There are many macroeconomic forecasts. Some forecasts are made by private economists, including those who work for Wall Street Investment firms. Other forecasts are made by economists who work for the government. Perhaps the most widely used macroeconomic forecasts are those published by economists who work for the Congressional Budget Office (CBO). The CBO is a nonpartisan agency within the federal government that provides estimates of the economic effects of government policies as part of the process by which Congress prepares the federal budget. One important aspect of the CBO’s work is to estimate future federal government budget deficits.

To forecast the size of future deficits, the CBO needs to forecast growth in key macroeconomic variables, including GDP. Faster growth in the U.S. economy should result in faster growth in federal tax revenues and slower growth in federal government transfer payments, including payments the federal government makes under the unemployment insurance system, the Temporary Assistance for Needy Families program, and the Supplemental Nutrition Assistance Program. When revenues grow faster than expenditures, the federal budget deficit shrinks.

The CBO’s forecasts of potential GDP provide perhaps the most best known projections of the future economic growth of the U.S. economy. The CBO calculates its forecasts of potential GDP by forecasting the variables that potential GDP depends on. As we’ve seen in Macroeconomics, Chapters 10 (Economics, Chapters 20), the two key variables in determining the growth in real GDP are the growth in labor productivity—the ratio of real GDP to the quantity of labor—and the growth of the labor force.

How well has the CBO forecast future U.S. economic growth? Or, equivalently, how well has the CBO forecast potential GDP. Each year the CBO publishes forecasts of potential GDP for the following 10 years and for longer periods—typically 40 or 50 years. Claudia Sahm, an economic consultant and opinion writer and formerly an economist at the Federal Reserve and the White House, has noted that the CBO’s 10-year forecasts of potential GDP have not been good forecasts of the actual growth of real GDP. Over the past 15 years, the CBO has also carried out surprisingly large downward revisions of its forecasts of potential GDP.

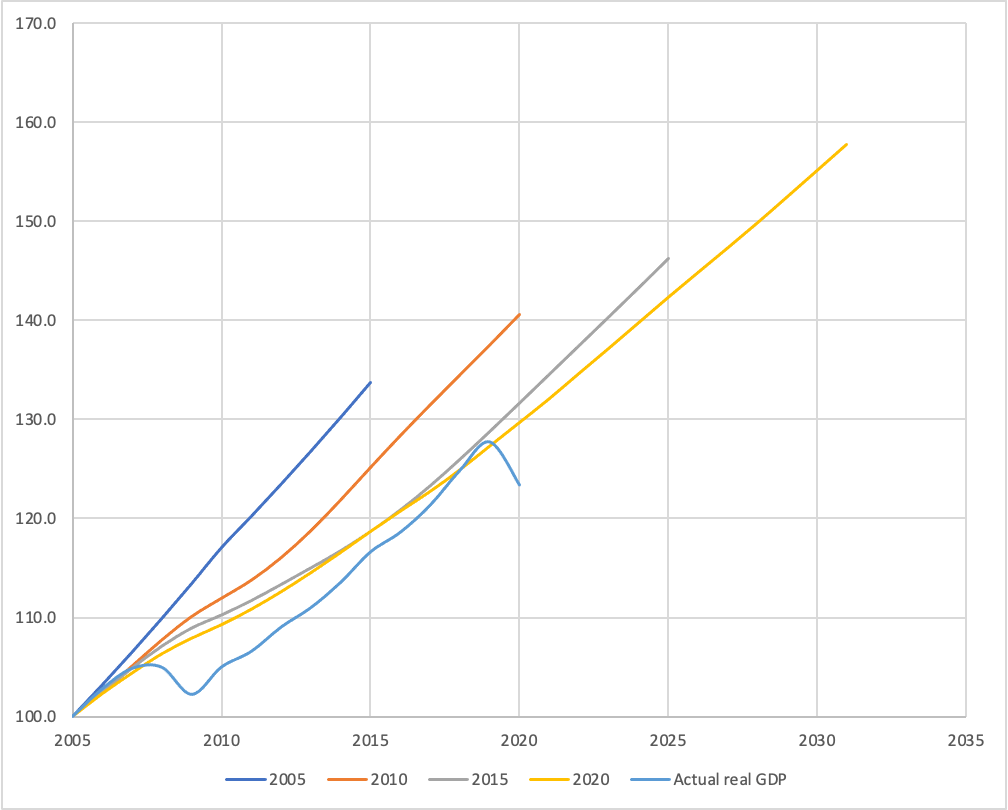

The figure below is similar to one prepared by Sahm and shows the forecasts of potential GDP the CBO published in 2005, 2010, 2015, and 2020 for the following 10 years. (For Sahm’s Twitter thread discussing her figure, click HERE.) That is, in 2005, the CBO issued a forecast of potential GDP for the years 2005–2015. In 2010, the CBO issued a forecast of potential GDP for the years 2010–2020, and so on. Note that for ease of comparison, all GDP values in the figure are set equal to a value of 100 in 2005.

Each straight line on the chart represents the CBO’s forecast of potential GDP over the 10 years following the year in which the forecast was published. For example, the top blue line represents the forecasts the CBO made in 2005 of the values of potential GDP for the years 2005 to 2015. The bottom blue line shows the actual values of real GDP for the years from 2005 to 2020. Note how at each five year interval, the CBO’s forecasts of potential GDP shifted down.

We can look at a few examples of how far off the CBO’s projections were. For instance, if the economy had grown as rapidly between 2005 and 2015 as the CBO forecast it would in 2005, real GDP would have been about 15 percent higher than it actually was. In other words, the U.S. economy would have produced about $2.5 trillion more in goods and services than it actually did. Similarly, if the economy had grown as rapidly between 2010 and 2019 as the CBO forecast it would in 2010, real GDP in 2019 would have been about 7.5 percent (or about $1.5 trillion) higher than it actually was.

Why has the CBO persistently overestimated the future growth rate of the U.S. economy? The main source of error has been the CBO’s overestimation of the growth in labor force productivity. They have also slightly overestimated the growth of the labor force. Claudia Sahm has a more basic criticism of the CBO’s approach to estimating potential GDP. She argues that if real GDP grows slowly during a period, perhaps because monetary and fiscal policies are insufficiently expansionary, the CBO will incorporate the lower actual real GDP values when it updates its forecasts of potential GDP. This approach can raise questions as to whether the CBO is actually measuring potential GDP as most economist’s define it (and as we define it in the textbook): The level real GDP attains when all firms are producing at capacity. Other economists share these concerns. For instance, Daan Struyven, Jan Hatzius, and Sid Bhushan of the Goldman Sachs investment bank, argue that the CBO’s estimate of potential GDP understates the true capacity of the U.S. economy by 3 to 4 percent.

The CBO’s substantial adjustments to its forecasts of potential GDP are another indication of how volatile the U.S. economy has been since the beginning of the 2007–2009 recession.

Sources: Tyler Powell, Louise Sheiner, and David Wessel, “What Is Potential GDP, and Why Is It So Controversial Right Now,” brookings.edu, February 22, 2021; and Congressional Budget Office, “Budget and Economic Data,” various years.

This was one of your best posts ever. A fascinating analysis–but disturbing in how bad the forecasts are made

LikeLike

Thanks. It is an eye-opener how far off their estimates are.

LikeLike