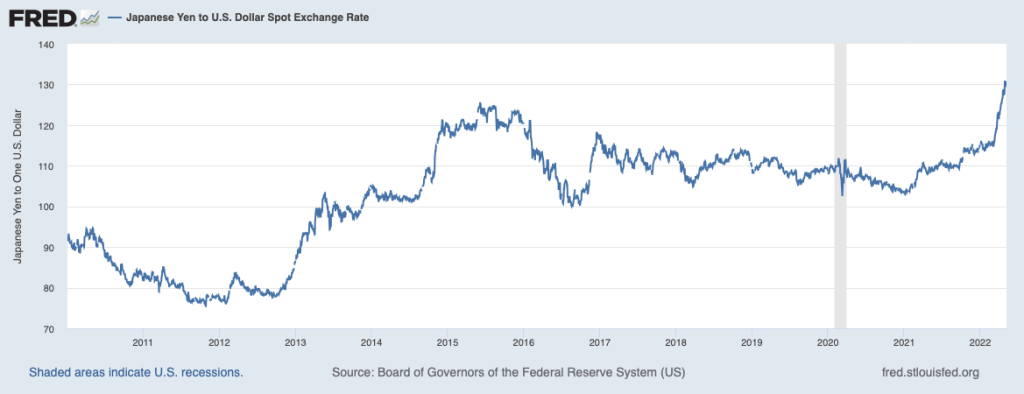

From early March to early May 2022, the Japanese yen persistently lost value versus the U.S. dollar. Between March 1 and May 9, the yen declined by 14% against the dollar, which is a substantial loss in value during such a short time period. What explains the decline in the exchange rate between the yen and the dollar during that time? In Macroeconomics, Chapter 18, Section 18.2 (Economics, Chapter 28, Section 28.2), we saw that the exchange rate between most pairs of currencies fluctuates in response to these factors:

- The foreign demand for U.S. goods

- U.S. interest rates relative to foreign interest rates

- Foreign demand for making direct investments or portfolio investments in the United States

- The U.S. demand for foreign goods

- Foreign interest rates relative to U.S interest rates

- U.S. demand for making direct investments or portfolio investments in other countries

The following figure shows movements in the exchange rate between the yen and the U.S. dollar since 2010. During different periods, the factor that is most important in explaining fluctuations in an exchange rate varies. (Important note: The figure follows the convention of expressing the exchange between the yen and dollar in terms of yen per dollar. Therefore, in the figure, an increase in the exchange rate corresponds to a decrease in the value of the yen versus the dollar because it takes more yen to buy one dollar.)

From early March to early May 2022, the decline in value of the yen versus the dollar was mainly the result of U.S. interest rates increasing relative to Japanese interest rates. As the inflation rate increased rapidly in the spring of 2022, both short-term and long-term interest rates in the United States increased, partly in response to policy actions taken by the Federal Reserve. The Federal Reserve was attempting to increase interest rates in order to raise borrowing costs for households and firms, thereby slowing spending and inflation. Japan was experiencing much lower rates of inflation—well below the Bank of Japan’s 2% annual inflation target—so the BOJ was reluctant to increase interest rates. As a consequence, the gap between the interest rate on 10-year U.S. Treasury notes and the interest rate on 10-year Japanese government bonds had risen to 2.9 percentage points.

Higher U.S. interest rates caused a shift to the right in the demand for dollars in exchange for yen as foreign investors exchanged their yen for dollars in order to buy U.S. Treasury securities and other U.S. financial assets. As we show in Chapter 18, Figure 18.13, an increase in the demand for dollars (holding all other factors constant) increases the equilibrium exchange rate between the yen and the dollar.

What effect does a stronger dollar and a weaker yen have on the two countries’ economies? A weaker yen means that the yen price of imports from the United States will be higher. The higher prices will increase the Japanese inflation rate, but with inflation being low in in the spring of 2022, Japanese policymakers weren’t concerned by this effect. And because the value of U.S. imports is small relative to the size of the Japanese economy, the effect on the inflation rate wouldn’t be large in any case. The dollar price of Japanese exports to the United States will be lower, which should help Japanese firms exporting to the United States.

The effect on the U.S. economy will be the mirror image of the effect on the Japanese economy. The dollar price of Japanese imports being lower will help reduce the U.S. inflation rate, but not to a great extent because the value of Japanese imports is small relative to the size of the U.S. economy. The yen price of U.S. exports to Japan will be higher, which will be bad news for U.S. firms exporting to Japan.

Finally, many banks, other financial firms, and non-financial firms borrow money in dollars. They do so because over time the advantages of borrowing dollars has increased, even for foreign firms that receive most of their revenue in their domestic currency rather than dollars. In particular, the value of the dollar is relatively stable compared with the value of many other currencies. In addition, the Federal Reserve has made available short-term dollar loans to foreign central banks that allow those banks to provide short-term loans to local firms that are having temporary difficulty making dollar payments on their loans. By late 2021, the total amount of dollar loans made outside of the United States had risen to more than $13 trillion. In the spring of 2022, the value of the dollar was rising not just against the Japanese yen but also against many other currencies. The increase was bad news for foreign firms borrowing in U.S. dollars because it would take more of their domestic currency to buy the dollars necessary to make their loans payments. A large and prolonged increase in the value of the U.S. dollar could possibly upset the stability of the international financial system.

Sources: Yuko Takeo and Komaki Ito, “Japan’s Stepped-Up Warnings Fail to Stem Yen’s Slide Past 128,” bloomberg.com, April 19, 2022; Jacky Wong, “Japan Gets a Taste of the Wrong Type of Inflation,” Wall Street Journal, April 1, 2022; Megumi Fujikawa, “Yen Hits Lowest Level Since 2015, and Japan, U.S. Are OK With That,” Wall Street Journal, March 28, 2022; Bank for International Settlements, “BIS International Banking Statistics and Global Liquidity Indicators at End-September 2021,” January 28, 2022; and Federal Reserve Bank of St. Louis.