Welcome to the first podcast for the Fall 2024 semester from the Hubbard/O’Brien Economics author team. Check back for Blog updates & future podcasts which will happen every few weeks throughout the semester.

Join authors Glenn Hubbard & Tony O’Brien as they provide an update on the Macroeconomy. They offer thoughts on the likelihood of a soft landing and whether the actions of the Federal Reserve helped or hindered that process. The monetary and fiscal challenges facing the new administration are real and the Fed will begin its process of rate-cutting this week in the upcoming FOMC meeting. Gain insight into this evolving situation by listening to this podcast. Click HERE to access the podcast.

Today (September 11), the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). This report is the last one that will be released before the Fed’s policy-making Federal Open Market Committee (FOMC) holds its next meeting on September 17-18.

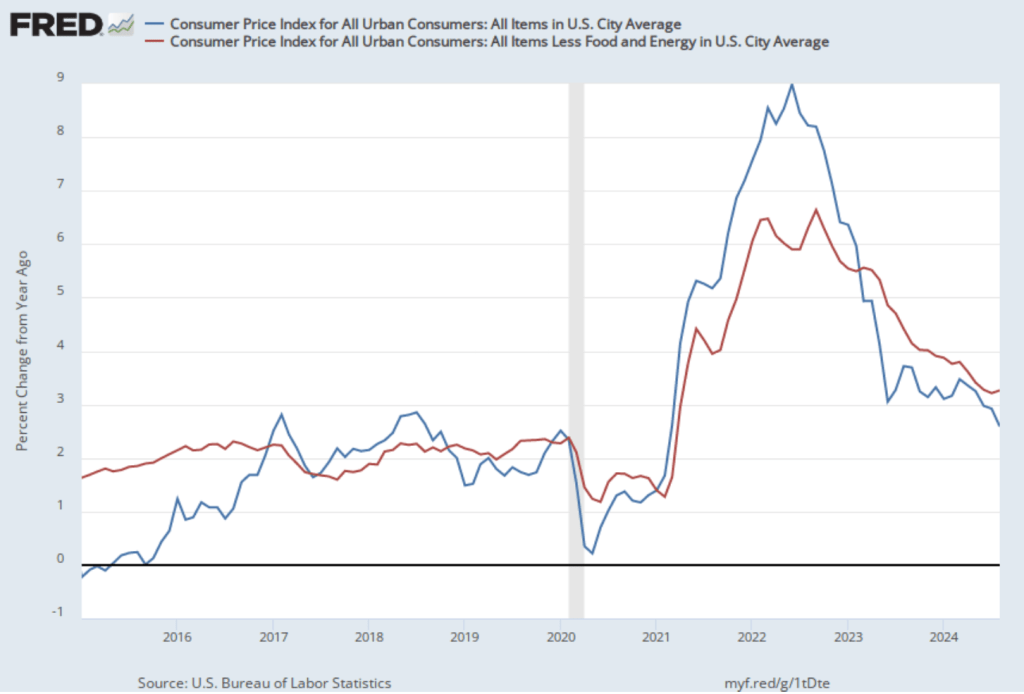

As the following figure shows, the inflation rate for August measured by the percentage change in the CPI from the same month in the previous month—headline inflation (the blue line)—was 2.6 percent down from 2.9 percent in July. Core inflation (the red line)—which excludes the prices of food and energy—increased slightly to 3.3 percent in August from 3.2 percent in July. Headline inflation was slightly below what economists surveyed by the Wall Street Journal had expected, while core inflation was slightly higher.

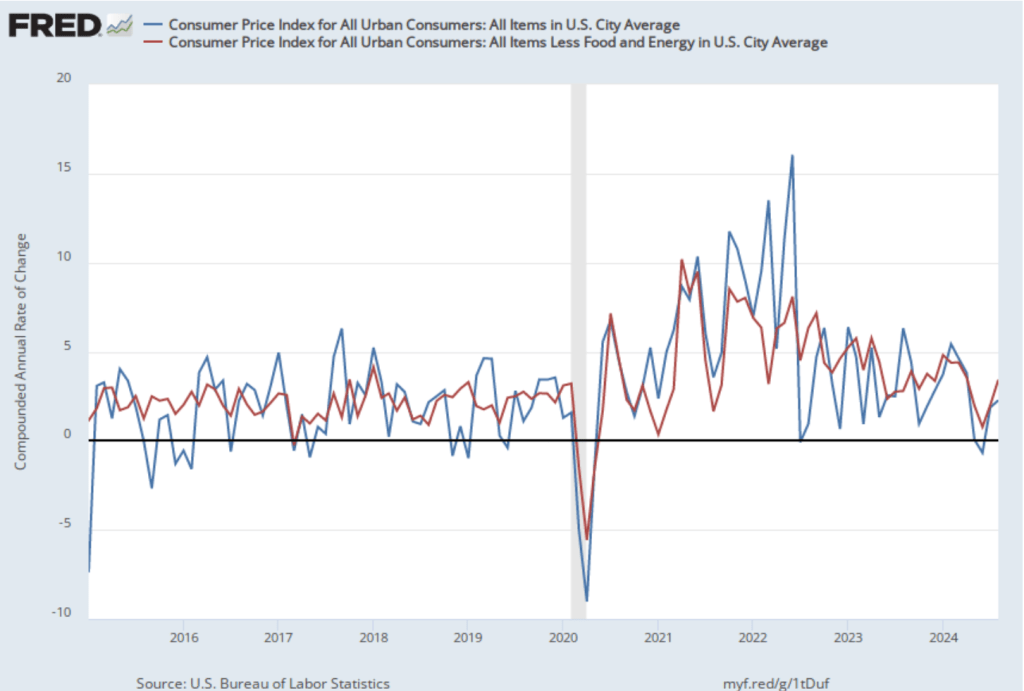

As the following figure shows, if we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—we see that both headline and core inflation increased. Headline inflation (the blue line) increased from 1.8 percent in July to 2.3 percent in August. Core inflation (the red line) jumped from 2.0 percent in July to 3.4 percent in August. Overall, we can say that, taking 1-month and 12 month inflation together, the U.S. economy may still be on course for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession—but the increase in 1-month inflation is concerning. Of course, as always, it’s important not to overinterpret the data from a single month. (Note, also, that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target.)

As we’ve discussed in previous blog posts, Federal Reserve Chair Jerome Powell and his colleagues on the FOMC have been closely following inflation in the price of shelter. The price of “shelter” in the CPI, as explained here, includes both rent paid for an apartment or house and “owners’ equivalent rent of residences (OER),” which is an estimate of what a house (or apartment) would rent for if the owner were renting it out. OER is included to account for the value of the services an owner receives from living in an apartment or house.

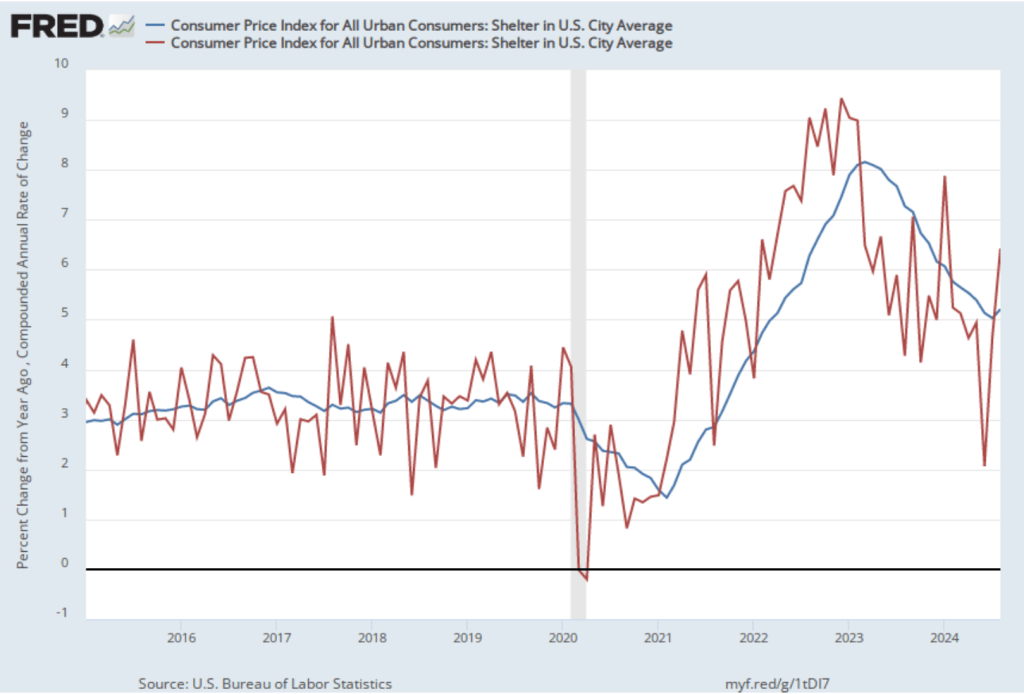

As the following figure shows, inflation in the price of shelter has been a significant contributor to headline inflation. The blue line shows 12-month inflation in shelter and the red line shows 1-month inflation in shelter. Twelve-month inflation in shelter reversed the decline that began in the spring of 2023, rising from 5.0 percent in July to 5.2 percent August. One-month inflation in shelter—which is much more volatile than 12-month inflation in shelter—increased from 4.6 percent in July to 5.2 percent in August, continuing an increase that began in June. The increase in 1-month inflation in shelter may concern the members of the FOMC, as may, to a lesser extent, the increase in 12-month inflation in shelter. Shelter has a smaller weight of 15 percent in the PCE price index that the Fed uses to gauge whether it is hitting its 2 percent inflation target in contrast with the 33 percent weight that shelter has in the CPI. But persistent shelter inflation in the 5 percent range would make a soft landing more difficult.

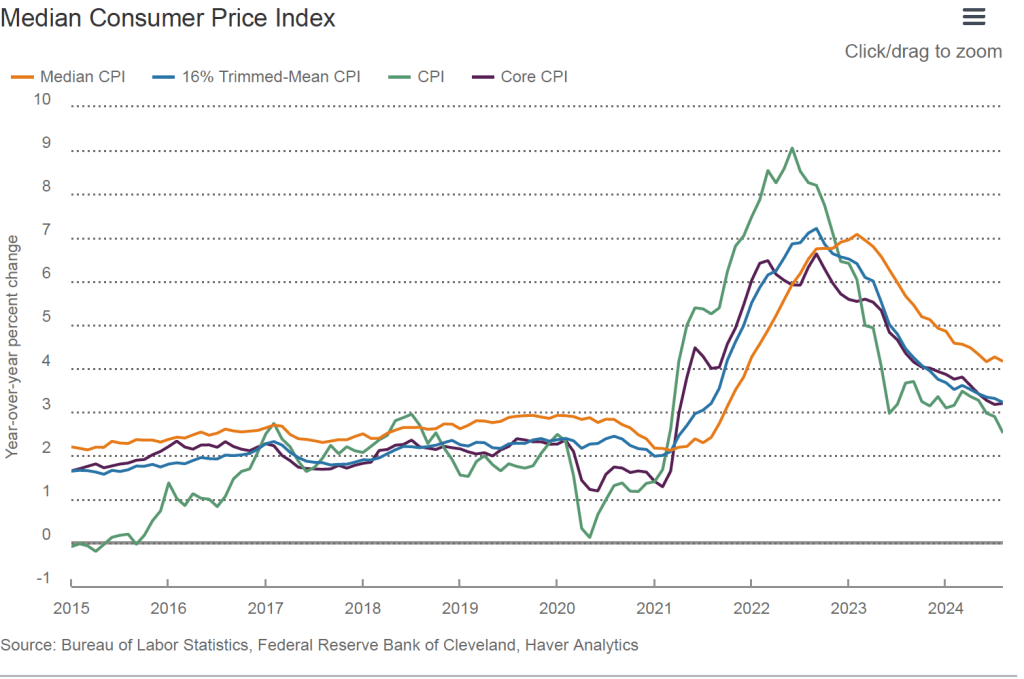

Finally, in order to get a better estimate of the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation. Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. Trimmed mean inflation drops the 8 percent of good and services with the higherst inflation rates and the 8 percent of goods and services with the lowest inflation rates.

As the following figure (from the Federal Reserve Bank of Cleveland) shows, median inflation (the orange line) declined slightly from 4.3 percent in July to 4.2 percent in August. Trimmed mean inflation (the blue line) also declined slightly from 3.3 in July to 3.2 percent in August. These data provide confirmation that core CPI inflation is likely running higher than a rate that would be consistent with the Fed achieving its inflation target.

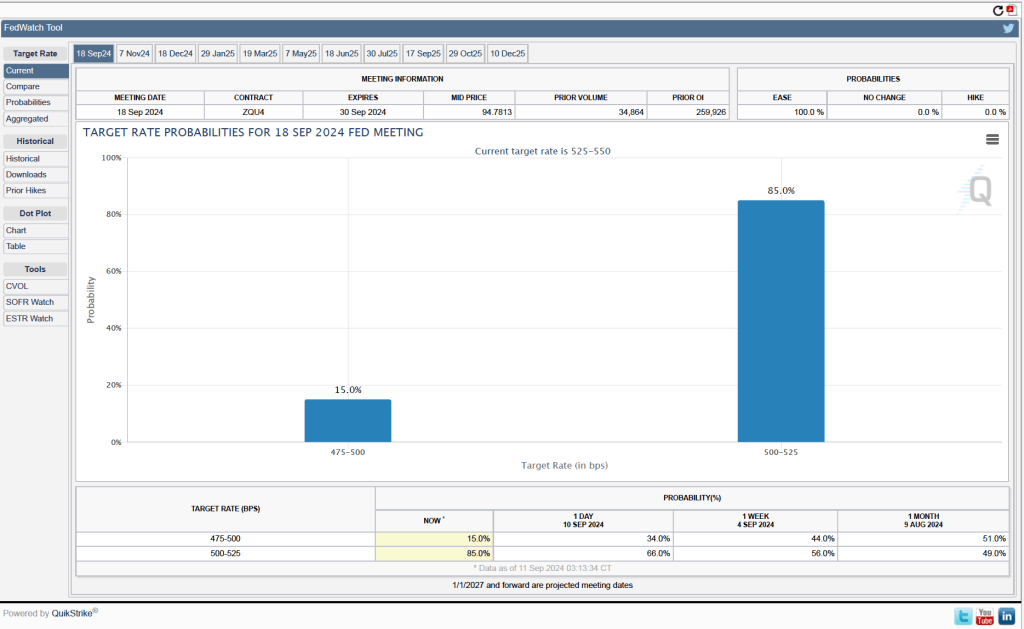

For the past few weeks Fed officials have been indicating that the FOMC is likely to cut its target for the federal funds at its next meeting on Septembe 17-18. Investors who buy and sell federal funds futures contracts expect that the FOMC will cut its target for the federal funds rate by 0.25 percentage point from the current range of 5.50 percent to 5.25 percent. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 85.0 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point at its next meeting and a probability of only 15.0 percent that the cut will be 0.50 percentage point.

The FOMC has to balance the risk of leaving its target for the federal funds rate at its current level for too long—increasing the risk of slowing demand so much that the economy slips into recession—against the risk of cutting its target too soon—increasing the risk that inflation persists above the Fed’s 2 percent target. We’ll see at the committee’s next meeting how Fed Chair Jerome Powell and the other members assess the current state of the economy as they consider when and by how much to cut their target for the federal funds rate.

The “Employment Situation” report (often referred to as the “jobs report”), which is released monthly by the Bureau of Labor Statistics (BLS), is always closely followed by economists and policymakers because it provides important insight in the current state of the U.S. economy. This month’s report is considered particularly important because last month’s report indicated that the labor market might be weaker than most economists had believed. As we discussed in a recent blog post, late last month Fed Chair Jerome Powell signaled that the Fed’s policy-making Federal Open Market Committee (FOMC) was likely to cut its target for the federal funds rate at its next meeting on September 17-18.

Economists and investment analysts had speculated that following August’s unexpectedly weak jobs report, another weak report might lead the FOMC to cut its federal funds target by 0.50 percentage rate rather than by the more typical 0.25 percent point. The jobs report the BLS released this morning (September 6) was mixed, showing a somewhat lower than expected increase in employment as measured by the establishment survey, but higher wage growth.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and policymakers at the Federal Reserve believe that employment data from the establishment survey provides a more accurate indicator of the state of the labor market than do either the employment data or the unemployment data from the household survey. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

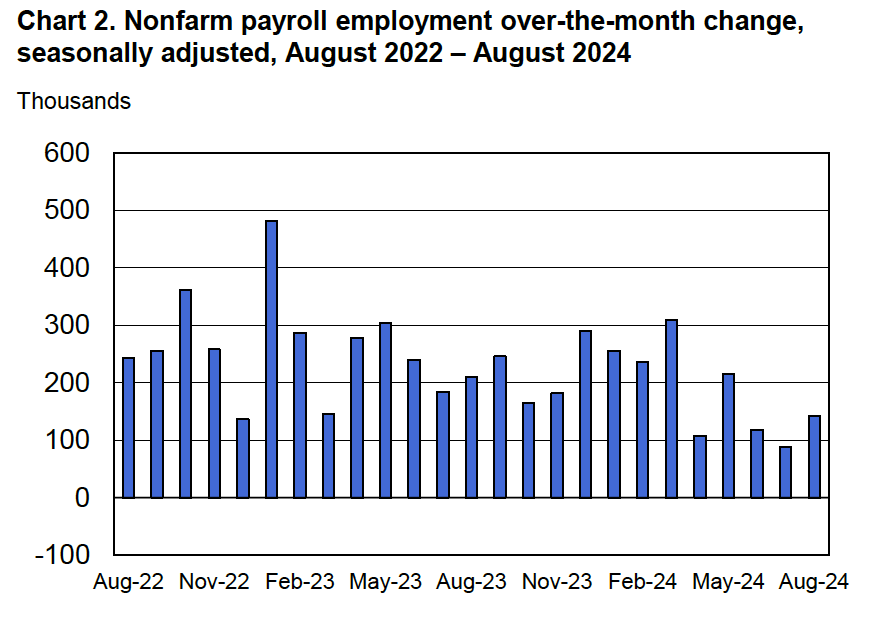

According to the establishment survey, there was a net increase of 142,000 jobs during August. This increase was below the increase of 161,000 that economists had forecast in a survey by the Wall Street Journal. The following figure, taken from the BLS report, shows the monthly net changes in employment for each month during the past two years. The BLS revised lower its estimates of the net increase in jobs during June and July by a total of 86,000. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”)

The BLS’s estimate of average monthly job growth during the last three months is now 116,000, a significant decline from an average of 211,000 per month during the previous three months and 251,000 per month during 2023.

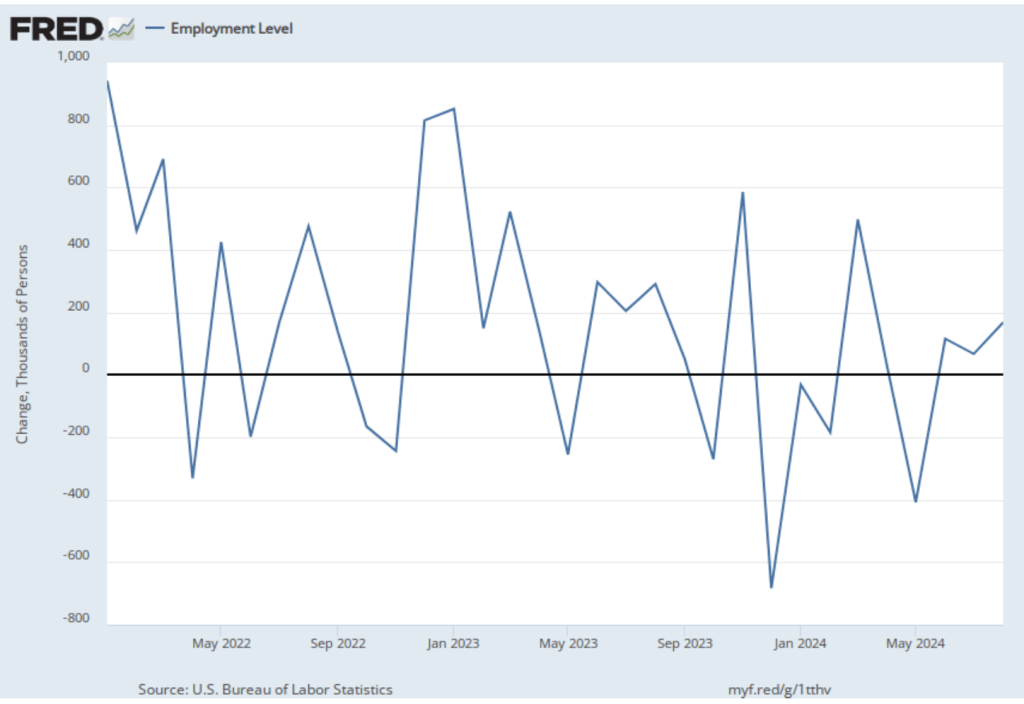

As the following figure shows, the net change in jobs from the household survey moves much more erratically than does the net change in jobs in the establishment survey. The net change in jobs as measured by the household survey increased from 67,000 in July to 168,000 in August. So, in this case the direction of change in the two surveys was the same—an increase in the net number of jobs created in August compared with July.

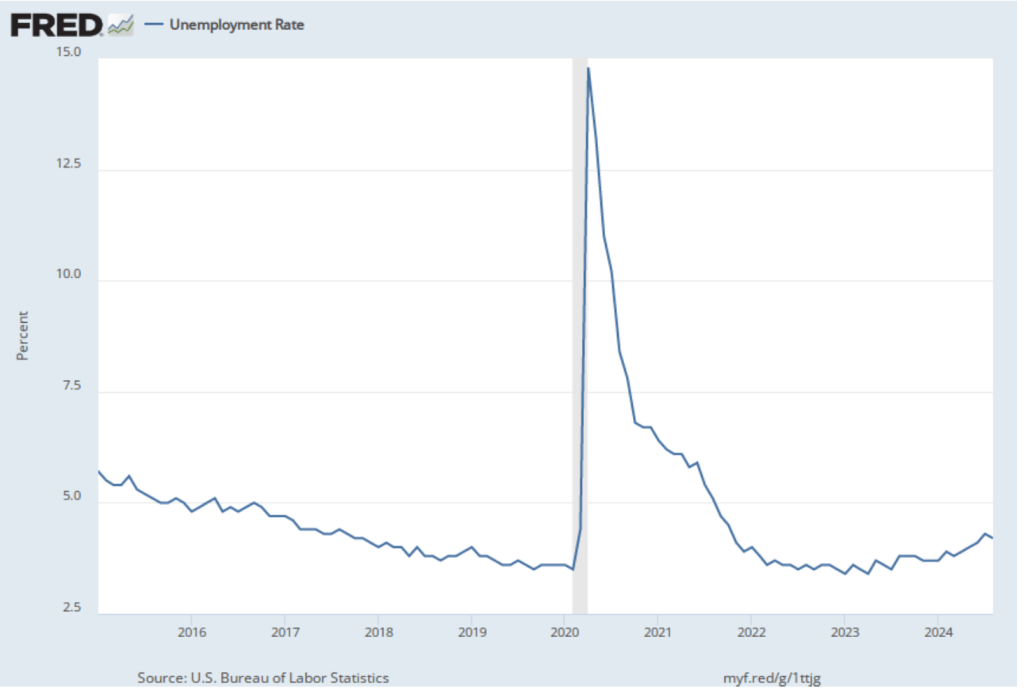

As the following figure shows, the unemployment rate, which is also reported in the household survey, decreased from 4.3 percent to 4.2 percent—breaking what had been a five month string of unemployment rate increases.

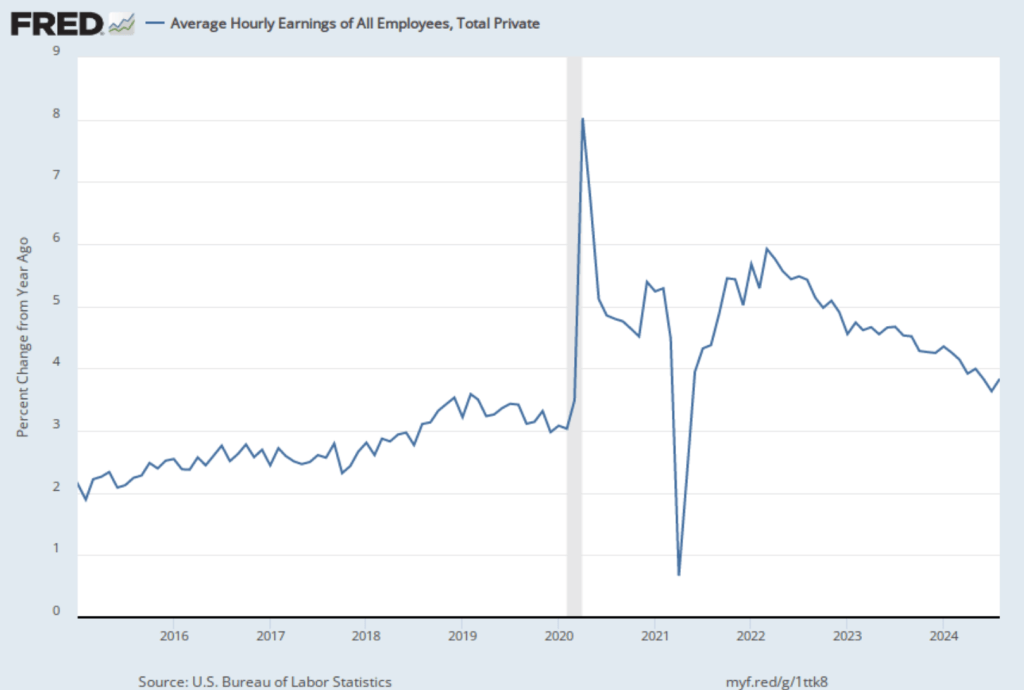

The establishment survey also includes data on average hourly earnings (AHE). As we note in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage that it is available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. AHE increased 3.8 percent in August, up from a 3.6 percent increase in July.

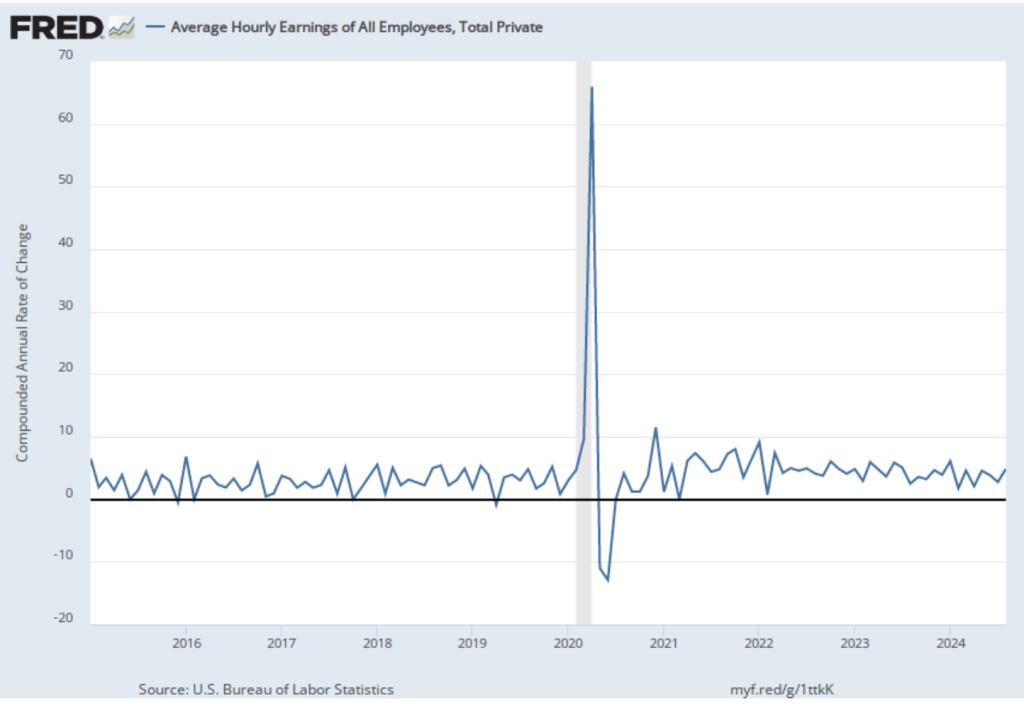

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic.

The 1-month rate of wage inflation of 4.9 percent in August is a significant increase from the 2.8 percent rate in July, although it’s unclear whether the increase represented renewed upward wage pressure in the labor market or reflected the greater volatility in wage inflation when calculated this way.

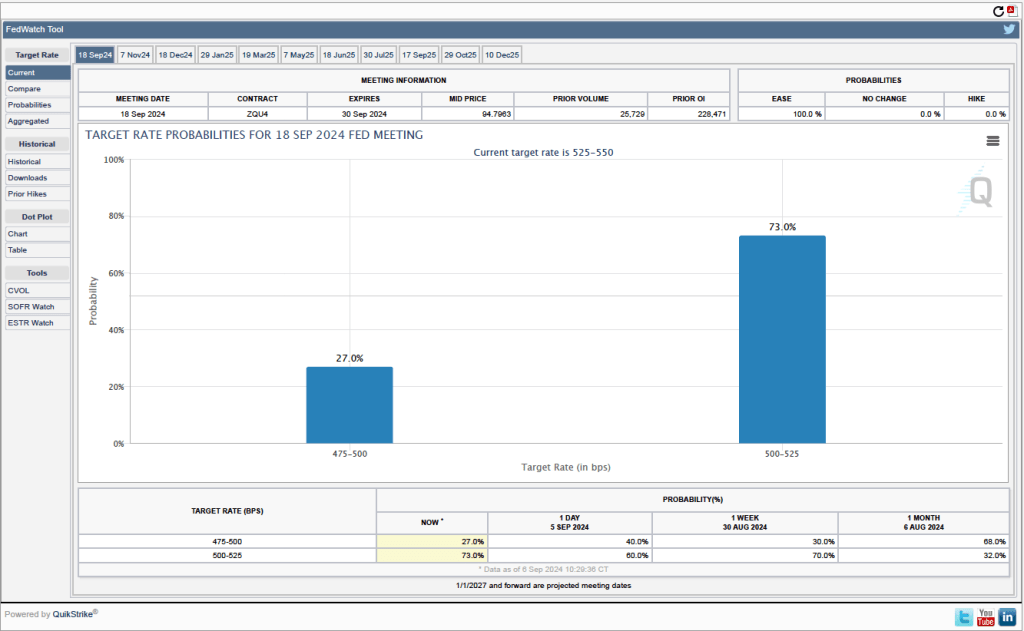

What effect is this jobs report likely to have on the FOMC’s actions at its September meeting? One indication comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 73.0 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point at its next meeting and a probability of only 27.0 percent that the cut will be 0.50 percentage point. In contrast, after the last jobs report was interpreted to indicate a dramatic slowing of the economy, investors assigned a probability of 79.5 percent to a 0.50 cut in the federal funds rate target.

It seems most likely following today’s mixed job report that the FOMC will cut its target for the federal funds rate by 0.25 percent point from the current target range of 5.25 percent to 5.50 percent to a range of 5.00 percent to 5.25 percent. The report doesn’t indicate the significant weakening in the labor market that was probably needed to push the committee to cutting its target by 0.50 percent point.

Image generated by GTP-4o “illustrating the concept of federal economic statistics.”

Government economic statistics help guide the actions of policymakers, firms, households, workers, and investors. As a recent report from the American Statistical Association expressed it:

“Official statistics from the federal government are a critically important source of needed information in the United States for policymakers and the public, providing information that meets the highest professional standards of relevance, accuracy, timeliness, credibility, and objectivity.”

Government agencies consider some of these statistics to be of particular importance. The Office of Management and Budget (OMB) has designated 36 data series as being principal federal economic indicators (PFEIs). Many of these are key macroeconomic data series, such as the consumer price index (CPI), gross domestic product (GDP), and unemployment. Others, such as housing vacancies and natural gas storage, are less familiar although important in assessing conditions in specific sectors of the economy.

Since 1985, the preparation and release of PFEIs has been governed by OMB Statistical Policy Directive No. 3. Among other things, Directive No. 3 is intended to ‘‘preserve the distinction between the policy-neutral release of data by statistical agencies and their interpretation by policy officials.’’ Although some politicians and commentators claim otherwise, federal government statistical agencies, such as the Bureau of Labor Statistics (BLS) and the Bureau of Economic Analysis (BEA), are largely staffed by career government employees whose sole objective is to gather and release the most accurate data possible with the funds that Congress allocates to them.

Directive No. 3 also requires the statistical agencies to act so as to ‘‘prevent early access to information that may affect financial and commodity markets.’’ Unfortunately, several times recently the BLS has been subject to criticism for releasing data early or releasing data to financial firms before the official public release of the data. For instance, on August 21, 2o24 the BLS was scheduled to release at 10:00 a.m. its annual benchmark revision of employment estimates from the establishment survey. (We discuss this release in this blog post.) Because of technical problems, the public release was delayed until 10:30. During that half hour, analysts at some financial firms called the BLS and were given the data over the phone. Doing so was contraty to Directive No. 3 because the employment data are a PFEI, which obliges the BLS to take special care that the data aren’t made available to anyone before their public release.

The New York Times filed a Freedom of Information Act (FOIA) request with the BLS in order to investigate the cause of several instances of the agency releasing data early. In an article summarizing the information the paper received as a result of its FOIA request, the reporters concluded that “the information [the BLS] has provided [about the reasons for the early data releases] has at times proved inaccurate or incomplete.” The BLS has pledged to take steps to ensure that in the future it will comply fully with Directive No. 3.

In a report discussing the difficulties federal agencies statistical have in meeting their obligations responsibilities, the American Statistical Association singled out two problems: the declining reponse rate to surveys—particularly notable with respect to the establishment employment survey—and tight budget constraints, which are hampering the ability of some agencies to hire the staff and to obtain the other resources necessary to collect and report data in an accurate and timely manner.

Image generated by GTP-4o of “an apartment building in Amersterdam.”

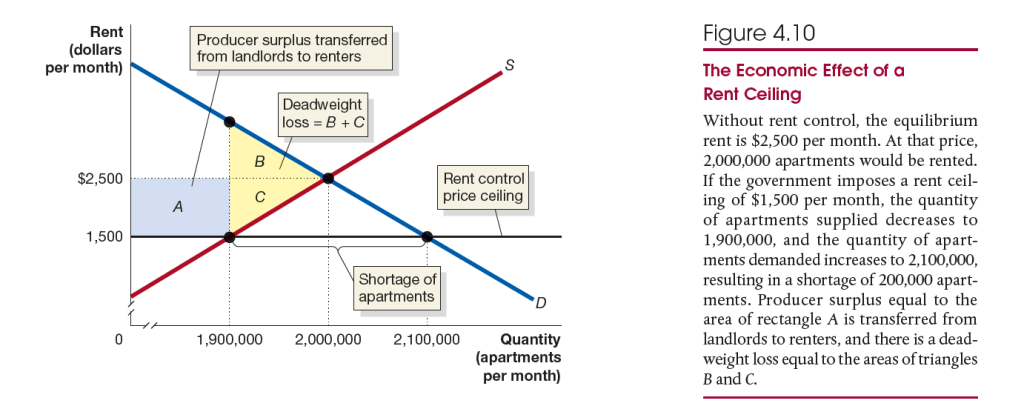

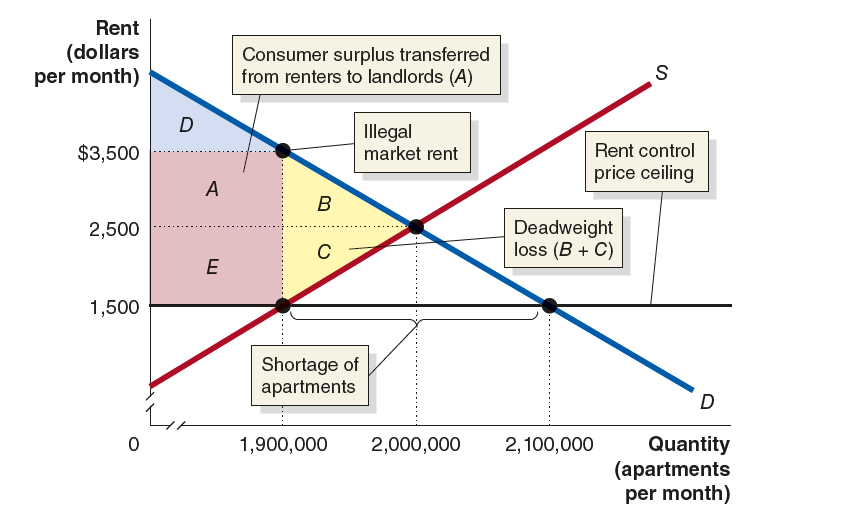

Recent articles in the media discussed the effects of rent control on the market for apartments in the Netherlands and in Stockholm, the capital of Sweden. The articles describe a situation that is consistent with the analysis in Chapter 4, Section 4.3. Figure 4.10 shows the expected results from the imposition of a rent control law. Some renters gain by living in apartments at below the equilibirum market rent, but the shortage of apartments resulting from the price ceiling means that some renters are unable to find apartments. As with other price controls, rent ceilings impose a deadweight loss on the economy, shown in the figure as the areas B + C.

An article on bloomberg.com discusses the effect on the market for apartments in the Netherlands of the passage in June of the Affordable Rent Act. The act raised the fraction of apartments covered by rent control from about 80 percent to 96 percent. The expansion of rent control appears to have led to an increased shortage of apartments. The article quotes one teacher who has been unable to find an apartment for her family as saying: “The cost isn’t the problem, but a real shortage of housing is.”

The article indicates that some landlords who doubt they can earn a profit under the new law are selling their buildings. If the buildings are converted to other uses, the shortage of apartments will be increased. The article mentions another unintended change to the apartment market from the provision of the new law that requires leases to be open-ended. Some landlords fear that as a result they may find themselves unable to evict tenants, however troublesome the tenants may be. In response, these landlords are giving priority to foreigners, who they believe are likely to move more often.

An article in the Economist looks at another aspect of rent control. The following figure is reproduced from Solved Problem 4.3. It shows that because rent control leads to a shortage of apartments it creates an incentive for tenants and landlords to agree to a rent that is higher than the legal rent ceiling. In this example, renters who are unable to find an apartment at the rent control ceiling of $1,500 may bid up the rent to $3,500—which in this example is $1,000 higher than the market equilibrium rent in the absence of rent control—rather than not be able to rent an apartment. Clearly, renters paying this illegal rent are worse off than they would be if there were no rent control law.

According to the article in the Economist, the average time on a waiting list for a rent controlled apartment is 20 years. Not surprisingly, “Young Swedes often have to put up with expensive sublets agreed to under the table,” for which they typically pay rents above both the rent control ceiling and the market equilibrium rent. Most economists agree that expanding the quantity of available housing by making it easier to build homes and apartments is a better way of reducing housing costs than is imposing rent controls.

President Lyndon Johnson signing the Economic Opportunity Act in 1964. (Photo from Wikipedia)

In 1964, President Lyndon Johnson announced that the federal government would launch a “War on Povery.” In 1988, President Ronald Regan remarked that “some years ago, the Federal Government declared war on poverty, and poverty won.” Regan was exaggerating because, however you measure poverty, it has declined substantially since 1964, although the official poverty rate has remained stubbornly high since the early 1970s.

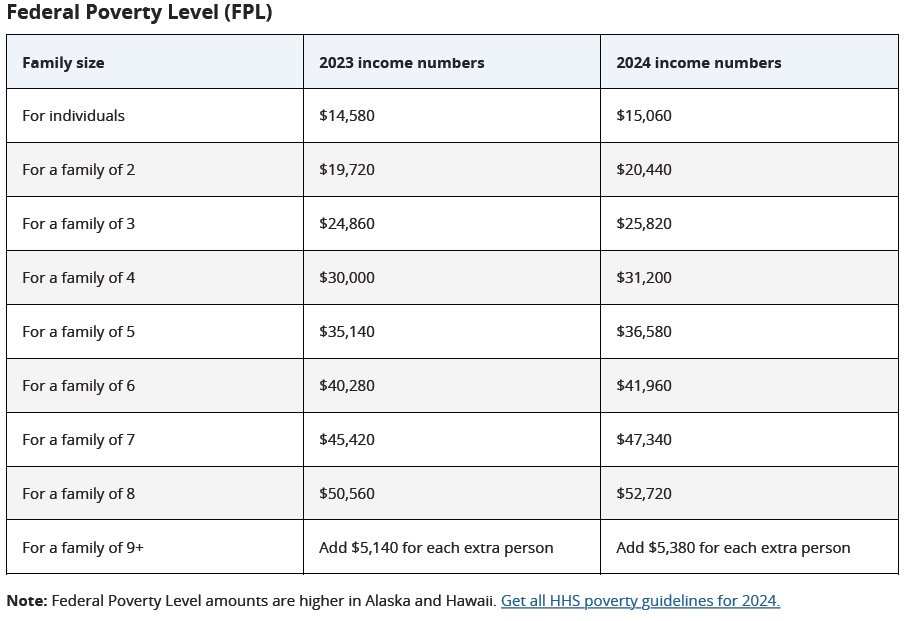

Each year the U.S. Census Bureau calculates the official poverty rate—the fraction of the population with incomes below the federal poverty level, often called the poverty line. The following table shows the poverty line for the years 2023 and 2024 illustrating how it varies with the size of a household:

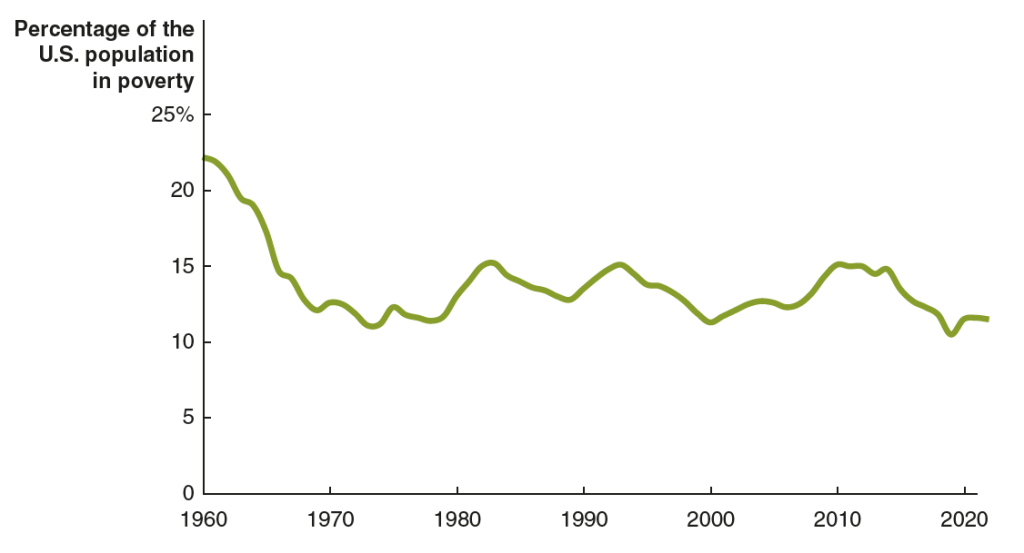

The following figure shows the official poverty rate for the years from 1960 to 2022. The poverty rate in 1960 was 22.2 percent. By 1973, it had been cut in half to 11.1 percent. The decline in the poverty rate largely stopped at that point. In the following years the official poverty rate fluctuated but stopped trending down. In 2022, the poverty rate was 11.5 percent—actually higher than in 1973. (The Census Bureau will release the poverty rate for 2023 later this month.)

But is the official poverty rate the best way to measure poverty? In Microeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), we discuss some of the issues involved in measuring poverty. One key issue is how income should be measured for purposes of calculating the poverty rate. In an academic paper, Richard Burkhauser, of the University of Texas, Kevin Corinth, of the American Enterprise Institute, James Elwell, of the Congressional Joint Committee on Taxastion, and Jeff Larimore, of the Federal Reserve Board, carefully consider this issue. (The paper can be found here, although you may need a subscription or access through your library.)

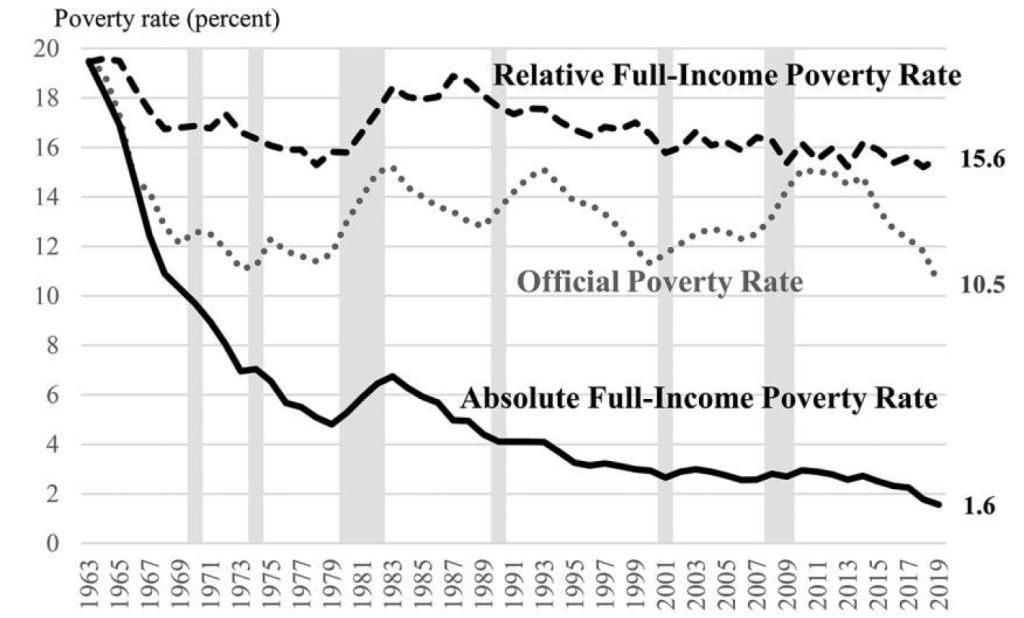

They find that using an adjusted measure of the poverty line and a fuller measure of income results in the poverty rate falling from 19.5 percent in 1963 to 1.9 percent in 2019. In other words, rather than the poverty rate stagnating at around 11 percent—as indicated using the official poverty numbers—it actually fell dramatically. Rather than progress in the War on Poverty having stopped in the early 1970s, these results indicate that the war has largely been won. The authors, though, provide some important qualifications to this conclusion, including the fact that even 1.9 percent of the population represents millions of people.

Discussions of poverty distinguish between absolute poverty—the ability of a person or family to buy essential goods and services—and relative poverty—the ability to buy goods and services similar to those that can be purchased by individuals and families with the median income. The authors of this study argue that in launching the War on Povery, President Johnson intended to combat absolute poverty. Therefore, the authors start with the poverty line as it was in 1963 and increase the line each year by the rate of inflation, as measured by changes in the personal consumption expenditures (PCE) price index.

To calculate what they call “the absolute full-income poverty measure (FPM)” they include in income both cash income and “in-kind programs designed to fight poverty, including food stamps (now the Supplemental Nutrition Assistance Program [SNAP]), the schoollunch program, housing assistance, and health insurance.” As noted earlier, using this new definition, the overall poverty rate declined from 19.5 percent in 1963 to 1.9 percent in 2019. The Black poverty rate declined from 50.8 percent in 1963 to 2.9 percent in 2019.

The author’s find that the War on Poverty has been less successful in reducing relative poverty. Linking increases in the poverty line to increases in median income results in the poverty rate having decreased only from 19.5 percent in 1963 to 15.6 percent in 2019. The authors also note that not as much progress has been made in fulfilling President Johnson’s intention that: “The War on Poverty is not a struggle simply to support people, to make them dependent on the generosity of others.” They find that the fraction of working-age people who receive less than half their income from working has increased from 4.7 percent in 1967 to 11.0 percent in 2019.

The following figure from the authors’ paper shows the offical poverty rate, the absolute full-income poverty rate—which the authors believe does the best job of representing President Johnson’s intentions when he launched the War on Poverty—and the relative poverty rate.

Because of disagreements on how to define poverty and because of the difficulty of constructing comprehensive measures of income—difficulties that the authors discuss at length in the paper—this paper won’t be the last word in assessing the results of the War on Poverty. But the paper provides an important new discussion of the issues involved in measuring poverty.

The result when asking GTP-4o to generate “an image illustrating inflation.”

Inflation, as measured by changes in the personal consumption expenditures (PCE) price index, continued a slow decline that began in March. (The Fed uses annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target.) On August 30, the Bureau of Economic Analysis (BEA) released its “Personal Income and Outlays” report for July, which contains monthly PCE data.

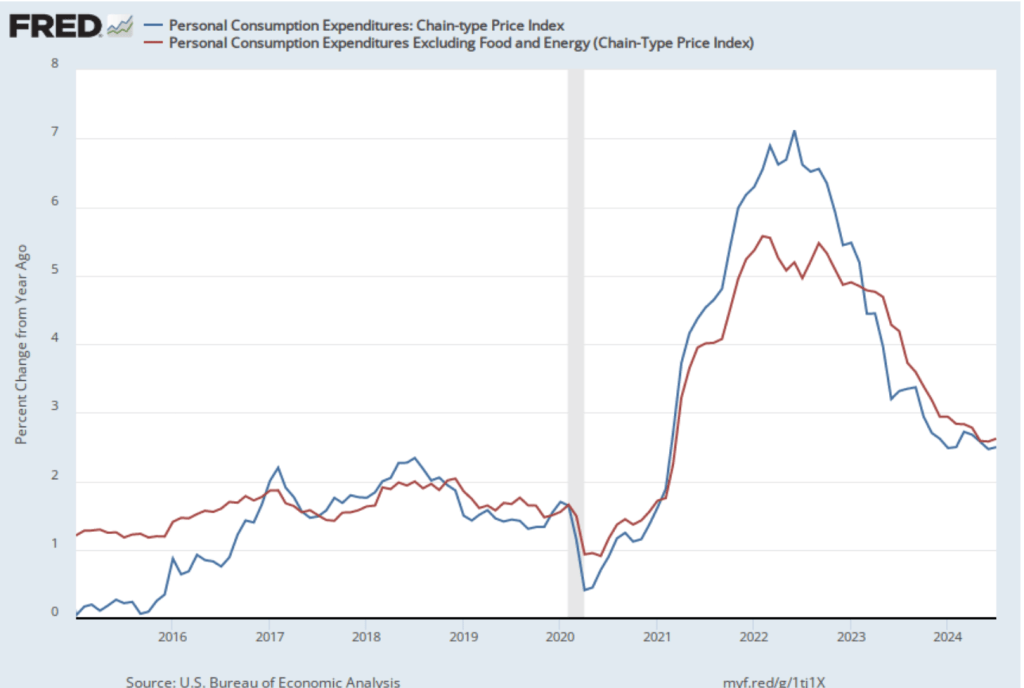

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2015 with inflation measured as the percentage change in the PCE from the same month in the previous year. Measured this way, in July PCE inflation (the blue line) was 2.5 percent, the same as in June. Core PCE inflation (the red line) in July was 2.6 percent, which was also unchanged from June.

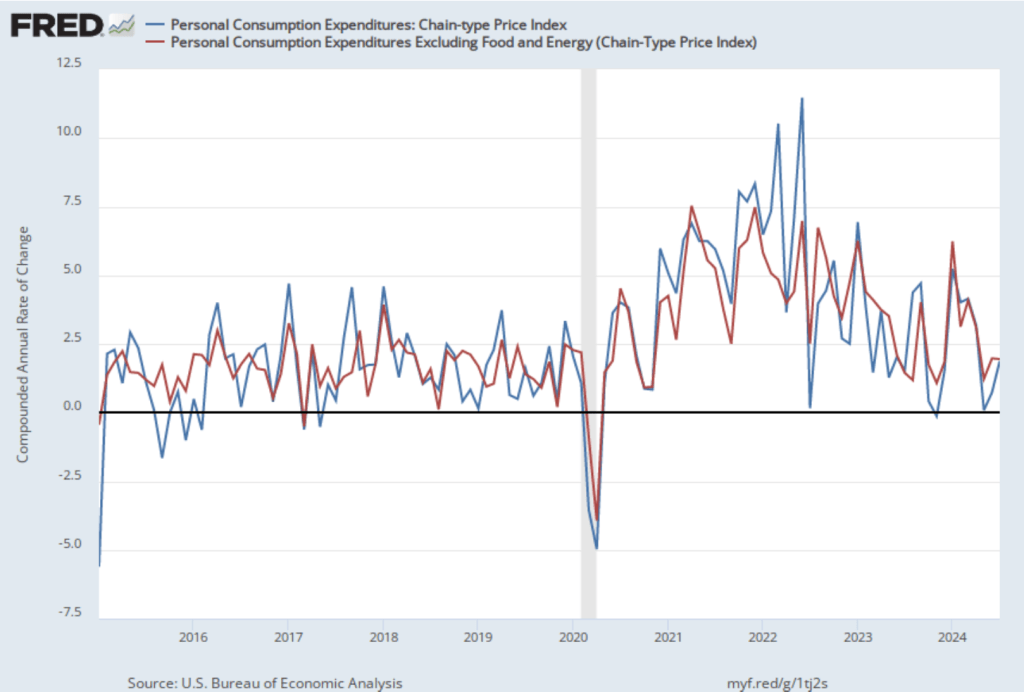

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation rose in July to 1.7 percent from 0.7 percent in July—although higher in July, inflation was below the Fed’s 2 percent target in both months. Core PCE inflation was 2.0 percent in July, which was unchanged from June. These data indicate that inflation has been at or below the Fed’s target for the last three months.

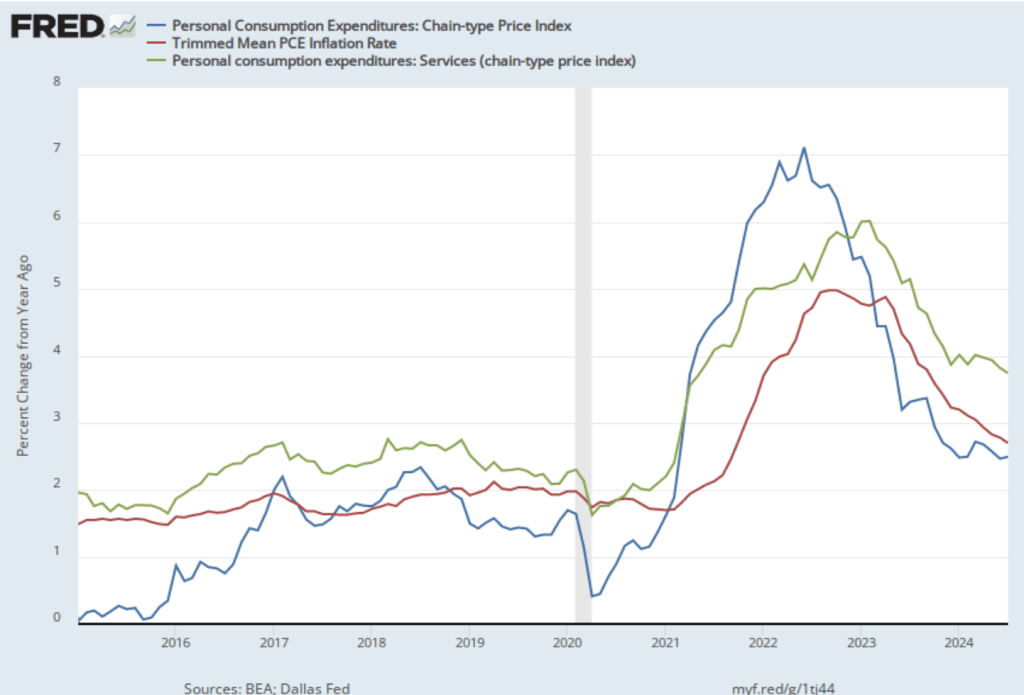

The following figure shows another way of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above), inflation measured using only the prices of the services included in the PCE (the green line), and the trimmed mean rate of PCE inflation (the red line). Fed Chair Jerome Powell and other members of the Federal Open Market Committee (FOMC) have said that they are concerned by the persistence of elevated rates of inflation in services. The trimmed mean measure is compiled by economists at the Federal Reserve Bank of Dallas by dropping from the PCE the goods and services that have the highest and lowest rates of inflation. It can be thought of as another way of looking at core inflation by excluding the prices of goods and services that had particularly high or particularly low rates of inflation during the month.

Inflation using the trimmed mean measure was 2.7 percent in July (calculated as a 12-month inflation rate), down only slightly from 2.8 percent in June—and still above the Fed’s target inflation rate of 2 percent. Inflation in services remained high in July at 3.7 percent, although down from 3.9 percent in June.

On balance, taking together these various measures, inflation seems on track to return to the Fed’s 2 percent target. As we noted in this earlier post, last week in a speech at the Federal Reserve Bank of Atlanta’s monetary policy symposium in Jackson Hole, Wyoming , Fed Chair Jerome Powell all but confirmed that the the Fed’s policy-maiking Federal Open Market Committee (FOMC) will cut its target for the federal funds rate at its next meeting on September 17-18. There was nothing in this latest PCE report to reduce the likelihood of the FOMC cutting its target at that meeting by an expected 0.25 percent point from a range of 5.25 percent to 5.50 percent to a range of 5.00 percent to 5.25 percent. There also is nothing in the report that would increase likelihood that the committee will cut its target by 0.50 percentage point, as many investors expected following the weak employment report released by the Bureau of labor Statistics (BLS) at the beginning of August. (We discuss this report and the reaction among investors in this post.)

A fundamental point in macroeconomics is that the value of income and the value of output or production are the same. The Bureau of Economic Analysis (BEA) measures the value of the U.S. economy’s production with gross domestic product (GDP) and the value of total income with gross domestic income (GDI). The two numbers are designed to be equal but because they are compiled from different data, the numbers can diverge. (We discuss GDP and GDI in the Apply the Connection “Was There a Recession during 2022? Gross Domestic Product versus Gross Domestic Income” in Macroeconomics, Chapter 8, Section 8.4 (Economics Chapter 18, Section 18.4).)

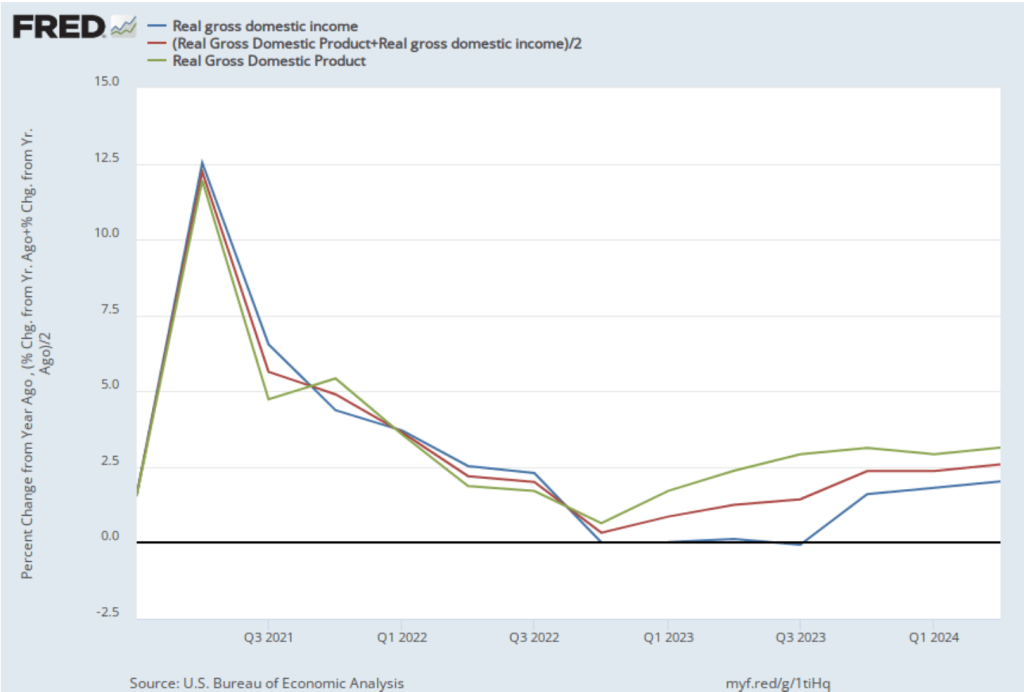

The figure above shows that in the past two years the growth rate of real GDP (the green line in the figure) has been significantly different—significantly higher—than the growth rate of GDI (the blue line). Both growth rates are measured as the percentage change from the same quarter in the previous year. Until the fourth quarter of 2022, the two growth rates were roughly similar over the period shown. But for the four quarters beginning in the fourth quarter of 2022, real GDI was flat with a growth rate of 0.0 percent, while real GDP grew at an average annual rate of 1.9 percent during that period. From the fourth quarter of 2023 through the second quarter of 2024, real GDI grew, but at an average annual rate of 1.8 percent, while real GDP was growing at a rate of 3.1 percent. (Some economists prefer to average the growth rates of GDP and GDI, which we show with the red line in the figure.)

In other words, judging by growth in real GDI, the U.S. economy was experiencing something between stagnation and moderate growth, while judging by growth in real GDP, the U.S. economy experiencing moderate to strong growth. There can be differences between GDP and GDI because (1) the BEA uses data on wages, profits, and other types of income to measure GDI, and (2) the errors in these data can differ from the errors in data on production and spending used to estimate GDP.

Jason Furman, chair of the Council of Economic Advisers under President Barack Obama, has suggested that a surge in immigration may explain why GDI growth has lagged GDP growth. As we discuss in this blog post, the Census Bureau may have been underestimating the number of immigrants who have entered the United States in recent years. The Congressional Budget Office (CBO) estimates that there are actually 6 million more people living in the United States in 2024 than the Census Bureau estimates because the bureau has underestimated the number of immigrants.

Compared to the native-born population, immigrants are disproportionately in the prime working ages of 25 to 54 and are therefore more likely to be in the labor force. It seems plausible—although so far as we know, the point hasn’t been documented—that the value of production resulting from the work of uncounted (in the census estimates) immigrants is more likely to be included in GDP than the income they are paid is to be counted in GDI. The result could explain at least part of the discrepancy between GDP and GDI that we’ve seen in the past two years. But while this factor affects the levels of GDP and GDI, it’s not clear that it affects the growth rates of GDP and GDI. The number of uncounted immigrants would have to be increasing over time for the growth rate of GDI to be reduced relative to the growth rate of GDP.

This episode may demonstrate the need for Congress to provide the BEA staff with resources they would need to do the work required to reconcile GDP estimates with GDI estimates.

Glenn discusses Fed policy, the state of the U.S economy, economic growth, China in the world economy, industrial policy, protectionism, and other topics in this episode of the Political Economy podcast from the American Enterprise Institute.

Image generated by GTP-4o of a woman singer performing at a concert.

The answer to the question in the title is “yes” according to a column by James Mackintosh in the Wall Street Journal. In the Apply the Concept “Taylor Swift Tries to Please Fans and Make Money,” in Chapter 11 of Microeconomics, we discussed how for her The Eras Tour, Taylor Swift reserved more than half of the concert tickets for her “verified fans.” The tickets sold to verified fans for an average price of $250.

On the resale market, prices of the tickets soared to $1,000 or more. Yet only about 5 percent of tickets purchased by verified fans were resold. Mackintosh’s wife and “eldest offspring” were in in the other 95 percent—they had purchased their tickets at a low price but wouldn’t resell them at a much higher price. Moreover—and this is where Mackintosh sees economics as breaking—if they didn’t already have the tickets they wouldn’t have bought them at the current high price.

Not being willing to buy something at a price you wouldn’t sell it for is inconsistent behavior because it ignores a nonmonetary opportunity cost. (As we discuss in Chapter 10, Section 10.4.) If Mackintosh’s wife won’t sell her ticket for $1,000, she incurs a $1,000 opportunity cost, which is the amount she gives up by not selling the ticket. The two alternatives—either paying $1,000 for a ticket or not receiving $1,000 by declining to sell a ticket—amount to exactly the same thing.

Mackintosh recognizes that the actions of his wife and offspring reflect what he calls a “mental bias,” which he correctly labels the endowment effect: The tendency to be unwilling to sell something you already own even if you are offered a price greater than the price you would be willing to buy the thing for if you didn’t already own it.

As we discuss in Chapter 10, the endowment effect is one of a number of results from behavioral economics, which is the study of situations in which people make choices that don’t appear to be economically rational. So, Mackintosh’s family—and other Swifties—didn’t break economics. Instead, they demonstrated one of the results of behavioral economics.