, as seems likely, the tariff increases end up being much smaller than those announced on April 2, the inflation rate in 2026 may be lower than the consumers surveyed expect.

Image generated by ChatGTP-4o of a family shopping in a supermarket.

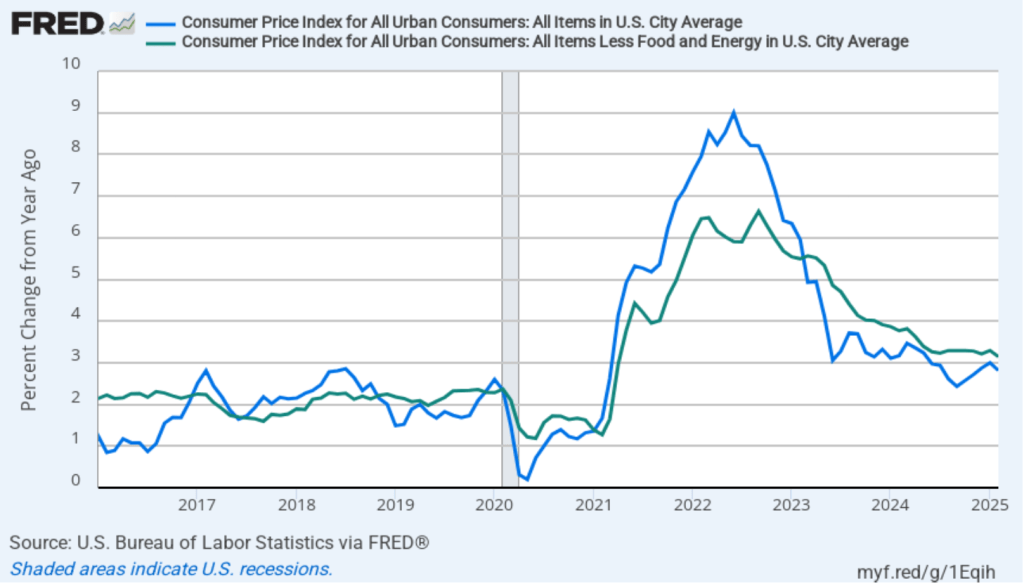

Today (May 13), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for April. The following figure compares headline inflation (the blue line) and core inflation (the green line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.3 percent in April—down from 2.4 percent in March.

The core inflation rate,which excludes the prices of food and energy, was 2.8 percent in April—unchanged from March.

Headline inflation was the lowest since February in 2021—before the acceleration in inflation that began in the spring of 2021. Core inflation was the lowest since March 2021. Both headline inflation and core inflation were what economists surveyed had expected.

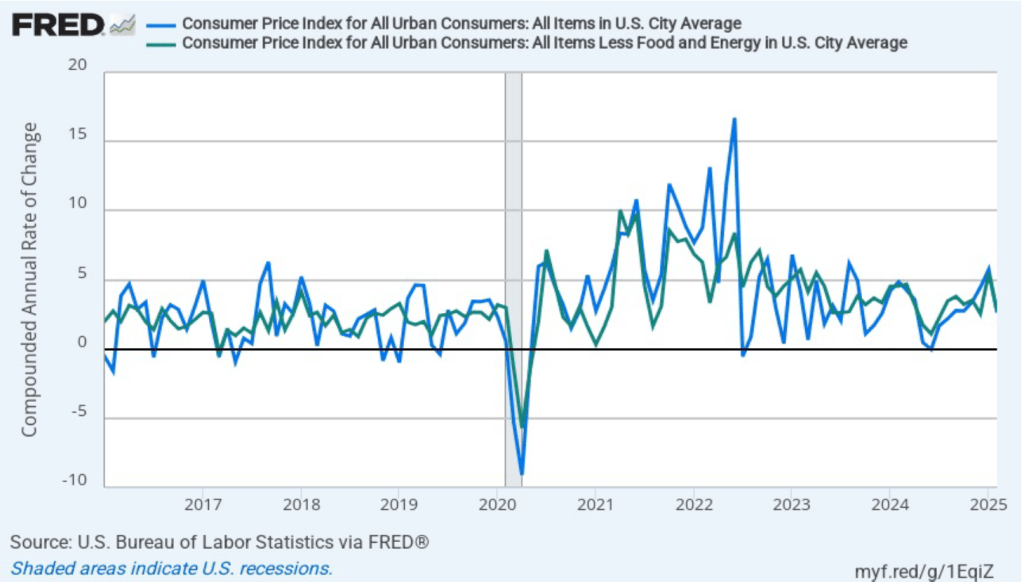

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) rose from –0.6 percent in March to 2.7 percent in April. Core inflation (the red line) rose from 0.9 percent in March to 2.9 percent in April.

The 1-month and 12-month inflation rates are telling different stories, with 12-month inflation indicating that the rate of price increase is back to what it was in early 2021. The 1-month inflation rate indicates a significant increase in April from the very low rate of price increase in March. The 1-month inflation rate indicates that inflation is still running ahead of the Fed’s 2 percent annual inflation target.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that 1-month inflation is particularly volatile. It is possible, though, that the increase in 1-month inflation in April reflects the effect on the price level of the large tariff increases the Trump Administration announced on April 2. Whether those effects will persist is unclear because the administration has been engaged in negotiations that may significantly reduce the tariff increases announced in April. Finally, note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

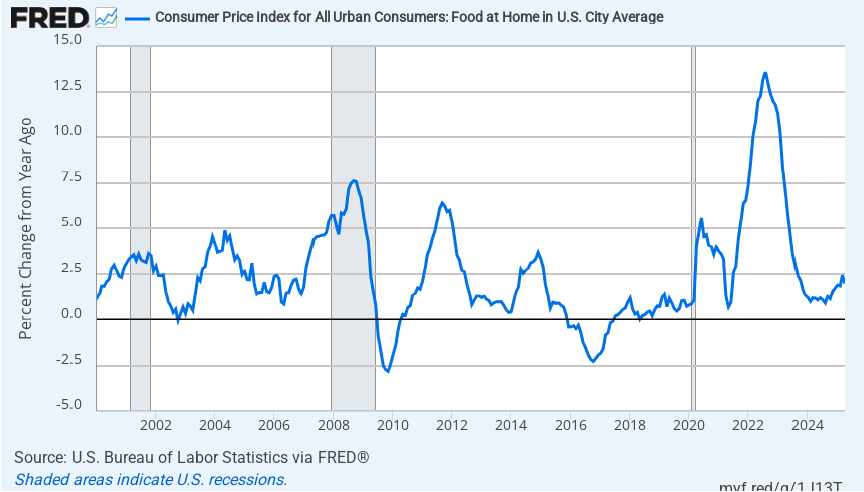

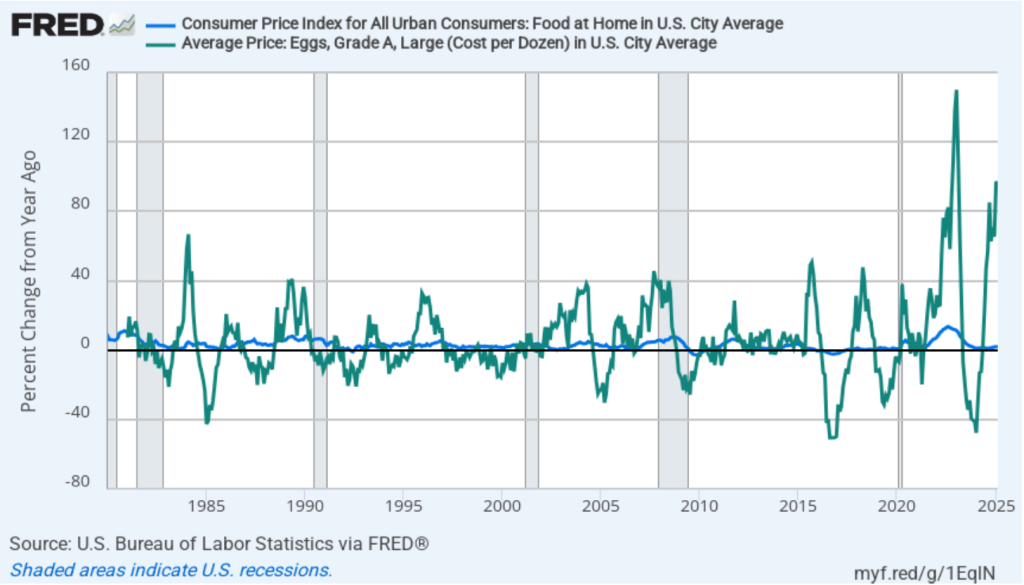

There’s been considerable discussion in the media about continuing inflation in grocery prices. The following figure shows inflation in the CPI category “food at home,” which is primarily grocery prices. Inflation in grocery prices was 2.0 percent in April and has been below 2.5 percent every month since September 2023. Over the past year, there has been a slight upward trend in inflation in grocery prices but to this point it remains relatively low, although well above the very low rates of inflation in grocery prices that prevailed from 2015 to 2019.

It’s the nature of the CPI that in any given month some prices will increase rapidly while other prices will increase slowly or even decline. Although, on average, grocery price inflation has been relatively low, there have been substantial increases in the prices of some food items. For instance, a recent article in the Wall Street Journal noted that rising cattle prices will likely be reflected in coming months rising prices for beef purchased in supermarkets. The following figure shows inflation in the prices of ground beef and steaks over the period starting in January 2015. As we should expect, the prices of these two goods are more volatile mont to month than are grocery prices as a whole. Ground beef prices increased 10.8 percent in April, an increase that will likely be noticeable to someone planning for a Memorial Day cookout.

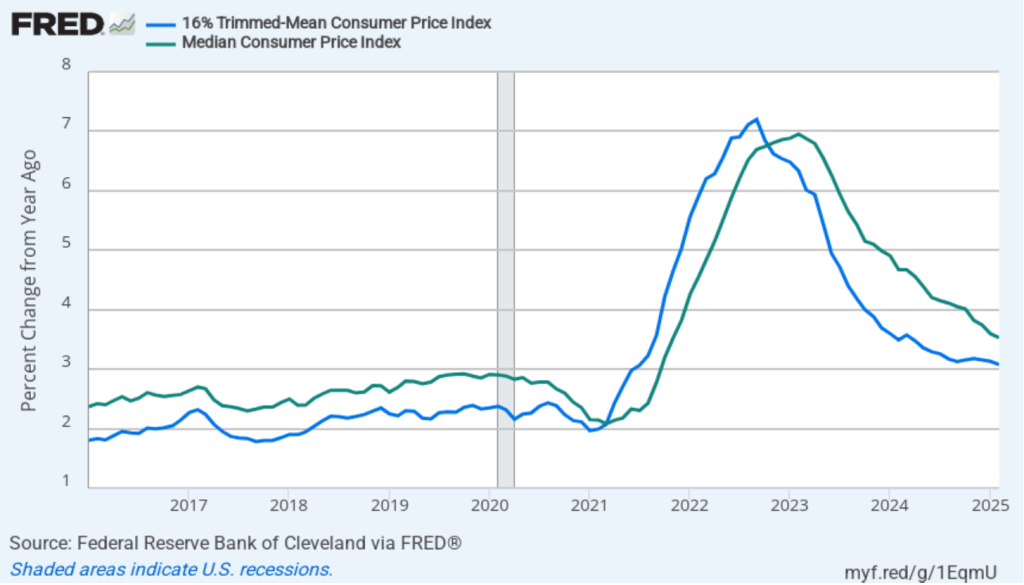

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.0 percent in April, unchanged from March. Twelve-month median inflation (the red line) 3.5 percent in April, also unchanged from March.

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation increased from 2.6 percent in March to 3.0. percent in April. One-month median inflation declined from 4.2 percent in March to 4.0 percent in April. These data, although mixed, provide some confirmation that inflation likely increased somewhat from March to April.

What are the implications of this CPI report for the actions the FOMC may take at its next several meetings? Investors who buy and sell federal funds futures contracts still do not expect that the FOMC will cut its target for the federal funds rate at its next two meetings. (We discuss the futures market for federal funds in this blog post.) Today, investors assigned only an 8.4 percent probability to the Fed’s policymaking Federal Open Market Committee (FOMC) cutting its target from the current 4.25 percent to 4.50 percent range at its meeting on June 17–18. Investors assigned a probability of 34.9 percent that the FOMC will cut its target after its meeting on July 29–30. Investors assigned a probability of 73.1 percent that the committee will cut its target after its meeting on September 16–17. The FOMC’s actions will likely depend in part on the success of the current trade negotiations.

Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (May 7) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee made one significant change to the wording in its statement following its last meeting on March 19. The committee added the words in bold to the following sentence:

“The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.”

The key event since the last FOMC meeting was President Trump’s announcement on April 2 that he would implement tariff increases that were much higher than had previously been expected.

As we noted in an earlier blog post, an unexpected increase in tariff rates will result in an aggregate supply shock to the economy. As we discuss in Macroeconomics, Chapter 13,Section 13.3 (Economics, Chapter 23, Section 23.3), an aggregate supply shock puts upward pressure on the price level at the same time as it causes a decline in real GDP and employment. The result, as the FOMC statement indicates, can be both rising inflation and rising unemployment. If higher inflation and higher unemployment persist, the U.S. economy would be experiencing stagflation. The United States last experienced stagflation during the 1970s when large increases in oil prices caused an aggregate supply shock.

During his press conference following the meeting, Fed Chair Jerome Powell indicated that the increase in tariffs might the Fed’s dual mandate goals of price stability and maximum employment “in tension” if both inflation and unemployment increase. If the FOMC were to increase its target for the federal funds rate in order to slow the growth of demand and bring down the inflation rate, the result might be to further increase unemployment. But if the FOMC were to cut its target for the federal funds rate to increase the growth of demand and reduce the unemployment rate, the result might be to further increase the inflation rate.

Powell emphasized during his press conference that tariffs had not yet had an effect on either inflation or unemployment that was large enough to be reflected in macroeconomic data—as we’ve noted in blog posts discussing recent macroeconomic data releases. As a result, the consensus among committee members is that it would be better to wait to future meetings before deciding what changes in the federal funds rate might be needed: “We’re in a good position to wait and see. We don’t have to be in a hurry.”

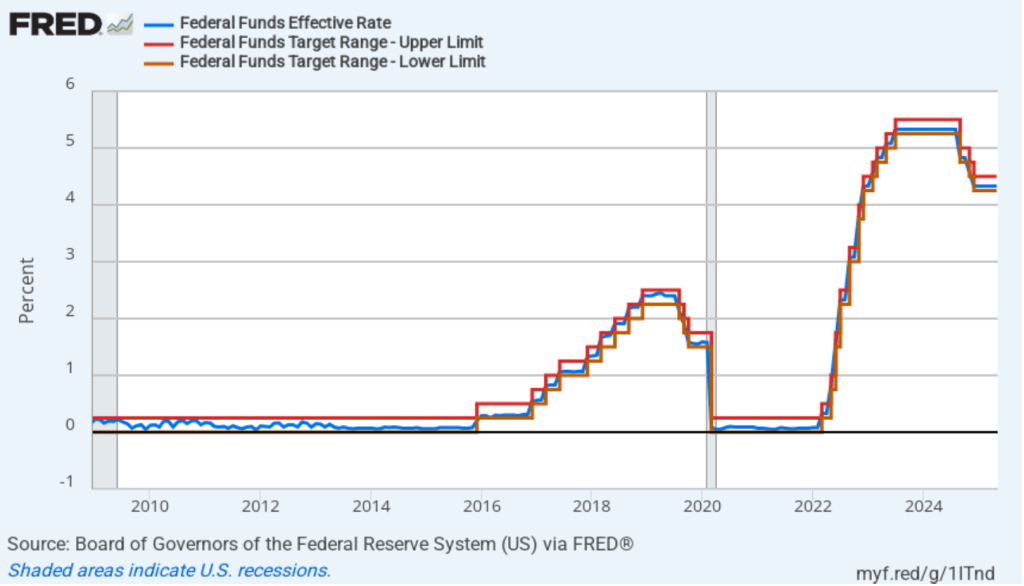

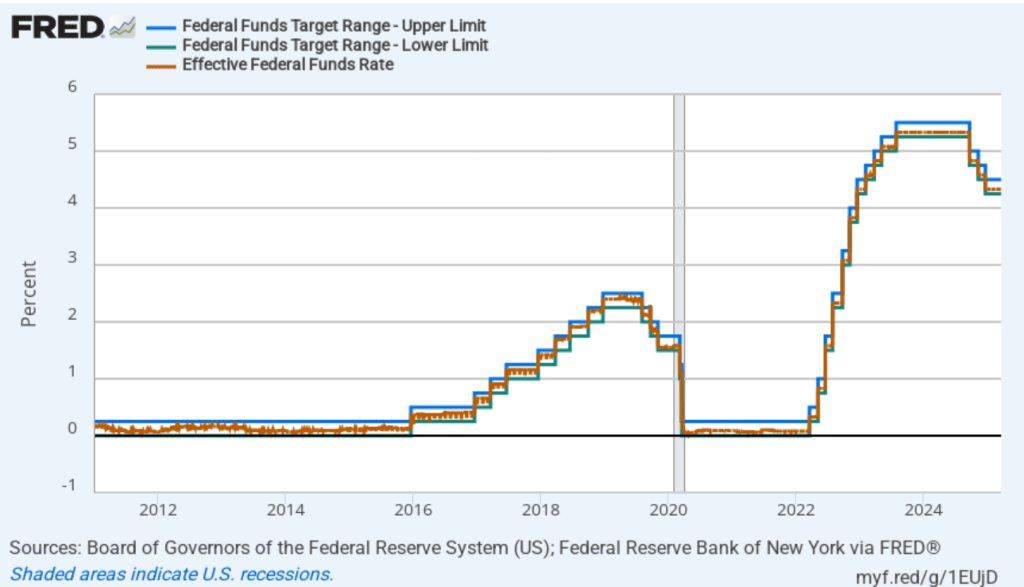

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed is successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

In his press conference, Powell indicated that when the committee would change its target for the federal funds rate was dependent on the trends in macroeconomic data on inflation, unemployment, and output during the coming months. He noted that if both unemployment and inflation significantly increased, the committee would focus on which variable had moved furthest from the Fed’s target. He also noted that it was possible that neither inflation nor unemployment might end up significantly increasing either because tariff negotiations lead to lower tariff rates or because the economy proves to be better able to deal with the effects of tariff increases than many economist now expect.

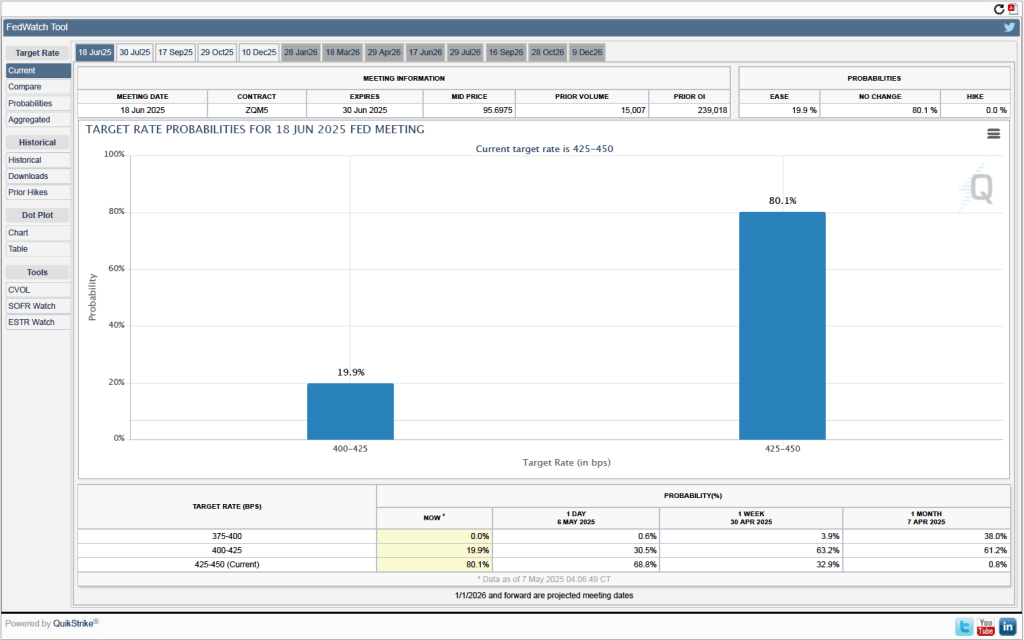

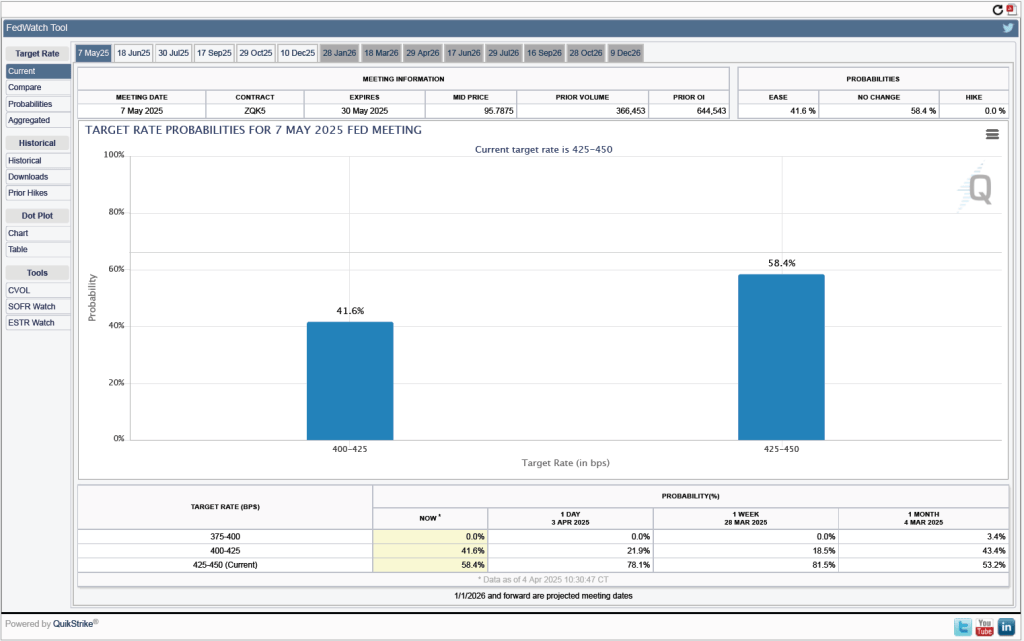

One indication of expectations of future changes in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 17–18 meeting. As shown in the following figure, investors assign a 80.1 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

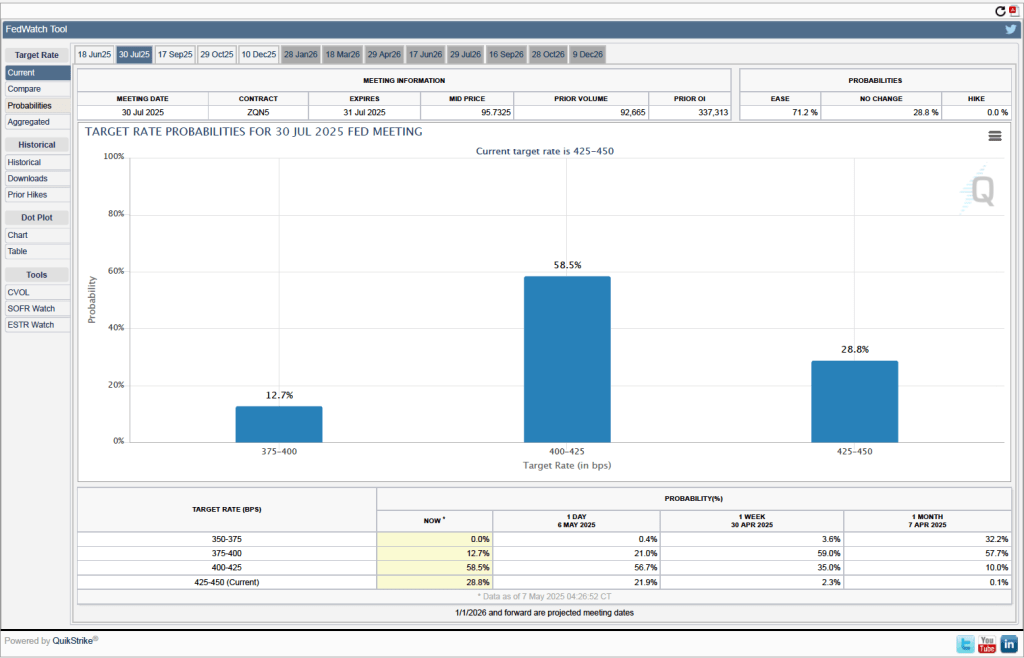

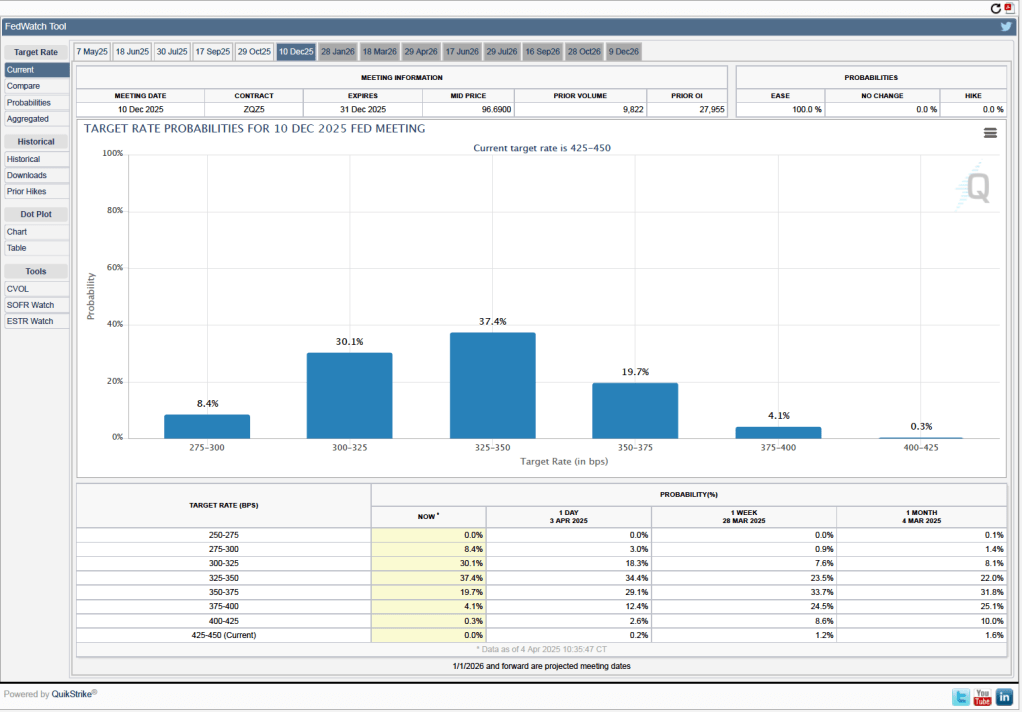

When will the Fed likely cut its target for the federal funds rate? As the following figure shows, investors expect it to happen at the FOMC’s July 29–30 meeting. Investors assign a probably of 58.5 percent to the committee cutting its target by 0.25 percentage point (25 basis points) at that meeting and a probability of 12.7 percent to the committee cutting its target by 50 basis points. Investors assign a probability of only 28.8 percent to the committee leaving its target unchanged.

Image created by ChatGTP=4o of workers on an automobile assembly line.

We noted in a blog post earlier this week that although the preliminary estimate from the Bureau of Economic Analysis (BEA) indicated that real GDP had declined during the first quarter of 2025, the report didn’t provide a clear indication that the U.S. economy was in recession. This morning (May 2), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for April. The data in the report also show no sign that the U.S. economy is in a recession. Although there have been many stories in the media about businesspeople becoming increasingly pessimistic, we don’t yet see it in the employment data. We should add two caveats, however: 1. The effects of the large tariff increases the Trump Administration announced on April 2 are likely not reflected in the data from this report, and 2. at the beginning of a recession the data in the jobs report can be subject to large revisions.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

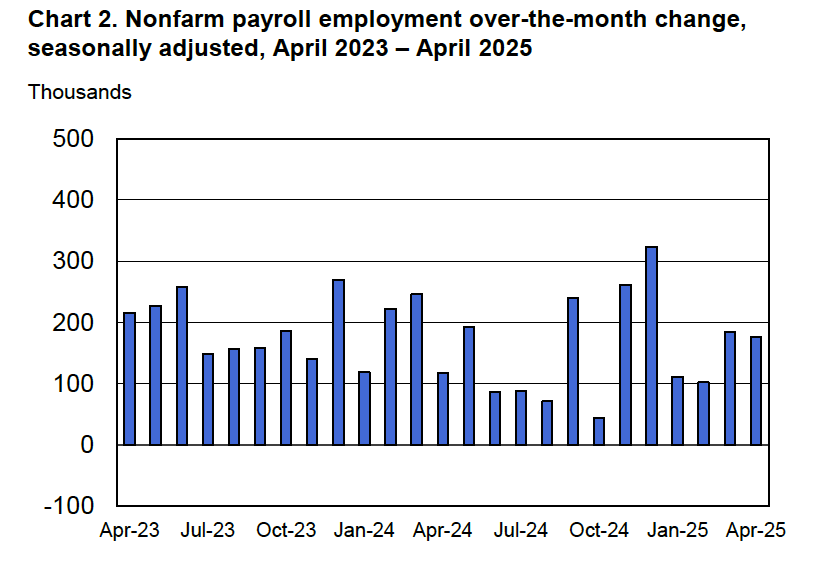

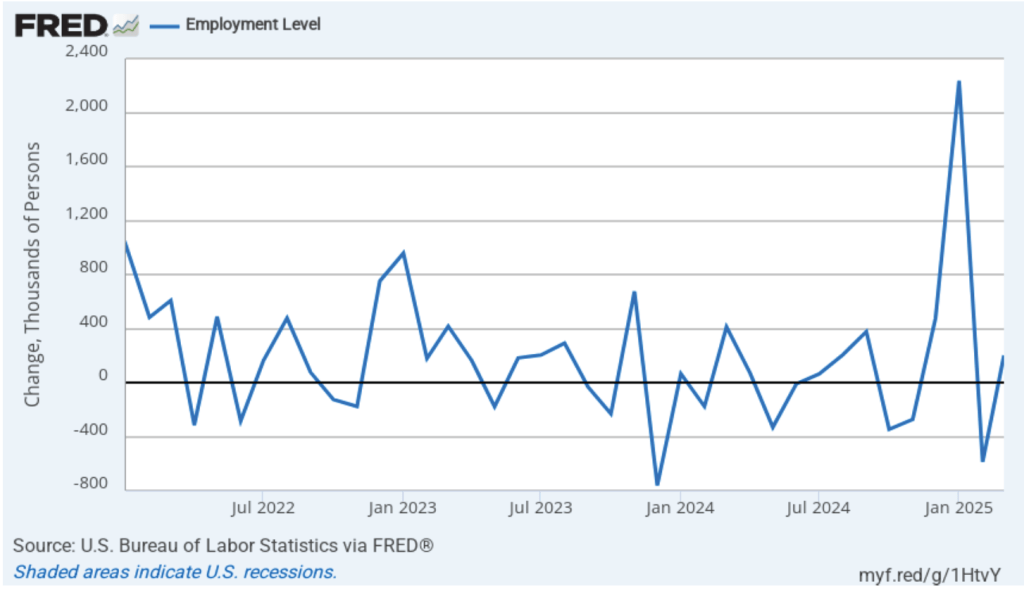

According to the establishment survey, there was a net increase of 177,000 jobs during April. This increase was well above the increase of 135,000 that economists surveyed had forecast. Somewhat offsetting this unexpectedly large increase was the BLS revising downward its previous estimates of employment in February and March by a combined 58,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in payroll employment for each month in the last two years.

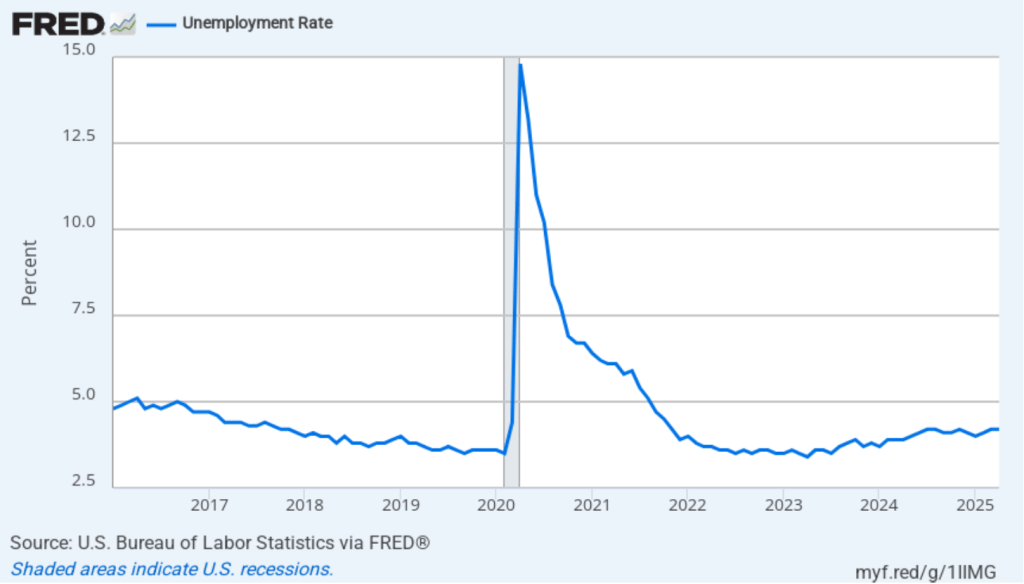

The unemployment rate was unchanged to 4.2 percent in April. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

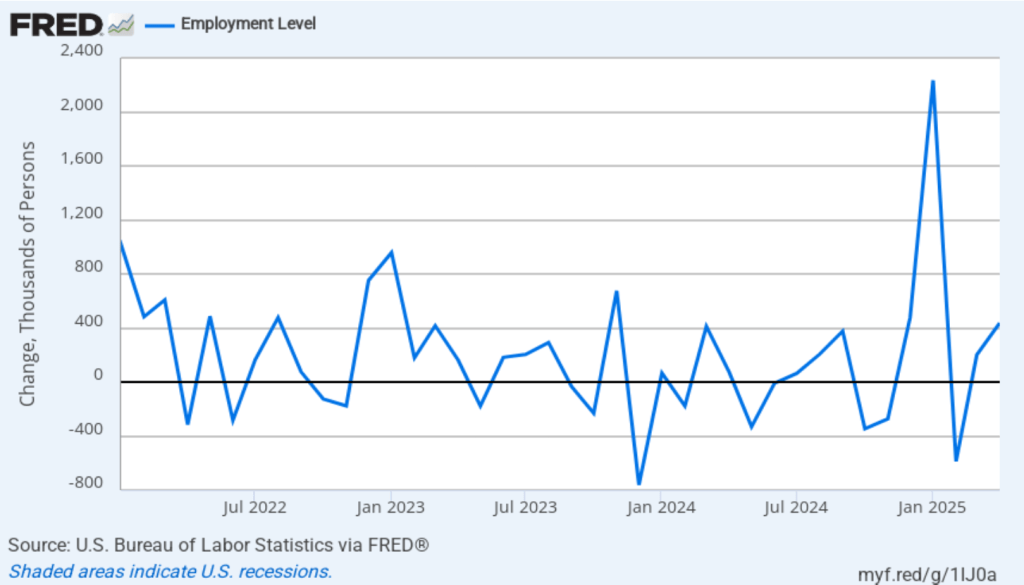

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 436,000 jobs in April, following an increase of 201,000 jobs in March. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, however, both surveys showed net jobs increasing. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

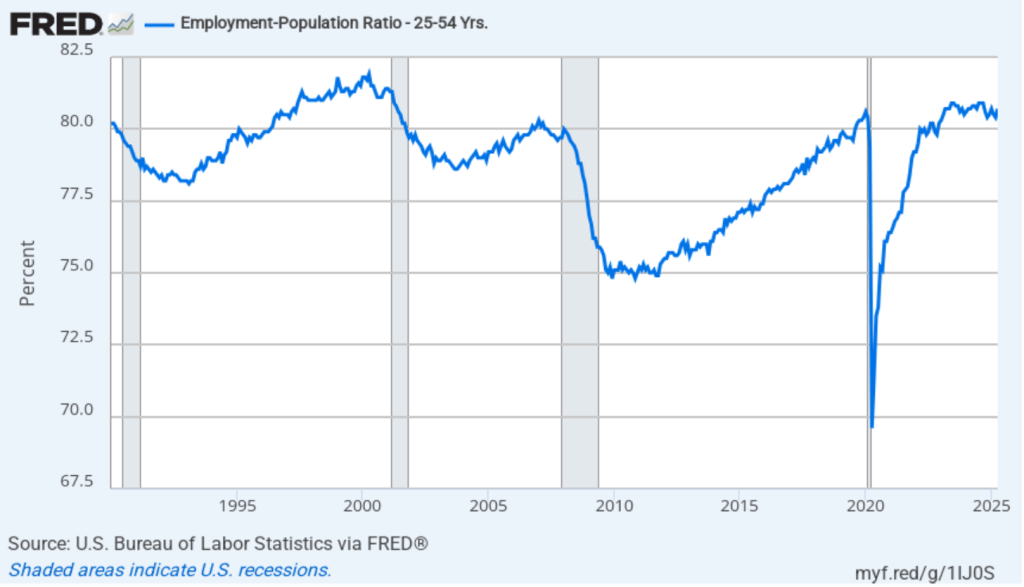

The household survey has another indication of continuing strength in the labor market. The employment-population ratio for prime age workers—those aged 25 to 54—increased from 80.4 percent in March to 80.7 percent in April. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to January 2020.

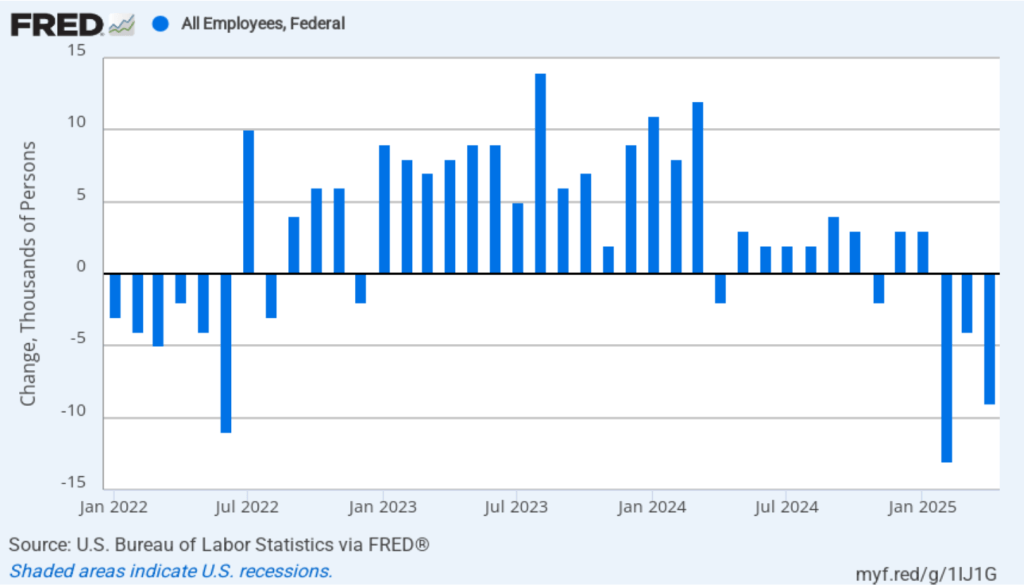

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 9,000 in April. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may find a more significant decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

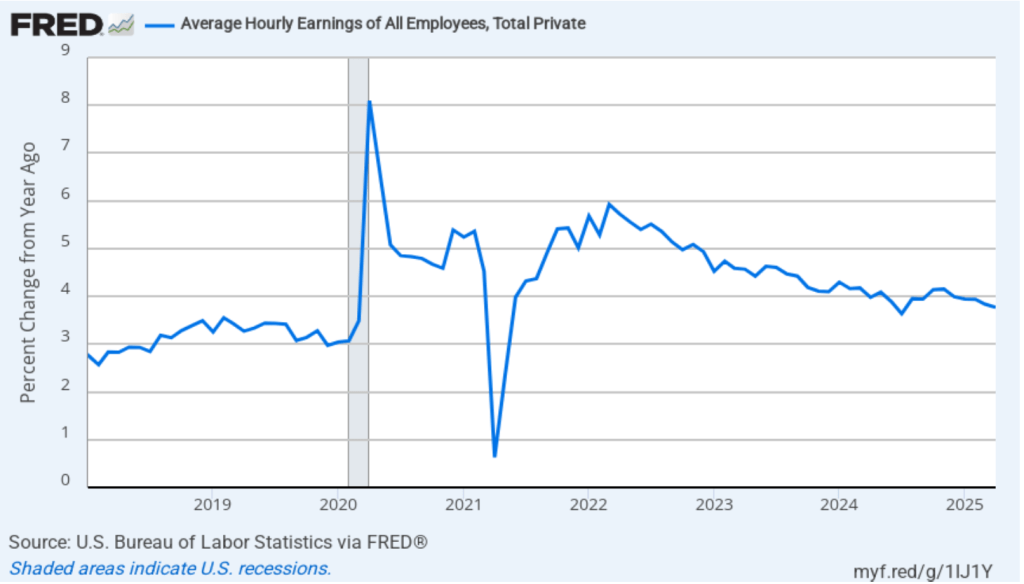

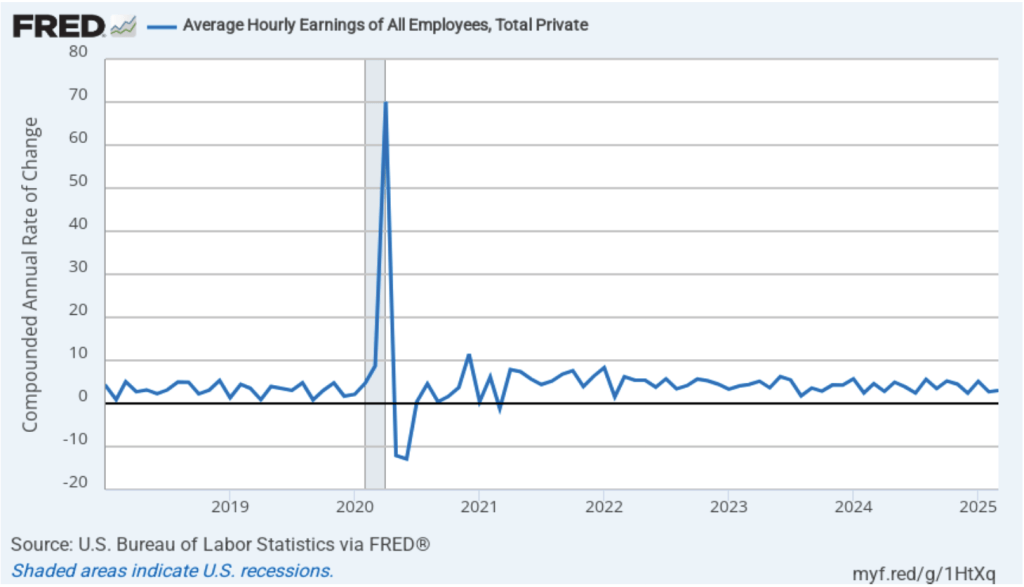

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.8 percent in April, which is unchanged from the March increase.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. The April, the 1-month rate of wage inflation was 2.0 percent, down from 3.4 percent in March. If the 1-month increase in AHE is sustained, it would contribute to the Fed’s achieving its 2 percent target rate of price inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s unexpectedly large tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

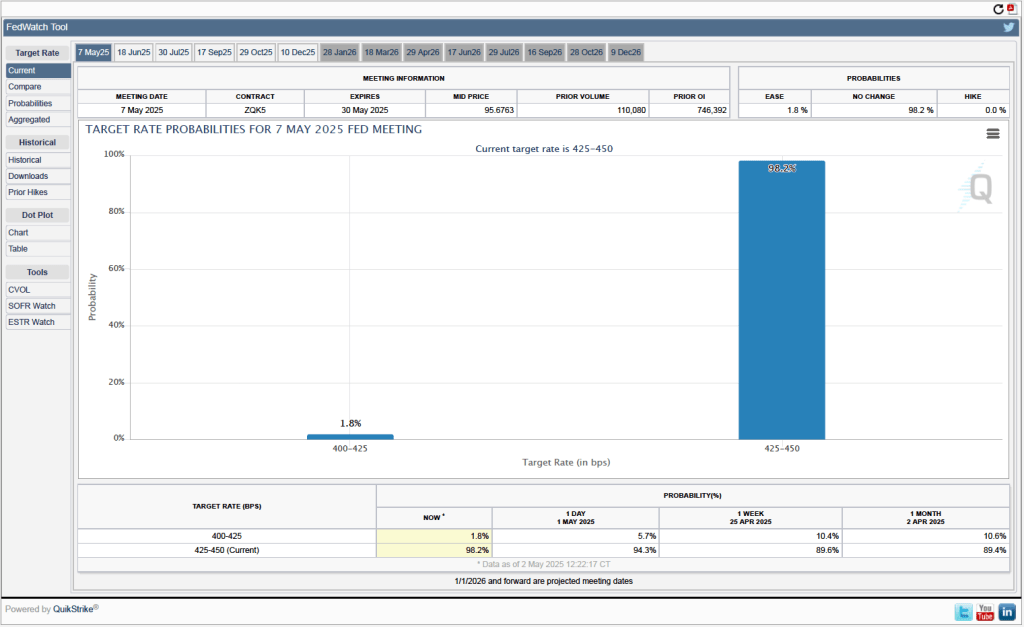

One indication of expectations of future changes in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the surprisingly large tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 6–7 meeting. As shown in the following figure, investors assign a 98.2 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

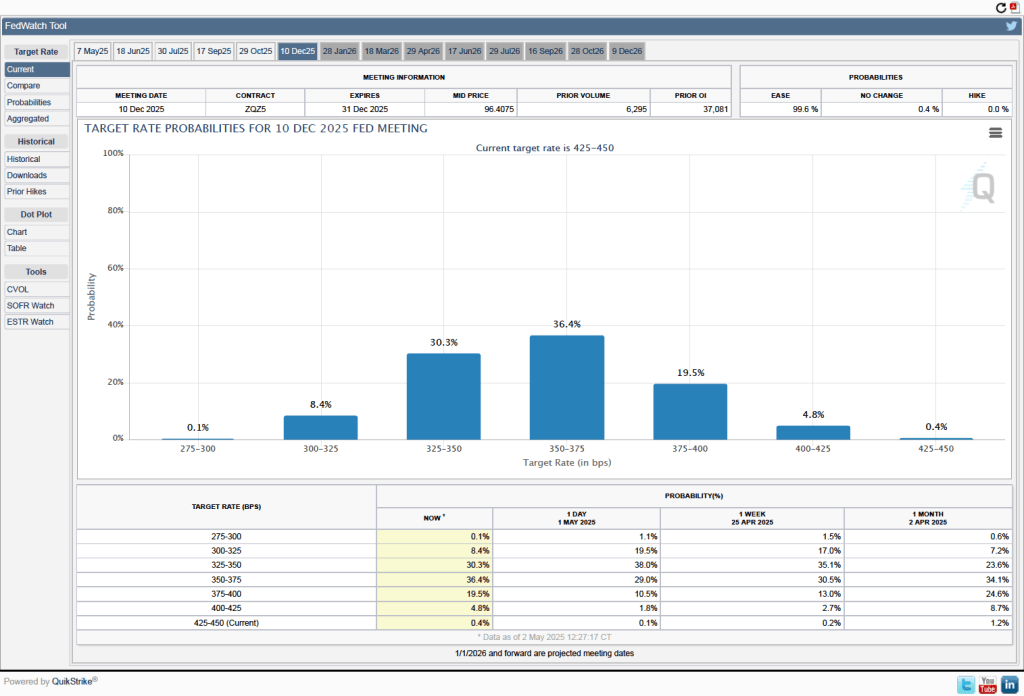

It’s a different story if we look at the end of the year. As the following figure shows, investors now expect that by the end of the FOMC’s meeting on December 9-10, the committee will have implemented at least three 0.25 percentage point (25 basis points) cuts in its target range for the federal funds rate. Investors assign a probability of 75.9 percent that the target range will end the year at 3.50 percent to 3.75 percent or lower. At their March meeting, FOMC members projected only two 25 basis point cuts this year—but that was before the announcement of the unexpectedly large tariff increases.

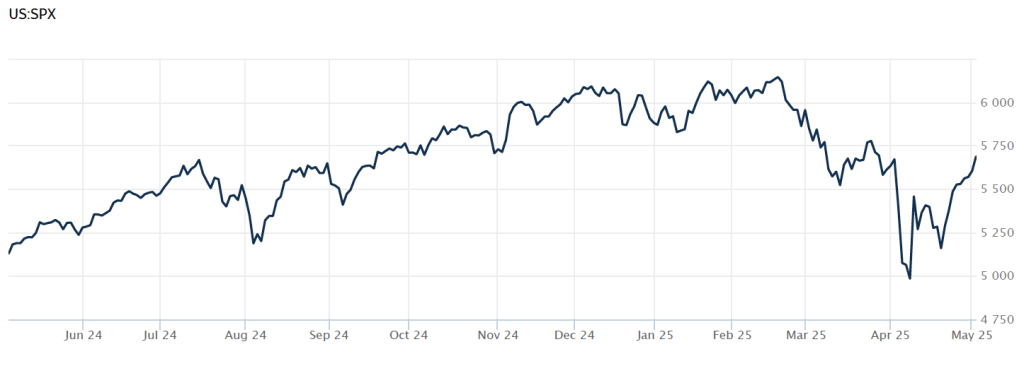

How the economy will fare for the remainder of the year depends heavily on what happens with respect to tariffs. News today that China and the United States may be negotiating lower tariff rates has contributed to rising stock prices. The following figure from the Wall Street Journal shows movements in the S&P stock index over the past year. The index declined sharply on April 2, following President Trump’s announcement of the tariff increases. As of 2 pm today, the S&P index has risen above its value on April 1, meaning that it has recovered all of the losses since the announcement of the tariff increases. The increase in stock prices likely indicates that investors expect that the tariff increases will end up being much smaller than those originally announced and that the chances of a recession happening soon are lower than they appeared to be on April 2.

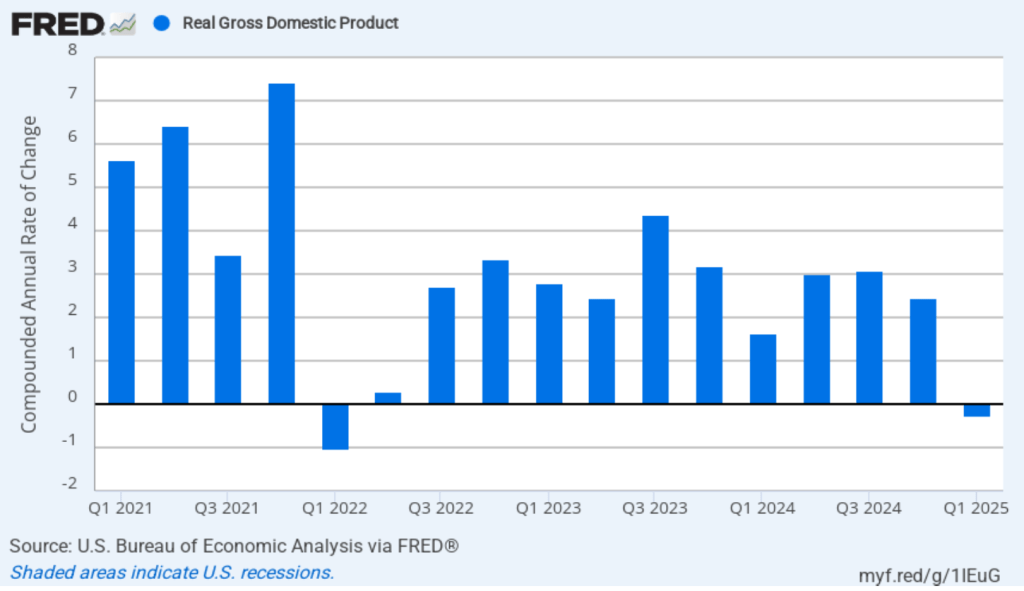

This morning (April 30), the Bureau of Economic Analysis (BEA) released its advance estimate of GDP for the first quarter of 2025. (The report can be found here.) The BEA estimates that real GDP fell by 0.3 percent, measured at an annual rate, in the first quarter—January through March. Economists surveyed had expected an 0.8 percent increase. Real GDP grew by an estimated 2.5 percent in the fourth quarter of 2024. The following figure shows the estimated rates of GDP growth in each quarter beginning in 2021.

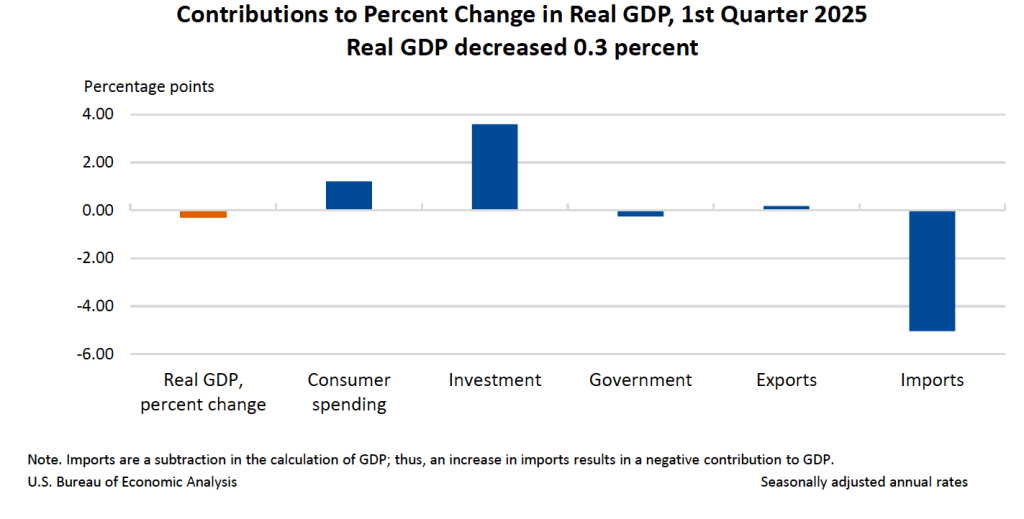

As the following figure—taken from the BEA report—shows, the increase in imports was the most important factor contributing to the decline in real GDP. The quarter ended before the Trump Administration announced large tariff increases on April 2, but the increase in imports is likely attributable to firms attempting to beat the tariff increases they expected were coming.

It’s notable that the change in real private inventories was a large $140 billion, which contributed 2.3 percentage points to the change in real GDP. Again, it’s likely that the large increase in inventories represented firms stockpiling goods in anticipation of the tariff increases.

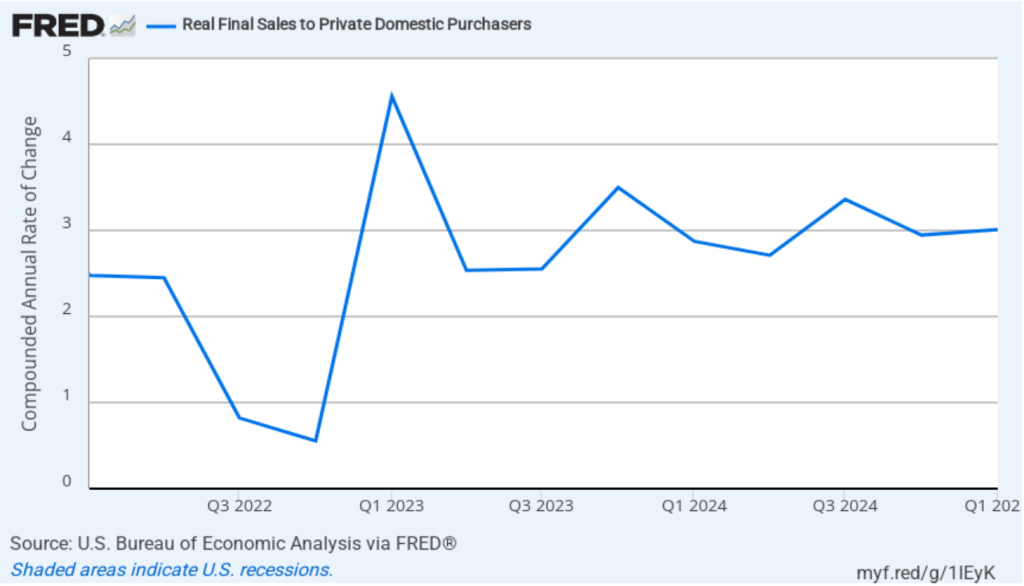

One way to strip out the effects of imports, inventory investment, and government purchases—which can also be volatile—is to look at real final sales to domestic purchasers, which includes only spending by U.S. households and firms on domestic production. As the following figure shows, real final sales to domestic purchasers increase by 3.0 percent in the first quarter of 2024, which was a slight increase from the 2.9 percent increase in the fourth quarter of 2024. The large difference between the change in real GDP and the change in real final sales to domestic purchasers is an indication of how strongly this quarter’s national income data were affected by businesses anticipating the tariff increases.

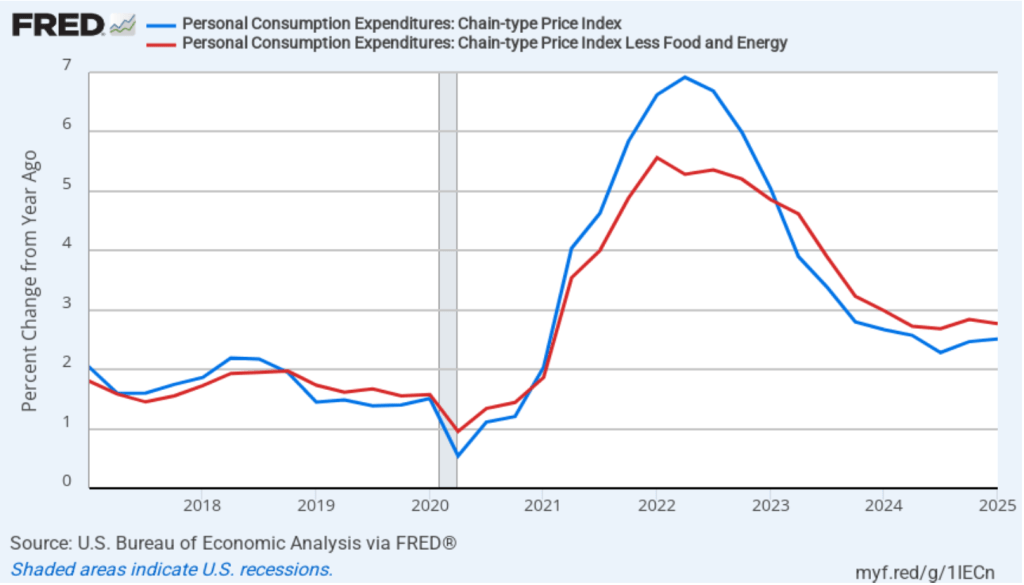

In the separate “Personal Income and Outlays” report that the BEA also released this morning, the bureau reported monthly data on the personal consumption expenditures (PCE) price index. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2017 with inflation measured as the percentage change in the PCE from the same month in the previous year. In March, PCE inflation was 2.3 percent, down from 2.7 percent in February. Core PCE inflation in March was 2.6 percent, down from 3.0 percent in February. Both headline and core PCE inflation were higher than the forecasts of economists surveyed.

The BEA also released quarterly PCE data as part of its GDP report. The following figure shows quarterly headline PCE inflation (the blue line) and core PCE inflation (the red line). Inflation is calculated as the percentage change from the same quarter in the previous year. Headline PCE inflation in the first quarter was 2.5 percent, unchanged from the fourth quarter of 2025. Core PCE inflation was 2.8 percent, also unchanged from the fourth quarter of 2025. Both measures were still above the Fed’s 2 percent inflation target.

The following figure shows quarterly PCE inflation and quarterly core PCE inflation calculated by compounding the current quarter’s rate over an entire year. Measured this way, headline PCE inflation increased from 2.4 percent in the fourth quarter of 2024 to 3.6 percent in the first quarter of 2025. Core PCE inflation increased from 2.6 percent in the fourth quarter of 2024 to 3.5 percent in the first quarter of 2025. Clearly, the quarterly data show significantly higher inflation than do the monthly data. As we discuss in this blog post, tariff increases result in an aggregate supply shock to the economy. As a result, unless the current and scheduled tariff increases are reversed, we will likely see a significant increase in inflation in the coming months. So, neither the monthly nor the quarterly PCE data may be giving a good indication of the course of future inflation.

What should we make of today’s macro data releases? First, it’s important to remember that these data will be subject to revisions in coming months. If we are heading into a recession, the revisions may well be very large. Second, we are sailing into unknown waters because the U.S. economy hasn’t experienced tariff increases as large as these since passage of the Smoot-Hawley Tariff in 1930. Third, at this point we don’t know whether some, most, all, or none of the tariff increases will be reversed as a result of negotiations during the coming weeks. Finally, on Friday, the Bureau of Labor Statistics will release its “Employment Situation Report” for March. That report will provide some additional insight into the state of the economy—as least as it was in March before the full effects of the tariffs have been felt.

As we’ve noted in earlier posts, according to the usually reliable GDPNow forecast from the Federal Reserve Bank of Atlanta, real GDP in the first quarter of 2025 will decline by 2.8 percent. This morning (April 4), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for March. The data in the report show no sign that the U.S. economy is in a recession. We should add two caveats, however: 1. The effects of the unexpectedly large tariff increases announced this week by the Trump Administration are not reflected in the data from this report, and 2. at the beginning of a recession the data in the jobs report can be subject to large revisions.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

According to the establishment survey, there was a net increase of 228,000 jobs during March. This increase was well above the increase of 140,000 that economists had forecast. Somewhat offsetting this unexpectedly large increase was the BLS revising downward its previous estimates of employment in January and February by a combined 48,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in payroll employment for each month in the last two years.

The unemployment rate rose slightly to 4.2 percent in March from 4.1 percent in February. As the following figure shows, the unemployment rate has been remarkably stable in recent months, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 201,000 jobs in March, following a sharp decrease of 588,000 jobs in February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, however, both surveys showed roughly the same net job increase. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

One concerning sign in the household survey is the fall in the employment-population ratio for prime age workers—those aged 25 to 54. The ratio declined from 80.5 percent in February to 80.4 percent in March. Although the prime-age employment-population is still high relative to the average level since 2001, it’s now well below the high of 80.9 percent in mid-2024. Continuing declines in this ratio would indicate a significant softening in the labor market.

It’s unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 4,000 in March. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may find a more significant decline in federal employment.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.8 percent in March, down from 4.0 percent in February.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. The March 1-month rate of wage inflation was 3.0 percent, up from 2.7 percent in February. Whether measured as a 12-month increase or as a 1-month increase, AHE is still increasing somewhat more rapidly than is consistent with the Fed achieving its 2 percent target rate of price inflation.

Taken by itself, today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. There are some indications that the economy may be weakening, as shown by some of the data in the jobs report and by some of the data incorporated by the Atlanta Fed in its pessimistic nowcast of first quarter real GDP. But the Fed hasn’t yet brought inflation down to its 2 percent annual target.

Looming over monetary policy is the fallout from the Trump Administration’s implementation of unexpectedly large tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

The effect of the tariffs poses a dilemma for the Fed. With inflation still running above the 2 percent annual target, additional upward pressure on the price level is unwelcome news. The dramatic decline in both stock prices and in the interest rate on the 10-Treasury note indicate that investors are concerned that the tariffs increases may push the U.S. economy into a recession. The FOMC can respond to the threat of a recession by cutting its target for the federal funds rate, but doing so runs the risk of pushing inflation higher.

In a speech today, Fed Chair Jerome Powell stated the following:

“We have stressed that it will be very difficult to assess the likely economic effects of higher tariffs until there is greater certainty about the details, such as what will be tariffed, at what level and for what duration, and the extent of retaliation from our trading partners. While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The size and duration of these effects remain uncertain. While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent. Avoiding that outcome would depend on keeping longer-term inflation expectations well anchored, on the size of the effects, and on how long it takes for them to pass through fully to prices. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

One indication of expectations of future cuts in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the surprisingly large tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 6–7 meeting. As shown in the following figure, investors assign a 58.4 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

It’s a different story if we look at the end of the year. As the following figure shows, investors now expect that by the end of the FOMC’s meeting on December 9-10, the committee will have implemented at least four 0.25 percentage point (25 basis points) cuts in its target range for the federal funds rate. Investors assign a probability of 75.8 percent that the target range will end the year 3.25 percent to 3.50 percent or lower. At their March meeting, FOMC members projected only two 25 basis point cuts this year—but that was before the announcement of the unexpectedly large tariff increases.

Today (March 28), the BEA released monthly data on the personal consumption expenditures (PCE) price index as part of its “Personal Income and Outlays” report. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2016 with inflation measured as the percentage change in the PCE from the same month in the previous year. In February, PCE inflation was 2.5 percent, unchanged since January. Core PCE inflation in January was 2.8 percent, up slightly from 2.7 percent in January. Headline PCE inflation was consistent with the forecasts of economists, but core PCE inflation was higher.

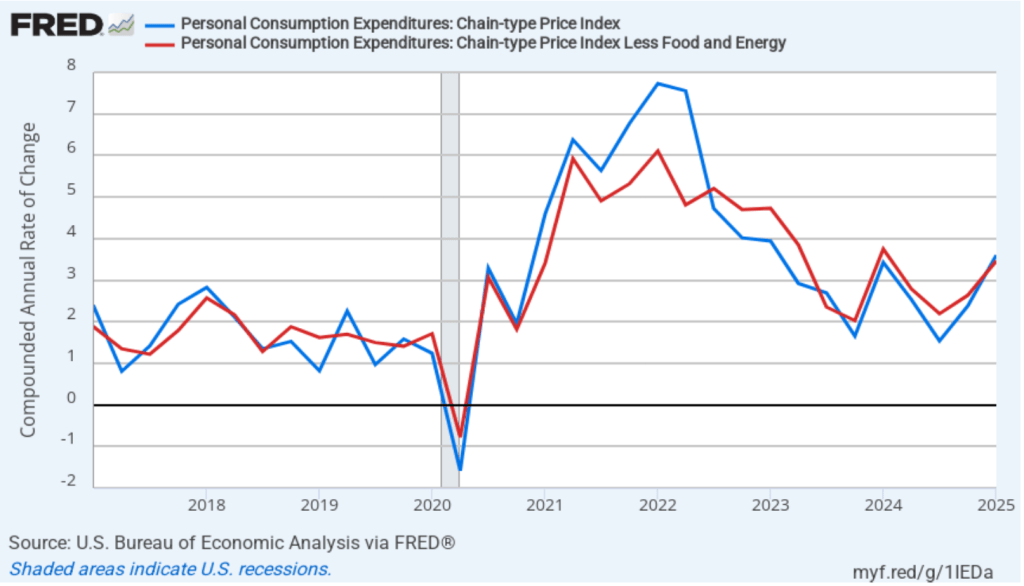

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation declined slightly in February to 4.0 percent from 4.1 percent in January. Core PCE inflation jumped in February to 4.5 percent from 3.6 percent in January. So, both 1-month PCE inflation estimates are running well above the Fed’s 2 percent target. The usual caution applies that 1-month inflation figures are volatile (as can be seen in the figure), so we shouldn’t attempt to draw wider conclusions from one month’s data. But it is definitely concerning that 1-month inflation has risen each month since November 2024.

Fed Chair Jerome Powell has noted that inflation in non-market services has been high. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the green line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

Headline market-based PCE inflation was 2.2 percent in February, and core market-based PCE inflation was 2.4 percent. So, both market-based measures show less inflation in February than do the total measures. In the following figure, we look at 1-month inflation using these measures. The 1-month inflation rates are both very high. Headline market-based inflation was 4.0 percent in February, up from 3.5 percent in January. Core market-based inflation was 4.6 percent in February, up from 2.8 percent in January. Both 1-month market-based inflation members have increased each month since November.

In summary, today’s data don’t show any evidence that inflation is returning to the Fed’s 2 percent annual target. It has to concern the Fed that the 1-month inflation measures have been increasing since November with the latest data showing inflation running far above the Fed’s target. The Fed’s goal of a “soft landing”—with inflation returning to the Fed’s 2 percent target without the economy entering a recession—no longer appears to be on the horizon. The current data seem more consistent with a “no landing” scenario in which the economy avoids a recession but inflation doesn’t return to the Fed’s target. As a result, it seems very unlikely that the Fed’s policymaking Federal Open Market Committee (FOMC) will lower its target for the federal funds rate at its next meeting on May 6-7, unless the unemployment rate jumps or the growth of output slows dramatically.

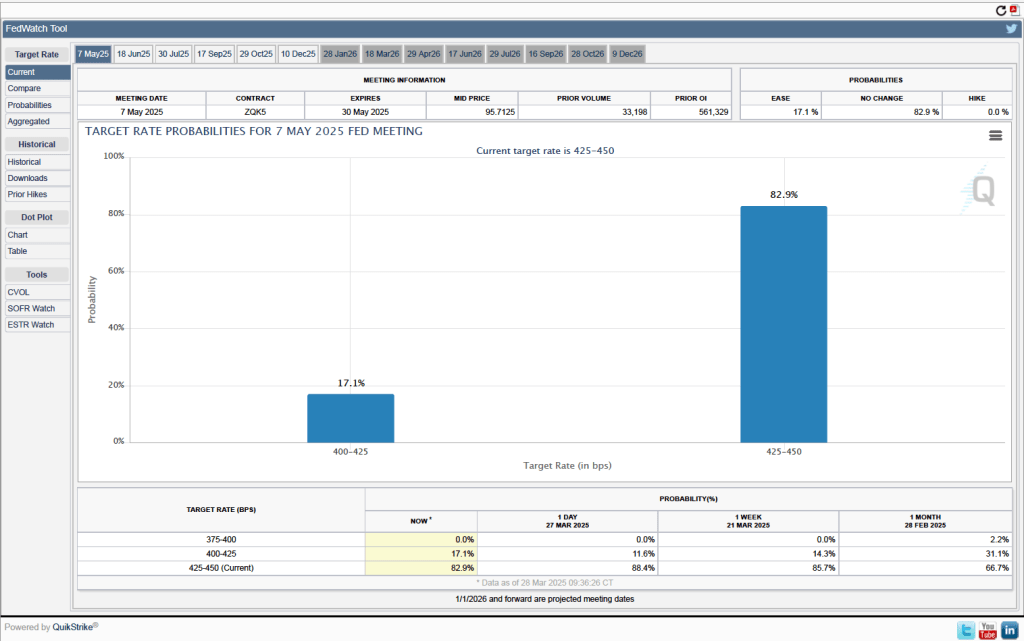

Investors who buy and sell federal funds futures contracts expect that the FOMC will leave its federal funds rate target unchanged at its next meeting. (We discuss the futures market for federal funds in this blog post.) As the following figure shows, investors assign a probability of 82.9 percent to the FOMC leaving its target for the federal funds rate unchanged at the current range of 4.25 percent to 4.50 percent. Investors assign a probability of only 17.1 percent to the FOMC cutting its target by 0.25 percentage point (25 basis points).

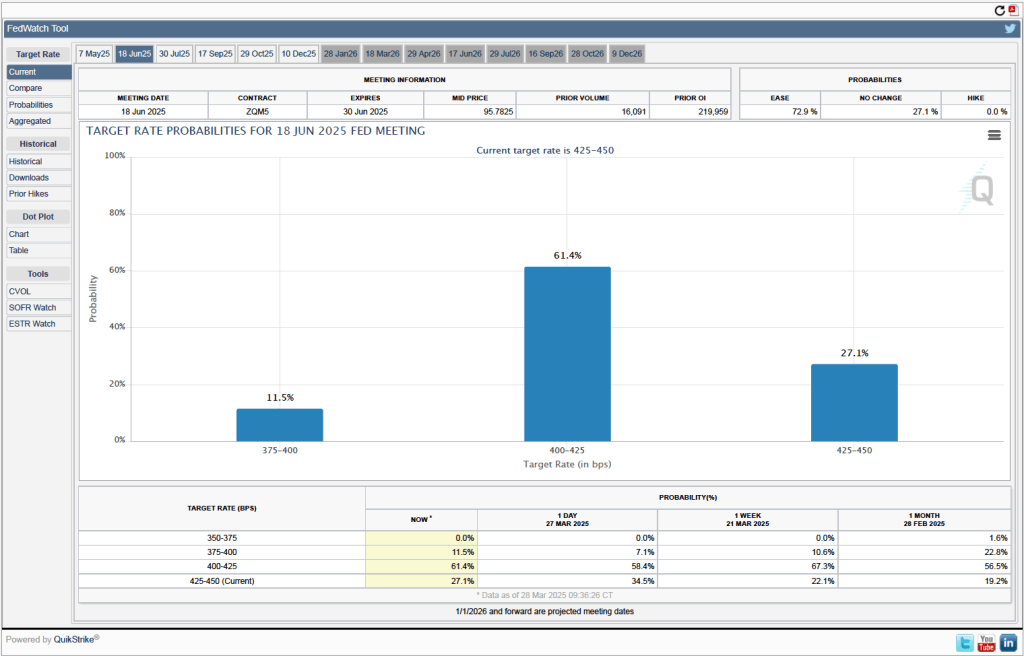

As the following figure shows, investors assign a probability of 72.9 percent percent to the FOMC cutting its target range by at least 25 basis points at its meeting on June 17–18. Despite the bad news on inflation in today’s BEA report, investors assign a zero probability to the FOMC increasing its target range for the federal funds rate to help push inflation back to the Fed’s target. One aspect of the current situation that both policymakers and investors are uncertain of is the effect of the Trump Administration’s new tariffs on the price level. It’s possible that some of the increase in inflation seen in today’s report is the result of tariff increases, but the full extent of the effect will only become evident when the tariffs are fully in place.

Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

As they had before their previous meeting, members of the Fed’s Federal Open Market Committee (FOMC) had signaled that the committee was likely to leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent at its meeting today (March 19). In a press conference following the meeting, Fed Chair Jerome Powell noted that the FOMC was facing significant policy uncertainty:

“Looking ahead, the new Administration is in the process of implementing significant policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation…. While there have been recent developments in some of these areas, especially trade policy, uncertainty around the changes and their effects on the economic outlook is high…. We do not need to be in a hurry to adjust our policy stance, and we are well positioned to wait for greater clarity.”

The next scheduled meeting of the FOMC is May 6–7. It seems likely that the committee will also keep its target rate constant at that meeting. Although at his press conference, Powell noted that “Policy is not on a preset course. As the economy evolves, we will adjust our policy stance in a manner that best promotes our maximum employment and price stability goals.” The statement the committee released after the meeting showed that the decision to leave the target rate unchanged was unanimous.

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed is successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

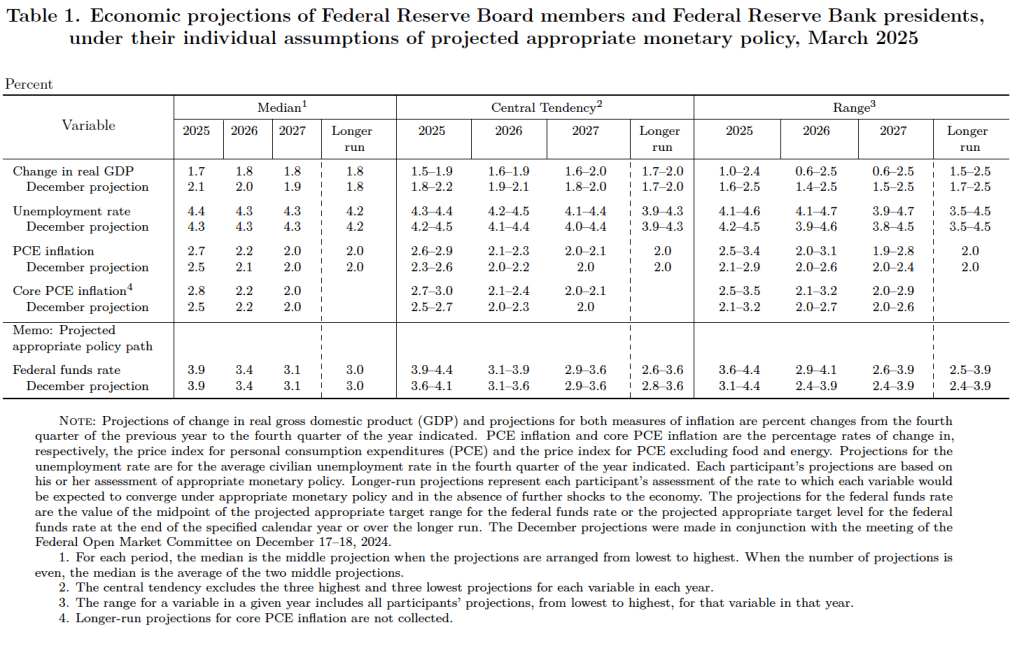

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does after its March, June, September, and December meetings. The SEP presents median values of the 18 committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

There are several aspects of these forecasts worth noting:

Committee members reduced their forecast of real GDP growth for 2025 from 2.1 percent in December to 1.7 percent today. Committee members also slightly increased their forecast of the unemployment rate at the end of 2025 from 4.3 percent to 4.4 percent. (The unemployment rate in February was 4.1 percent.)

Committee members now forecast that personal consumption expenditures (PCE) price inflation will be 2.7 percent at the end of 2025. In December, they had forecast that it would 2.5 percent. Similarly, their forecast of core PCE inflation increased from 2.5 percent to 2.8 percent. The committee does not expect that PCE inflation will decline to the Fed’s 2 percent annual target until 2027.

The committee’s forecast of the federal funds rate at the end of 2025 was unchanged at 3.9 percent. The federal funds rate today is 4.33 percent, which indicates that committee members expect to make two 0.25 percentage point (25 basis points) cuts in their target for the federal funds rate this year. Investors are similarly forecasting two 25 basis point cuts.

During his press conference, Powell indicated that a significant part of the increase in goods inflation during the first two months of the year was likely due to tariffs, although the Fed’s staff was unable to make a precise estimate of how much. Economists generally believe that tariffs cause one-time increases in the price level, rather than persistent inflation. Powell was asked during the press conference whether the FOMC was likely to “look through”—that is, not respond—to the tariffs. Powell replied that it was too early to make that decision, but that: “If there’s an inflation that’s going to go away on its own, it’s not the correct response to tighten policy.”

Powell noted that although surveys show that businesses and consumers expect an increase in inflation, over the long run, expectations are that the inflation rate will return to the Fed’s 2 percent annual target. In that sense, Powell said that expectations of inflation remain “well anchored.”

Barring a sharp slowdown in the growth of real GDP, a significant rise in the unemployment rate, or a significant rise in the inflation rate, the FOMC seems likely to leave its target for the federal funds rate unchanged over the next few months.

Today (March 12), the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). The following figure compares headline inflation (the blue line) and core inflation (the green line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.8 percent in February—down from 3.0 percent in January.

The core inflation rate,which excludes the prices of food and energy, was 3.1 percent in February—down from 3.3 percent in January.

Both headline inflation and core inflation were slightly below what economists surveyed had expected.

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) fell sharply from 5.7 percent in February to 2.6 percent in January. Core inflation (the green line) decreased from 5.5 percent in January to 2.8 percent in January.

Overall, considering 1-month and 12-month inflation together, the most favorable news is the sharp decline in both the headline and the core 1-month inflation rats. But inflation is still running ahead of the Fed’s 2 percent annual inflation target.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that 1-month inflation is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

There’s been considerable discussion in the media about continuing inflation in grocery prices. In the following figure the blue line shows inflation in the CPI category “food at home,” which is primarily grocery prices. Inflation in grocery prices was 1.8 percent in February and has been below 2 percent every month since November 2023. Although on average grocery price inflation has been low, there have been substantial increases in the prices of some food items. For instance, egg prices—shown by the green line—increased by 96.8 percent in February. But, as the figure shows, egg prices are usually quite volatile month-to-month, even when the country is not dealing with an epidemic of bird flu.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.1 percent in February, unchanged from January. Twelve-month median inflation (the green line) declined slightly from 3.6 percent in January to 3.5 percent in February.

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation fell from 5.1 percent in January to 3.3. percent in February. One-month median inflation from 3.9 percent in January to 3.5 percent in February. These data provide confirmation that (1) CPI inflation at this point is likely running higher than a rate that would be consistent with the Fed achieving its inflation target, and (2) inflation slowed somewhat from January to February.

What are the implications of this CPI report for the actions the FOMC may take at its next several meetings? The major stock market indexes rose sharply at the beginning of trading this morning, but then swung back and forth between losses and gains. Inflation being lower than expected may have increased the probability that the FOMC will cut its target for the federal funds rate sooner rather than later. Lower inflation and lower interest rates would be good news for stock prices. But investors still appear to be worried about the extent to which a trade war might both slow economic growth and increase the price level.

Investors who buy and sell federal funds futures contracts still do not expect that the FOMC will cut its target for the federal funds rate at its next two meetings. (We discuss the futures market for federal funds in this blog post.) Today, investors assigned only a 1 percent probability that the Fed’s policymaking Federal Open Market Committee (FOMC) will cut its target from the current 4.25 percent to 4.50 percent range at its meeting next week. Investors assigned a probability of 33.3 percent that the FOMC would cut its target after its meeting on May 6–7. Investors today assigned a probability of 78.6 percent that the committee will cut its target after its meeting on June 17–18. That probability has fallen slightly over the past week.

At his press conference after next Wednesday’s FOMC meeting, Fed Chair Jerome Powell will give his thoughts on the current economic situation.