Fed Chair Jerome Powell holding a news conference following the March 22 meeting of the FOMC. Photo from Reuters via the Wall Street Journal.

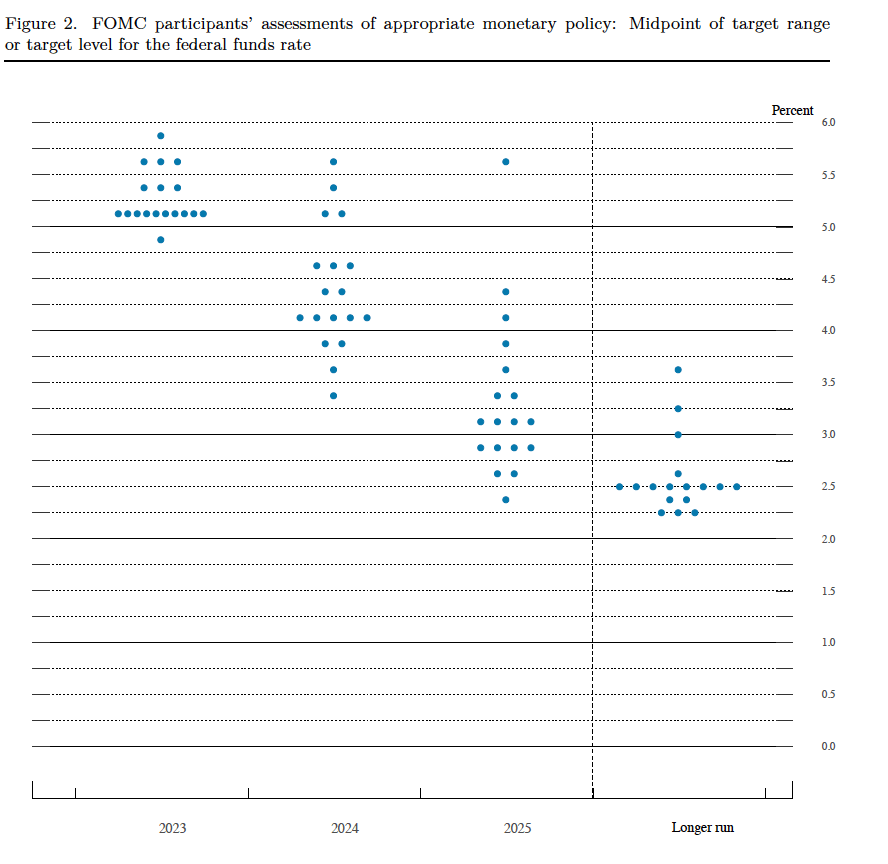

On March 22, the Federal Open Market Committee (FOMC) unanimously voted to raise its target for the federal funds rate by 0.25 percentage point to a range of 4.75 percent to 5.00 percent. The members of the FOMC also made economic projections of the values of certain key economic variables. (We show a table summarizing these projections at the end of this post.) The summary of economic projections includes the following “dot plot” showing each member of the committee’s forecast of the value of the federal funds rate at the end of each of the following years. Each dot represents one member of the committee.

If you focus on the dots above “2023” on the vertical axis, you can see that 17 of the 18 members of the FOMC expect that the federal funds rate will end the year above 5 percent.

In a press conference after the committee meeting, a reporter asked Fed Chair Jerome Powell was asked this question: “Following today’s decision, the [financial] markets have now priced in one more increase in May and then every meeting the rest of this year, they’re pricing in rate cuts.” Powell responded, in part, by saying: “So we published an SEP [Summary of Economic Projections] today, as you will have seen, it shows that basically participants expect relatively slow growth, a gradual rebalancing of supply and demand, and labor market, with inflation moving down gradually. In that most likely case, if that happens, participants don’t see rate cuts this year. They just don’t.” (Emphasis added. The whole transcript of Powell’s press conference can be found here.)

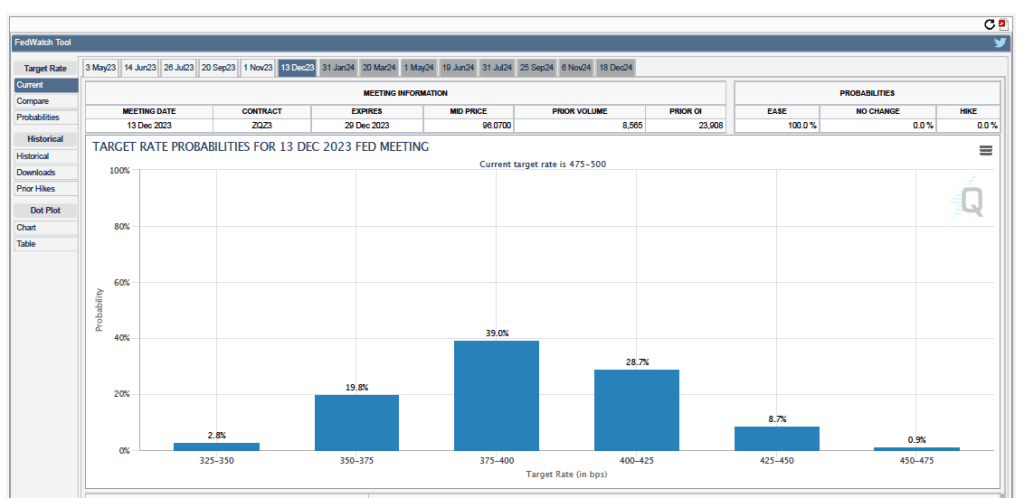

Futures markets allow investors to buy and sell futures contracts on commodities–such as wheat and oil–and on financial assets. Investors can use futures contracts both to hedge against risk–such as a sudden increase in oil prices or in interest rates–and to speculate by, in effect, betting on whether the price of a commodity or financial asset is likely to rise or fall. (We discuss the mechanics of futures markets in Chapter 7, Section 7.3 of Money, Banks, and the Financial System.) The CME Group was formed from several futures markets, including the Chicago Mercantile Exchange, and allows investors to trade federal funds futures contracts. The data that result from trading on the CME indicate what investors in financial markets expect future values of the federal funds rate to be. The following chart shows values after trading of federal funds futures on March 24, 2023.

The chart shows six possible ranges for the federal funds rate after the FOMC’s last meeting in December 2023. Note that the ranges are given in basis points (bps). Each basis point is one hundredth of a percentage point. So, for instance, the range of 375-400 equals a range of 3.75 percent to 4.00 percent. The numbers at the top of the blue rectangles represent the probability that investors place on that range occurring after the FOMC’s December meeting. So, for instance, the probability of the federal funds rate target being 4.00 percent to 4.25 percent is 28.7 percent. The sum of the probabilities equals 1.

Note that the highest target range given on the chart is 4.50 percent to 4.75 percent. In other words, investors in financial markets are assigning a probability of zero to an outcome that the dot plot shows 17 of 18 FOMC members believe will occur: A federal funds rate greater than 5 percent. This is a striking discrepancy between what the FOMC is announcing it will do and what financial markets think the FOMC will actually do.

In other words, financial markets are indicating that actual Fed policy for the remainder of 2023 will be different from the policy that the Fed is indicating it intends to carry out. Why don’t financial markets believe the Fed? It’s impossible to say with certainty but here are two possibilities:

- Markets may believe that the Fed is underestimating the likelihood of an economic recession later this year. If an economic recession occurs, markets assume that the FOMC will have to pivot from increasing its target for the federal funds rate to cutting its target. Markets may be expecting that the banks will cut back more on the credit they offer households and firms as the banks prepare to deal with the possibility that substantial deposit outflows will occur. The resulting credit crunch would likely be enough to push the economy into a recession.

- Markets may believe that members of the FOMC are reluctant to publicly indicate that they are prepared to cut rates later this year. The reluctance may come from a fear that if households, investors, and firms believe that the FOMC will soon cut rates, despite continuing high inflation rates, they may cease to believe that the Fed intends to eventually bring the inflation back to its 2 percent target. In Fed jargon, expectations of inflation would cease to be “anchored” at 2 percent. Once expectations become unanchored, higher inflation rates may become embedded in the economy, making the Fed’s job of bringing inflation back to the 2 percent target much harder.

In late December, we can look back and determine whose forecast of the federal funds rate was more accurate–the market’s or the FOMC’s.