Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (June 18) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee noted that a key reason for keeping its target range unchanged was that: “Uncertainty about the economic outlook has diminished but remains elevated.” Committee members were unanimous in voting to keep its target range unchanged.

In his press conference following the meeting, Fed Chair Jerome Powell indicated that a key source of economic uncertainty was the effect of tariffs on the inflation rate. Powell indicated that the likeliest outcome was that tariffs would lead to the inflation rate temporarily increasing. He noted that: “Beyond the next year or so, however, most measures of longer-term expectations [of inflation] remain consistent with our 2 percent inflation goal.”

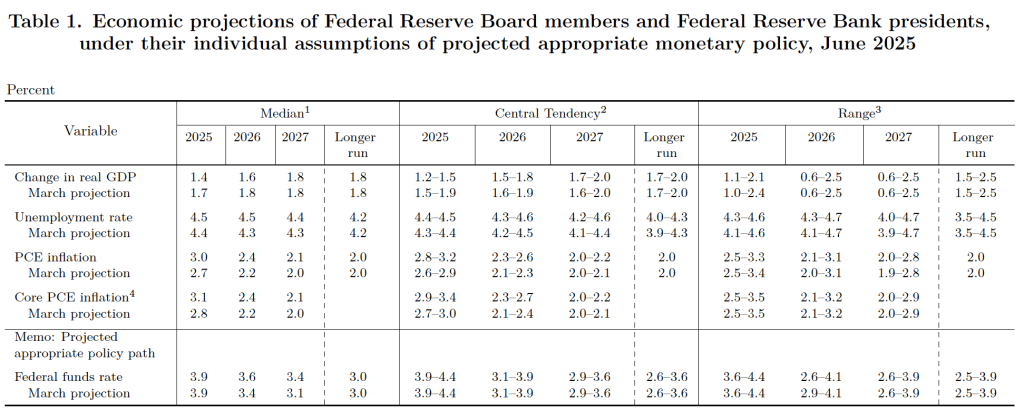

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does after its March, June, September, and December meetings. The SEP presents median values of the 18 committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

There are several aspects of these forecasts worth noting:

- Committee members reduced their forecast of real GDP growth for 2025 from 1.7 percent in March to 1.4 percent today. (It had been 2.1 percent in their December forecast.) Committee members also slightly increased their forecast of the unemployment rate at the end of 2025 from 4.4 percent to 4.5 percent. (The unemployment rate in May was 4.2 percent.)

- Committee members now forecast that personal consumption expenditures (PCE) price inflation will be 3.0 percent at the end of 2025. In March they had forecast that it would be 2.7 percent at the end of 2025, and in December, they had forecast that it would 2.5 percent. Similarly, their forecast of core PCE inflation increased from 2.8 percent to 3.1 percent. It had been 2.5 percent in December. The committee does not expect that PCE inflation will decline to the Fed’s 2 percent annual target until sometime after 2027.

- The committee’s forecast of the federal funds rate at the end of 2025 was unchanged at 3.9 percent. The federal funds rate today is 4.33 percent, which indicates that the median forecast of committee members is for two 0.25 percentage point (25 basis points) cuts in their target for the federal funds rate this year. Investors are similarly forecasting two 25 basis point cuts.

During his press conference, Powell indicated that because the tariff increases the Trump administration implemented beginning in April were larger than any in recent times, their effects on the economy are difficult to gauge. He noted that: “There’s the manufacturer, the exporter, the importer and the retailer and the consumer. And each one of those is going to be trying not to be the one to pay for the tariff, but together they will all pay together, or maybe one party will pay it all.” The more of the tariff that is passed on to consumers, the higher the inflation rate will be.

Earlier today, President Trump reiterated his view that the FOMC should be cutting its target for the federal funds rate, labeling Powell as “stupid” for not doing so. Trump has indicated that the Fed should cut its target rate by 1 percentage point to 2.5 percentage points in order to reduce the U.S. Treasury’s borrowing costs. During World War II and the beginning of the Korean War, the Fed pegged the interest rates on Treasury securities at low levels: 0.375 percent on Treasury bills and 2.5 percent on Treasury bonds. Following the Treasury-Federal Reserve Accord, reached in March 1951, the Federal Reserve was freed from the obligation to fix the interest rates on Treasury securities. (We discuss the Accord in Chapter 13 of Money, Banking, and the Financial System.) Since that time, the Fed has focused on its dual mandate of maximum employment and price stability and it has not been directly concerned with affecting the Treasury’s borrowing cost.

Barring a sharp slowdown in the growth of real GDP, a significant rise in the unemployment rate, or a significant rise in the inflation rate, the FOMC seems unlikely to change its target for the federal funds rate before its meeting on September 16–17 at the earliest.