Supports: Hubbard/O’Brien, Chapter 24, Money, Banks, and the Federal Reserve System; Macroeconomics Chapter 14; Essentials of Economics Chapter 16.

Apply the Concept: WHAT DO BANK RUNS TELL US ABOUT PANIC TOILET PAPER BUYING DURING THE CORONAVIRUS PANDEMIC?

Here’s the key point: Lack of confidence leads to panic buying, but a return of confidence leads to a return to normal buying.

In Chapter 24, Section 24.4 of the Hubbard and O’Brien Economics 8e text (Chapter 14, Section 14.4 of Macroeconomics 8e) we discuss the problem of bank runs that plagued the U.S. financial system during the years before the Federal Reserve began operations 1914. During the 2020 coronavirus epidemic in the United States consumers bought most of the toilet paper available in supermarkets leaving the shelves bare. Toilet paper runs turn out to be surprisingly similar to bank runs.

First, consider bank runs. The United States, like other countries, has a fractional reserve banking system, which means that banks keep less than 100 percent of their deposits as reserves. During most days, banks will experience roughly the same amount of funds being withdrawn as being deposited. But if, unexpectedly, a large number of depositors simultaneously attempt to withdraw their deposits from a bank, the bank experiences a run that it may not be able to meet with its cash on hand. If large numbers of banks experience runs, the result is a bank panic that can shut down the banking system.

Runs on commercial banks in the United States have effectively ended due to the combination of the Federal Reserve acting as a lender of last resort to banks experiencing runs and the Federal Deposit Insurance Corporation (FDIC) insuring bank deposits (currently up to $250,000 per person, per bank). But consider the situation prior to 1914. As a depositor in a bank during that period, if you had any reason to suspect that your bank was having problems, you had an incentive to be at the front of the line to withdraw your money. Even if you were convinced that your bank was well managed and its loans and investments were sound, if you believed the bank’s other depositors thought the bank had a problem, you still had an incentive to withdraw your money before the other depositors arrived and forced the bank to close. In other words, in the absence of a lender of last resort or deposit insurance, the stability of a bank depends on the confidence of its depositors. In such a situation, if bad news—or even false rumors—shakes that confidence, a bank will experience a run.

Moreover, without a system of government deposit insurance, bad news about one bank can snowball and affect other banks, in a process called contagion. Once one bank has experienced a run, depositors of other banks may become concerned that their banks might also have problems. These depositors have an incentive to withdraw their money from their banks to avoid losing it should their banks be forced to close.

Now think about toilet paper in supermarkets. From long experience, supermarkets, such as Kroger, Walmart, and Giant Eagle, know their usual daily sales and can place orders that will keep their shelves stocked. The same is true of online sites like Amazon. By the same token, manufacturers like Kimberly-Clark and Procter and Gamble, set their production schedules to meet their usual monthly sales. Consumers buy toilet paper as needed, confident that supermarkets will always have some available.

Photo of empty supermarket shelves taken in Boston, MA in March 2020. Credit: Lena Buananno

But then the coronavirus hit and in some states non-essential businesses, colleges, and schools were closed and people were advised to stay home as much as possible. Supermarkets remained open everywhere as did, of course, online sites such as Amazon. But as people began to consider what products they would need if they were to remain at home for several weeks, toilet paper came to mind.

At first only a few people decided to buy several weeks worth of toilet paper at one time, but that was enough to make the shelves holding toilet paper begin to look bare in some supermarkets. As they saw the bare shelves, some people who would otherwise have just bought their usual number of rolls decided that they, too, needed to buy several weeks worth, which made the shelves look even more bare, which inspired more to people to buy several weeks worth, and so on until most supermarkets had sold out of toilet paper, as did Amazon and other online sites.

Before 1914 if you were a bank depositor, you knew that if other depositors were withdrawing their money, you had to withdraw yours before the bank had given out all its cash and closed. In the coronavirus epidemic, you knew that if you failed to rush to the supermarket to buy toilet paper, the supermarket was likely to be sold out when you needed some. Just as banks relied on the confidence of depositors that their money would be available when they wanted to withdraw it, supermarkets rely on the confidence of shoppers that toilet paper and other products will be available to buy when they need them. A loss of that confidence can cause a run on toilet paper just as before 1914 a similar loss of confidence caused runs on banks.

In bank runs, depositors are, in effect, transferring a large part of the country’s inventory of currency out of banks, where it’s usually kept, and into the depositors’ homes. Similarly, during the epidemic, consumers were transferring a large part of the country’s inventory of toilet paper out of supermarkets and into the consumers’ homes. Just as currency is more efficiently stored in banks to be withdrawn only as depositors need it, toilet paper is more efficiently stored in supermarkets (or in Amazon’s warehouses) to be purchased only when consumers need it.

Notice that contagion is even more of a problem in a toilet paper run than in a bank run. People can ordinarily only withdraw funds from banks where they have a deposit, but consumers can buy toilet paper wherever they can find it. And during the epidemic there were news stories of people traveling from store to store—often starting early in the morning—buying up toilet paper.

Finally, should the government’s response to the toilet paper run of 2020 be similar to its response to the bank runs of the 1800s and early 1900s? To end bank runs, Congress established (1) the Fed—to lend banks currency during a run—and (2) the FDIC—to insure deposits, thereby removing a depositor’s fear that the depositor needed to be near the head of the line to withdraw money before the bank’s cash holdings were exhausted.

The situation is different with toilet paper. Supermarkets are eventually able to obtain as much toilet paper as they need from manufacturers. Once production increases enough to restock supermarket shelves, consumers—many of whom already have enough toilet paper to last them several weeks—stop panic buying and ample quantities of toilet paper will be available. Once consumers regain confidence that toilet paper will be available when they need it, they have less incentive to hoard it. Just as a lack of confidence leads to panic buying, a return of confidence leads to a return to normal buying.

Although socialist countries such as Venezuela, Cuba, and North Korea suffer from chronic shortages of many goods, market economies like the United States experience shortages only under unusual circumstances like an epidemic or natural disaster.

Note: For more on bank panics, see Hubbard and O’Brien, Money, Banking, and Financial Markets, 3rd edition, Chapter 12 on which some of this discussion is based.

Sources: Sharon Terlep, “Relax, America: The U.S. Has Plenty of Toilet Paper,” Wall Street Journal, March 16, 2020; Matthew Boyle, “You’ll Get Your Toilet Paper, But Tough Choices Have to Be Made: Grocery CEO,” bloomberg.com, March 18, 2020; and Michael Corkery and Sapna Maheshwari, “Is There Really a Toilet Paper Shortage?” New York Times, March 13, 2020.

Question

Suppose that as a result of their experience during the coronavirus pandemic, the typical household begins to store two weeks worth of toilet paper instead of just a few days worth as they had previously been doing. Will the result be that toilet paper manufacturers permanently increase the quantity of toilet paper that they produce each week?

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.

Supports: Hubbard/O’Brien, Economics, Chapter 25 – Monetary Policy (Macro Chapter 15 and Essentials Chapter 17), and Chapter 26 – Fiscal Policy (Macro Chapter 16 and Essentials Chapter 18).

The Great Recession of 2007-2009 was the worst economic contraction in the United States since the Great Depression of the 1930s. Accordingly, it brought a vigorous response from federal policymakers. As of late March 2020, it was too soon to tell how severe the economic contraction from the coronavirus pandemic might be. But policymakers had already responded with major initiatives. In the following sections, we compare monetary and fiscal policies employed during the Great Recession and those employed at the beginning of the coronavirus pandemic.

A Brief History of U.S. Recessions

Historically, most recessions in the United States have been caused by one of two often related factors: (1) A financial crisis or (2) Federal Reserve actions taken to reduce the inflation rate. The two main exceptions are the recession of 1973-1975, which was primarily the result of a sharp increase in oil prices, and the recession of 2020, which was the result of the effects of the coronavirus pandemic and of the business closures ordered by state and local governments in an attempt to contain the pandemic.

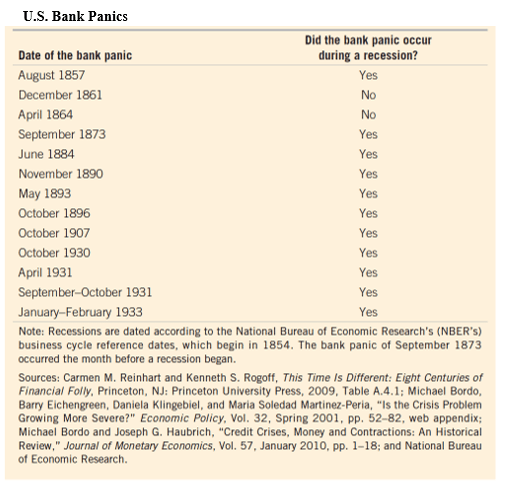

Prior to 1914, the United States lacked both a central bank that could act as a lender of last resort to keep bank runs from escalating into bank panics and a system of deposit insurance. By cutting off many businesses from their main source of credit and cutting off both households and firms from their bank deposits, bank panics resulted in declines in production and employment. The failure of the Federal Reserve to effectively deal with the waves of bank panics from 1930 to 1933 at the beginning of the Great Depression led Congress in 1934 to establish the Federal Deposit Insurance Corporation (FDIC) to insure deposits in commercial banks (currently up to $250,000 per depositor, per bank). The following table shows that prior to World War II (U.S. participation lasted from 1941 to 1945), most recessions were associated with bank panics.

As a result of deposit insurance and more active Federal Reserve discount lending, after World War II problems in the commercial banking system were no longer a major source of instability in the U.S. economy. As the following figure shows, declines in residential construction have preceded every recession in the United States since 1958 (the shaded areas represent periods of recession). Edward Leamer of the University of California, Los Angeles had gone so far as to argue that “housing is the business cycle.” Prior to the housing crash that preceded the Great Recession, the main cause of the declines in residential construction shown in the figure were rising mortgage interest rates, typically due to the Federal Reserve raising its target for the federal funds rate—the interest rate that banks charge each other on overnight loans—in response to increases in the inflation rate.

Monetary Policy during the Great Recession

Both the Great Recession of 2007-2009 and pre-World War II recessions were accompanied by financial panics. Both the Great Recession of 2007-2009 and post-World War II recessions were accompanied by sharp downturns in the housing market.

But the Great Recession differed from earlier recessions two key ways: First, it was caused by problems internal to the housing market rather than the effect on the housing market of contractionary monetary policy; and second, it did not involve commercial banks. Instead, it involved the shadow banking sector of investment banks, money market mutual funds, and insurance companies.

Problems began in the market for mortgage-backed securities—bonds that consisted of mortgages bundled together. The value of the bonds depended on the value of the underlying mortgages. When housing prices began to decline in 2006, borrowers began defaulting on mortgages. Many commercial and investment banks owned these mortgage-backed securities, so the decline in the value of the securities caused these banks to suffer heavy losses. By mid-2007, investors and policymakers became concerned about the decline in the value of mortgage-backed securities and the large losses suffered by commercial and investment banks. Many investors refused to buy mortgage-backed securities, and some investors would buy only bonds issued by the U.S. Treasury.

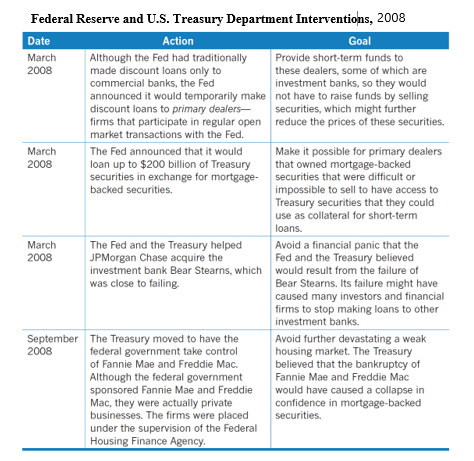

The problems in financial markets resulting from the bursting of the housing bubble were severe, particularly after the failure of the Lehman Brothers investment bank in September 2008. In previous recessions, the focus of the Fed’s expansionary policy had been on cutting its target for the federal funds rate to reduce borrowing costs and spur spending, particularly spending on residential construction. The Fed did rapidly cut its target for the federal funds rate from 5.25 percent in September 2007 to effectively 0 percent in December 2008. But the financial crisis reduced the effect of these rate cuts because the flow of funds through the financial system had largely dried up. As a result, the Fed entered into an unusual partnership with the U.S. Treasury Department and intervened in financial markets in unprecedented ways, which we summarize in the following table. In addition to the actions shown in the table, for the first time since the 1930s, the Fed bought commercial paper—short-term bonds issued by corporations—because many firms found their usual sources of funds were no longer available in the crisis. The Fed’s aim was to restore the flow of funds through the financial system to enable firms to obtain the credit they needed to maintain production and employment.

Fiscal Policy during the Great Recession

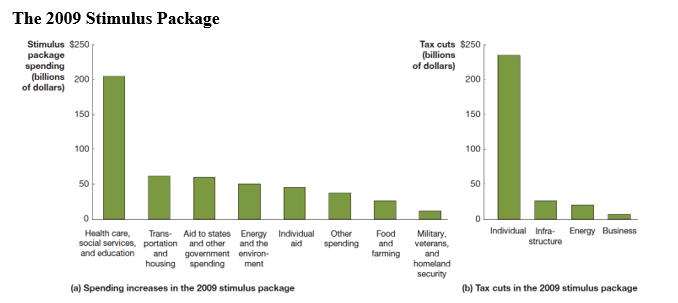

Presidents George W. Bush and Barack Obama both initiated fiscal policy responses to the Great Recession. In 2008, President Bush and Congress enacted a tax cut that took the form of rebates of taxes had already paid. After taking office in January 2009, President Obama and Congress enacted the $840 billion American Recovery and Reinvestment Act (AARA), often called the “stimulus package.” The following figure summarizes the spending and tax cuts in the ARRA.

During the Great Recession, the Fed’s monetary policy moved well beyond its usual focus on targeting the federal funds rate. But fiscal policy was more conventional: Increasing government spending and cutting taxes to increase aggregate demand, real GDP, and employment. The ARRA was notable mainly because of its size.

Monetary Policy in Response to the Coronavirus Epidemic

During 2019, prior to the epidemic beginning to affect the United States, the Fed had twice cut its target for the federal funds rate in response to a slowing rate of economic growth. With the spread of the coronavirus at the start of 2020, the Fed again cut its target twice, returning it effectively to 0 percent in mid-March. With many businesses closed and many consumers largely confined to their homes, the Fed knew that lower borrowing costs would not be the key to maintaining economic activity. Accordingly, the Fed revived some of the lending facilities that it had used during the 2007-2009 financial crisis and set up some new facilities with the goal of maintaining the flow of funds through the financial system and the ability of firms whose revenues had plunged to continue to access credit.

Here is a summary of Fed’s policy actions during March and early April 2020:

Cuts to the Federal Funds Rate The Fed reduced its target for the federal funds rate from a range of 1.75 percent to 1.50 percent to a range of 0 percent to 0.25 percent.

Purchases of Mortgage-Backed Securities To provide funds to the market for mortgage lending, the Fed began purchasing mortgage-backed securities guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae, which are government-sponsored enterprises (GSEs).

Central Bank Liquidity Swap Lines To meet a surge in demand by foreign businesses and governments for U.S. dollars, the Fed expanded its Central Bank Liquidity Swap Lines, which allow foreign central banks to exchange their currencies for dollars.

Facility for Foreign and International Monetary Authorities To further help foreign central banks meet the demand for U.S. dollars by foreign businesses and governments, the Fed established the Foreign and International Monetary Authorities repurchase agreement facility, which allowed these authorities to “temporarily exchange their U.S. Treasury securities held with the Federal Reserve for U.S. dollars, which can then be made available to institutions in their jurisdictions.” This new facility reduced the need for foreign central banks to sell U.S. Treasury securities to obtain U.S. dollars. Those sales had been contributing to volatility in the market for U.S. Treasury securities.

Primary Dealer Credit Facility To ensure the liquidity of the 24 primary dealers, which are the large financial firms who interact with the Fed in securities markets, the Fed established the Primary Dealer Credit Facility to provide loans to these dealers.

Commercial Paper Funding Facility To ensure that corporations would have access to short-term funds necessary to meet payrolls and pay their suppliers, the Fed established the Commercial Paper Funding Facility to buy commercial paper from corporations.

Primary Market Corporate Credit Facility To ensure that corporations have access to longer-term funds, the Fed established the Primary Market Corporate Credit Facility to make loans to corporations whose bonds are rated investment grade by Moody’s, S&P, and Fitch, the private bond rating agencies.

Secondary Market Corporate Credit Facility To ensure the smooth functioning of the corporate bond market, the Fed established the Secondary Market Corporate Credit Facility to buy in the secondary market investment grade bonds issued by corporations and to buy shares in exchange-traded funds that are primarily invested in such bonds. First established in March, the facility was expanded in April to allow for the purchase of some non-investment grade corporate bonds and the purchase of shares in exchange-traded funds that are invested in such bonds.

Term Asset-Backed Securities Loan Facility (TALF) To support the flow of credit to consumers and businesses, the Fed began buying asset-backed securities (ABS) backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA).

Municipal Liquidity Facility To support the ability of state, county, and city governments to borrow, the Fed began buying short-term state and local bonds.

Main Street New Loan Facility (MSNLF) and Main Street Expanded Loan Facility (MSELF) To ensure that small and medium size businesses had the financial resources to survive the crisis, the Fed offered 4-year loans to companies employing up to 10,000 workers or with revenues of less than $2.5 billion. Principal and interest payments were deferred for one year. The facility was intended to augment the Paycheck Protection Programs, which was part of the CARES act and involves loans administered through the federal government’s Small Business Administration to firms with 500 or fewer employees.

In taking these actions, the Fed relied on its authority under Section 13(3) of the Federal Reserve Act, which authorizes the Fed under “unusual and exigent circumstances” to lend broadly. Following the 2007-2009 financial crisis, Congress amended the Federal Reserve Act to require that the Fed receive the prior approval for such actions from the Secretary of the Treasury. After consultation with Fed Chair Jerome Powell, Treasury Secretary Steven Munchin provided the required approval. As in the 2007-2009 financial crisis, the Fed was again conducting monetary policy in collaboration with the U.S. Treasury, rather than operating independently, as it had prior to 2007.

It remains to be seen whether these extraordinary actions will be sufficient to keep funds flowing through the financial system and to provide sufficient credit to allow businesses whose revenues had plunged to remain solvent.

Fiscal Policy in Response to the Coronavirus Epidemic

During the week of March 15, 2020, more than 3 million workers applied for federal unemployment benefits—five times more than had ever previously applied during a single week. Congress and President Donald Trump responded to the crisis by passing three aid packages by the end of March 2020, with the likelihood that further aid packages would be passed during the following weeks.

Unlike with fiscal policy actions during previous recessions, including the ARRA passed during the Great Recession, the main goal of these aid packages was not to directly stimulate aggregate demand by increasing government spending and cutting taxes. With many businesses closed and people in some states being asked to “shelter in place” or stay home except for essential trips such as buying groceries, a stimulus package of the conventional type was unlikely to be effective. Congress and the president instead focused on (1) helping businesses to remain open after many had experienced enormous declines in revenue and (2) providing households with sufficient funds to pay their rent or mortgage, buy groceries, and cover other essential spending.

Here is a summary of Congress and the president’s first three fiscal policy actions:

Research Funding and Aid to State and Local Governments In early March, Congress and the president passed an $8.3 billion bill to provide funds for research into a vaccine for the coronavirus and for state and local governments to help cover some of their costs in fighting the virus.

Increases in Benefits and Tax Credits In mid-March, Congress and the president passed a $100 billion bill aimed at increasing unemployment benefits, increasing benefits under the Supplemental Nutrition Assistance Program ( also called food stamps), and providing tax credits to firms offering paid sick leave to employees.

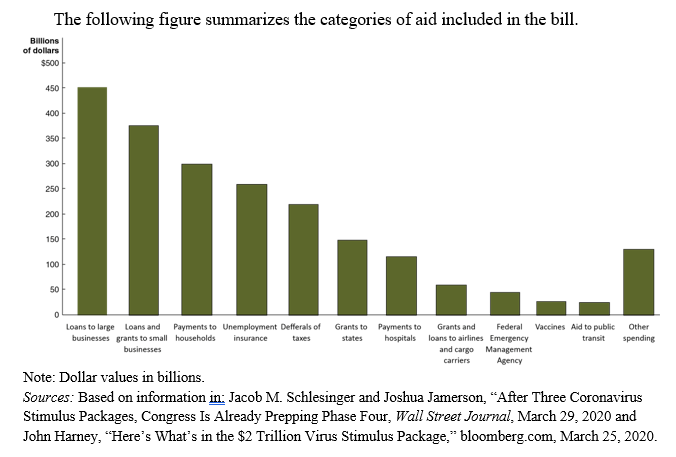

Coronavirus Aid, Relief and Economic Security (CARES) Act On March 27, Congress and the president passed the Coronavirus Aid, Relief and Economic Security (CARES) Act, a more than $2 trillion aid package—by far the largest fiscal policy action in U.S. history—to provide:

Direct payments to households

Supplemental unemployment insurance payments

Funds to state governments to offset some of their costs in fighting in the epidemic

Loans and grants to businesses

The macroeconomic policy actions undertaken by the Fed, Congress, and the president in the spring of 2020 were unprecedented in size and scope. Whether they would be effective in keeping the coronavirus epidemic from causing a major recession in the United States remains to be seen.

Note: Some of the figures and tables reproduced here were first published in Hubbard and O’Brien, Economics, 6th and 8th editions or Hubbard and O’Brien, Money, Banking, and Financial Markets, 3rd edition.

Sources: Federal Reserve Bank of New York, “New York Fed Actions Related to COVID-19,” newyorkfed.org; Board of Governors of the Federal Reserve System, “Text of the Federal Reserve Act: Section 13. Powers of Federal Reserve Banks,” federalreserve.gov, February 13, 2017; Nick Timiraos, “Fed Cuts Rates to Near Zero and Will Relaunch Bond-Buying Program,” Wall Street Journal, March 26, 2020; Eric Morath, Jon Hilsenrath and Sarah Chaney, “Record Rise in Unemployment Claims Halts Historic Run of Job Growth,” Wall Street Journal, March 18, 2020; Emily Cochrane, “House Passes $8.3 Billion Emergency Coronavirus Response Bill,” New York Times, March 9, 2020; and John Harney, “Here’s What’s in the $2 Trillion Virus Stimulus Package,” bloomberg.com, March 25, 2020.

Questions

1. There are both similarities and differences between monetary policies employed during the Great Recession of 2007-2009 and those employed at the beginning of the coronavirus pandemic in 2020.

(a) How has the Fed attempted to stimulate the economy during a typical recession?

(b) Briefly discuss ways in which the Fed’s approach during the Great Recession and during the coronavirus pandemic was similar.

(c) Briefly discuss ways in which the Fed’s approach during the Great Recession and during the coronavirus pandemic differed.

2. There are both similarities and differences between fiscal policies employed during the Great Recession of 2007 – 2009 and those employed at the beginning of the coronavirus pandemic of 2020.

(a) How have Congress and the president attempted to stimulate the economy during a typical recession?

(b) Briefly discuss ways in which Congress and the president’s approach during the Great Recession and during the coronavirus pandemic was similar to traditional expansionary policy.

(c) Briefly discuss how Congress and the president’s approach during the Great Recession and during the coronavirus pandemic differed from traditional expansionary policy.

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.

Supports: Hubbard/O’Brien, Chapter 23, Aggregate Demand and Aggregate Supply Analysis; Macroeconomics Chapter 13; Essentials of Economics Chapter 15.

Apply the Concept: Using the Aggregate Demand and Aggregate Supply Model to Analyze the Coronavirus Pandemic

Here’s the key point: The coronavirus caused large shifts in short-run aggregate supply and in aggregate demand, so this virus caused by far the largest decline in real GDP and largest increase in unemployment over such a brief period in U.S. history.

In early 2020, the United States experienced an epidemic from a novel coronavirus that causes the disease Covid-19. We can use the aggregate demand and aggregate supply model to analyze some of the key macroeconomic effects on the U.S. economy from this epidemic. As we’ve seen, economists distinguish between recessions caused by an aggregate supply shock, such as an unexpected increase in oil prices, or an aggregate demand shock, such as a decline in spending on new houses. The effects of the coronavirus combined both an aggregate supply shock and an aggregate demand shock.

To this point, we have discussed negative aggregate supply shocks that shift only the short-run aggregate supply curve to the left, leaving the aggregate demand curve unaffected. It’s usually reasonable to assume that the aggregate demand curve doesn’t shift when analyzing the effects of the two main types of supply shocks: (1) a supply shock caused by an increase in the cost of producing goods and services; or (2) a supply shock that reduces the capacity of firms to produce goods and services.

An example of the first type of supply shock is an increase in oil prices. Higher oil prices increase the cost of producing many goods and services, shifting the short-run aggregate supply curve to the left. (See panel (a) of Figure 23.7 in the Hubbard and O’Brien 8th edition text). Total spending in the economy declines, which we show as a movement along the aggregate demand curve (not as a shift in the aggregate demand curve). That movement is the result of the higher price level reducing the spending of households and firms on consumption, investment, and net exports.

The second type of supply shock reduces the capacity of firms and is typically the result of a natural disaster such as the Tohoku earthquake that Japan experienced in 2011. The earthquake triggered a tsunami that disabled the nuclear power plant in the city of Fukushima. The disruption in the power supply to several cities, including Tokyo took months to resolve. During this period, the ability of many Japanese firms to produce goods and services was reduced, causing the short-run aggregate supply curve to shift to the left. Notice that a natural disaster will also have some effect on aggregate demand if there are deaths (about 16,000 people in Japan died as a result of the Tohoku earthquake and tsunami) or if some firms are physically destroyed, making their workers unemployed, thereby reducing the workers’ incomes and their consumption spending. But because the resulting shift of the aggregate demand curve is likely to be small relative to the shift in the short-run aggregate supply curve, it makes sense to concentrate on the effects of the shift in short-run aggregate supply.

The coronavirus pandemic was an unprecedented supply shock to the U.S. economy. The virus originated in the city of Wuhan in China. A number of U.S. firms rely on Chinese suppliers in the Wuhan area. In January 2020, as the government of China closed factories in that area to control the spread of the virus, some U.S. firms, including Apple and Nike, announced that they would be unable to meet their production goals because some of their suppliers had shut down. By March, as the virus began to become widespread in the United States, governors in a number of states ordered all non-essential firms to close.

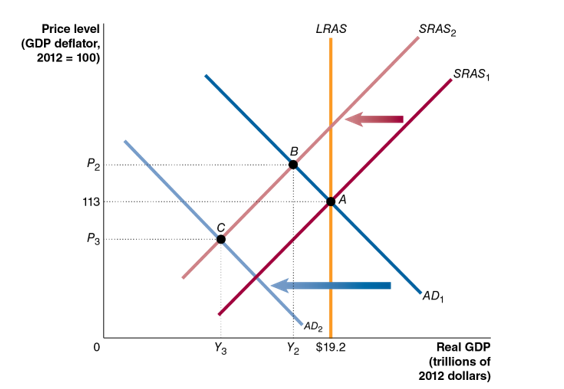

The following figure illustrates the effects of the virus on U.S. real GDP and the price level. In the figure, at the beginning of 2020, the economy was in long-run macroeconomic equilibrium, with the short-run aggregate supply curve, SRAS1, intersecting the aggregate demand curve, AD1, at point A on the long-run aggregate supply curve, LRAS. Equilibrium occurred at real GDP of $19.2 trillion and a price level of 113. By disrupting the global supply chains of U.S. firms and by leading governments to order the closure of many businesses, the virus caused the short-run aggregate supply curve to shift to the left from SRAS1 to SRAS2. (Note that in the following discussion, we are using the basic aggregate demand and aggregate supply model. In this model, there is no economic growth, so the long-run aggregate supply curve (LRAS) doesn’t shift.)

If the virus had caused a supply shock of the first type that we described earlier—affecting the economy in a way similar to a large increase in oil prices—the new short-run equilibrium would have occurred at point B. Real GDP would have declined from $19.2 trillion to Y2 and the price level would have risen from 113 to P2. (We prepared this content and graph in early April, so we don’t yet know the full effects of the virus on the economy. We therefore don’t attempt to put actual values on the new short-run equilibrium real GDP and price level.)

But point B was not the new short-run equilibrium for several reasons:

Reduced consumption spending The government closed many businesses, directly reducing output resulting in millions of workers losing their jobs. As workers experienced falling incomes, they reduced their consumption spending.

Reduced investmentspending Many residential and business construction projects had to be suspended, reducing investment spending.

Reduced exports U.S. exports declined because the pandemic also led to closures of businesses in Europe, Canada, Japan, and other U.S. trading partners.

As a result of these factors, the United States experienced a sharp decline in total spending in the economy, shifting the aggregate demand curve to the left from AD1 to AD2. In analyzing the supply shock resulting from the coronavirus, we have to include the effect on aggregate demand, which we ignore when considering supply shocks caused by higher oil prices or by a natural disaster, such as an earthquake.

Because the coronavirus pandemic caused both the SRAS and the AD curves to shift to the left, the new short-run equilibrium occurred at point C, with real GDP having fallen to Y3 and the price level having declined to P3. Note that if the shift of the SRAS curve had been larger than the shift of the AD curve, real GDP would have fallen further and the price level would have risen, rather than fallen.

The coronavirus pandemic resulted in very large shifts in short-run aggregate supply and in aggregate demand, so this virus caused by far the largest decline in real GDP and largest increase in unemployment over such a brief period in the history of the United States. The U.S. economy also suffered a large decline in real GDP and a substantial increase in unemployment during the Great Depression of the 1930s. But the decline in the U.S. economy during that economic contraction had been stretched out over the period from August 1929 to March 1933, rather than happening suddenly as was true with the contraction caused by the coronavirus.

Sources: Ruth Simon and Austen Hufford, “Not Just Nike and Apple: Small U.S. Firms Disrupted by Coronavirus,” Wall Street Journal, February 21, 2020; Eric Morath, Jon Hilsenrath, and Sarah Chaney, “Record 3.28 Million File for U.S. Jobless Benefits,” Wall Street Journal, March 26, 2020; and “158 Million Americans Told to Stay Home, but Trump Pledges to Keep It Short,” New York Times, March 26, 2020.

Question

During the spring of 2020, many state and local governments ordered most non-essential businesses to close. Suppose that, as a result, the short-run aggregate supply curve, SRAS, shifted to the left by more than did the aggregate demand curve, AD. On the graph shown here, draw in a new SRAS given this assumption. Label this curve SRAS3. Label the new equilibrium level of real GDP Y4 and the new equilibrium price level P4. Briefly explain the relationship between Y3 and Y4 and between P3 and P4, as shown in your graph.

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.

On March 19th Glenn Hubbard sat down with the editorial team at Pearson to talk through some of the high-level economic issues involved in the coronavirus pandemic.

In this 10 minute podcast Glenn discusses the nature of the economic shock and what we should expect, based on historical shocks. We explore every day topics students are wondering about like what will the job market look like to the policy ideas of what could help stabilize the US economy.

Give your students the link and ask them any of the following discussion questions to get them thinking about the pandemic in an economic context:

1. Is this kind of economic supply shock a new concept or something that the U.S. has experienced before? Is there any precedent for whether this should be a short or drawn out recession? What factors will contribute to the length of the recession?

2. What economic policies would you prescribe for dealing with this crisis and why? Which policy would be the most beneficial for families given the current state of the economy? Which policies would be the most beneficial for businesses and long-term economic growth?

3. What current mandates as a result of the pandemic could translate into longer-term modifications to how we learn and work? Discuss the possible structural changes to the economy.

4. What are the trade-offs involved in controlling the pandemic? Assuming there will be a significant impact on the economy, what macroeconomic policies would you implement to soften the shock to allow people to more easily follow the guidelines to reduce the pandemic without suffering severe economic consequences? Will your policies help restart the economy once the pandemic has passed?

Instructors can access the answers to these questions by emailing Pearson at Christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.